Prem Watsa – Fairfax Financial Holdings Bloomberg/Bloomberg through Getty Images

Fairfax Financial Holdings

Fairfax Financial Holdings Limited, ( TSX: FFH: CA) through its subsidiaries, offers residential or commercial property and casualty insurance coverage and reinsurance, and financial investment management services in the United States, Canada, Asia, and worldwide. The business runs through Home and Casualty Insurance Coverage and Reinsurance, Life Insurance Coverage and Run-off, and Non-Insurance Business sectors. As part of its operating design, FFH owns numerous non-insurance companies, either partially or entirely. FFH is generally active in the business insurance coverage and reinsurance sectors, 2 cyclical sectors, which are experiencing an increase.

Considering That 1985, FFH has actually been headed by Prem Watsa, its creator, Chairman and CEO. Watsa is a renowned figure in the Canadian company world, and he and FFH have actually been compared to Warren Buffett and Berkshire Hathaway Inc. ( BRK.A) Watsa anticipated the United States Subprime crisis as early as 2006, referencing it in his letter to investors.

The Fairfax Financial company has actually been carrying out well, and this has actually been identified by the market. Experts have actually normally been favorable on the business, besides a current ‘brief report by Muddy Waters. On the day of this report, shares fell by as much as 12.5%

In this short article, I profile the essential hidden companies, and offer an outlook for the business. FFH reports its Q4 figures after the marketplace close on February 15th. I anticipate the Q4 figures to reveal ongoing revenue development. As an expert with substantial knowledge in insurance coverage and reinsurance accounting, I will likewise examine the brief thesis.

I rate FFH as a hold entering into incomes. I anticipate to update post incomes based upon strong efficiency and sectoral tailwinds.

The Fairfax Insurance Coverage Services

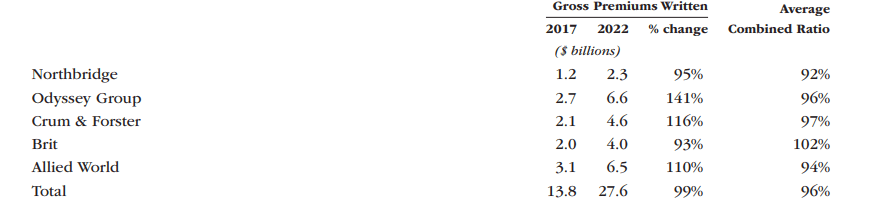

Fairfax runs through ownership of the essential companies described in the table listed below from the 2022 Letter to Investors

Fairfax

As can be seen, each of business has actually experienced quick development over the duration, with the entire group premiums composed having actually folded simply 5 years, with a typical Combined Ratio (CR or COR) of 96%.

The Combined Ratio is a crucial metric of worth development in Property/Casualty Insurance coverage (P&C), with a 96% Integrated Ratio relating to an underwriting revenue after expenses of 4% of premiums. Financial investment returns on the premium ‘float’ are then contributed to produce the monetary incomes. An insurance coverage company with a 96% combined ratio is carrying out well.

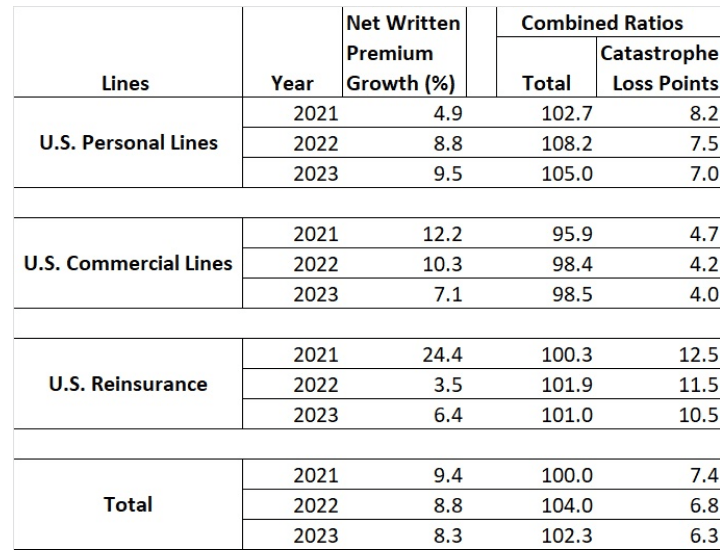

As a contrast, the table listed below from Insurance Coverage Journal reveals the efficiency of the total United States P&C market, with combined ratios of over 100% in every section from 2021-2023. The short article points out that 2017 was the in 2015 the market printed a sub-100% integrated ratio. While 5% bottom line outperformance does not sound much, in a service making $28bn of premiums each year, that’s a strong worth motorist.

Insurance Coverage Journal

So what company are the subsidiaries in?

Odyssey Re

Odyssey is a US-based pure play P&C reinsurer, composing 24% of the total group premiums. While Odyssey has a big United States direct exposure, it is likewise as a reinsurer varied worldwide, with operations in Europe and Asia. Odyssey has actually been regularly lucrative, having actually produced a combined ratio of under 100% regularly given that 2001.

While presenting Odyssey, I will enter into some information of the reinsurance company and outlook from released sources, however likewise sharing observations from my own comprehensive executive experience in the sector. As the majority of the FFH companies are active to a degree in the reinsurance sector, these observations are likewise appropriate to the outlook for these other companies.

Reinsurance can best be considered the insurance provider of insurance provider. It is a wholesale company offering security items to insurance provider, allowing them to handle their necessary capital and volatility. Crucial items consist of disaster reinsurance, which concentrates on security versus typhoons, earthquakes, floods etc.

Disaster losses have actually been at raised levels given that 2017, as described in this report by Aon.

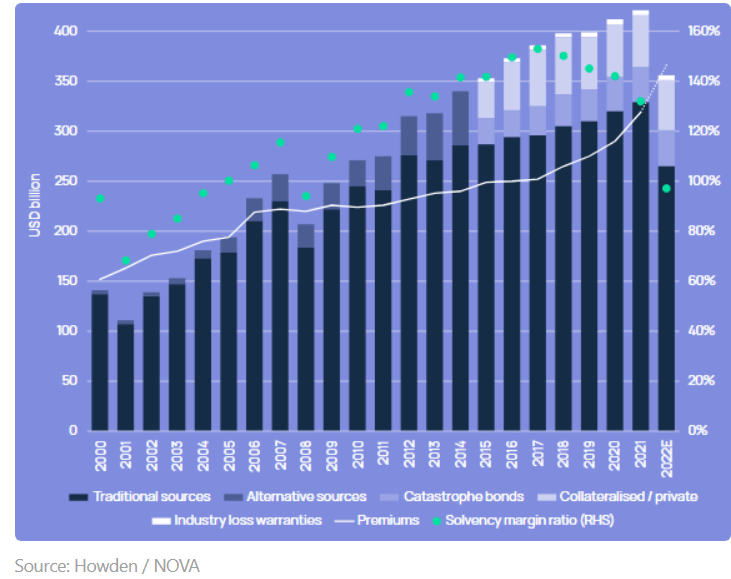

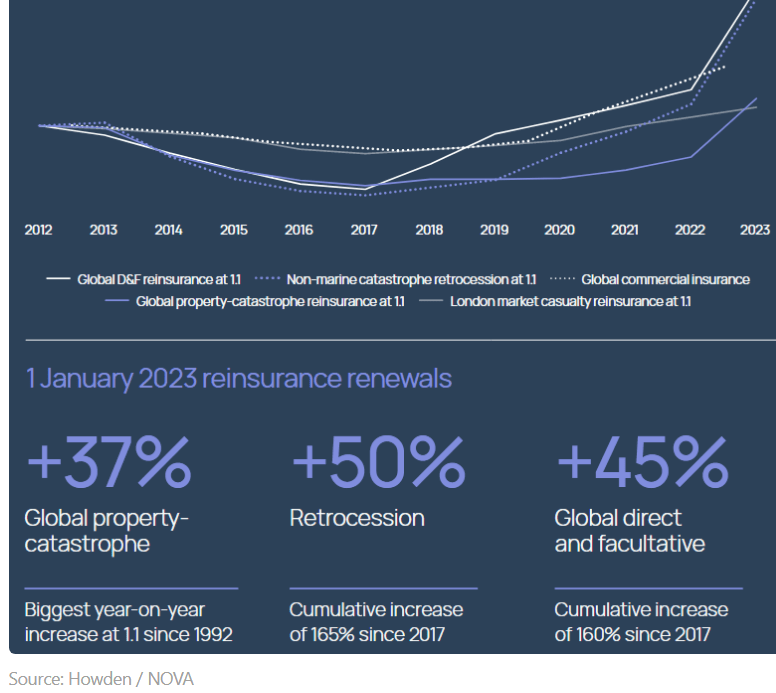

As a wholesale and capital extensive company, reinsurance has rather low barriers to entry, and this has actually been boosted over the last few years by the intro of securitised items, such as disaster bonds, which have actually helped with access to business by the capital markets. Gradually, Insurance coverage Linked Securities (ILS) have actually ended up being a big capital service provider in the area. The dark blue bars at the bottom of the display listed below program represent standard capital, the bars above Insurance coverage Linked Securities and Disaster Bonds.

Howden/Nova

As an outcome, although disaster experience has actually been progressively on the boost, plentiful capital reduced costs. These have actually led to a duration of bad outcomes for reinsurance business worldwide.

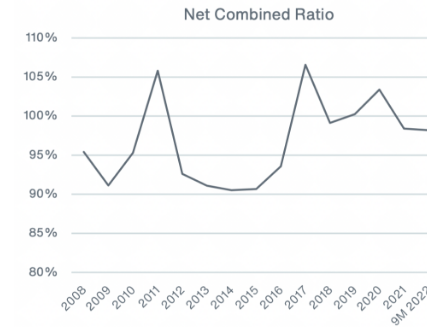

According to the chart listed below by, Aon – combined ratios for the sector surged in 2017, and remained above 100% till 2021. The primary factors for this were the increased disaster experience, however likewise losses from COVID Organization Disruption. The specialized section saw losses from COVID and likewise the Ukraine War. According to Aon’s report, the leading 22 Reinsurance business had a typical combined ratio of 101% given that 2017, and a paltry 5% Return on Equity.

Aon

2022 was a watershed year for the market, according to Munich Re, cyclone Ian and other disasters drove losses to $120bn for the year.

Along with the bad outcomes of the standard reinsurers, the substantial part of the capital in the market from ILS came under tension as the security that supports the item was ‘caught’ by being held versus overdue claims, and brand-new capital was sluggish to come to the marketplace. With safe rates increased, the spread provided by ILS items didn’t make up for the high-risk profile.

On the need side, high rates of inflation implied that the need for reinsurance capital increased considerably.

The outcome of this has actually been a sharp boost in the costs of reinsurance items in 2023 as displayed in the listed below display from Howden, a leading (Re) insurance coverage broker. 2023 was the most significant single boost in Disaster costs for years.

Howden/Nova

Reinsurance agreements, as a wholesale item offered to big business tend to be worked out each year, with around 60% of agreements falling due at January first, the well-known ‘Reinsurance renewal season’, and 25-30% mid-year in June/July.

While costs have actually stabilised, similar to inflation, they still increase in the 2024 renewals, according to the current outlook from Hannover Re, with a typical boost in costs of 2.3% after changing for inflation and loss patterns.

I anticipate to see Odyssey produce strong figures in the approaching outcomes. It is necessary to comprehend that the incomes for insurance companies and reinsurers just stream through as the liabilities that they presume run. This need to produce a profits tailwind for Odyssey as the lower priced company ‘runs’ their figures, and the greater priced company ‘works on’. In other words, the 2023 January and mid-year rate walkings will just reveal through completely over the coming quarters.

Allied World Insurance Provider (AWAC)

AWAC is a hybrid insurance provider and reinsurer that runs on an international basis. FFH got AWAC in 2017 for $5bn, which was a significant acquisition for the group. AWAC makes up 24% of the group premiums.

AWAC has actually been carrying out well, printing a 91% combined ratio in 2022, while growing at 14% year-on-year. AWAC composes a broad mix of classes of company, with a home and specialized predisposition to a business and business customer base.

AWAC runs with the broadest footprint of the group, with 23 workplaces worldwide. They likewise have a distribute at Lloyds of London.

In my view, AWAC uses scale and a great efficiency performance history to the FFH steady, plus some diversity of threat profile. Their operating sectors have less apparent concentration on the rates tailwinds detailed above than state, Odyssey, or Brit (listed below) however I anticipate to see at the least a continued success at 2022 levels.

Crum & & Forster

Crum and Forster, representing 17% of FFH, is a US-based specialized insurance provider, composing primarily Mishap and Health and Excess and Surplus Lines (E&S) insurance coverage. The E&S section is a specialised location that offers insurance coverage on a non-admitted basis for more difficult to put threats. Insurance coverage items and costs are firmly managed by the states. Modifications need comprehensive regulative filing. E&S insurance companies can change item and rates more easily than confessed insurance companies, and as such can be far more active in adjusting to altering threat conditions.

With insurance companies margins under pressure, and regulators in numerous states withstanding rate and item modifications, the E&S market removed in 2022. S&P approximated that E&S premiums increased by 28% in simply 6 months of 2022.

I anticipate Crum & & Forster to continue to reveal excellent development and strong margins.

Brit

Brit is a service based in Lloyds of London. which runs in the reinsurance and specialized insurance coverage classes, consisting of Direct and Facultative Residential Or Commercial Property (D&F) Brit contributes 14% of group premiums.

The majority of business composed by Brit is US-based, with substantial disaster direct exposures. Outcomes at Brit have actually been a laggard to the group, with a frustrating typical combined ratio of 102%. This is not lucrative for an insurance provider composing ‘brief tail’ business-like residential or commercial property.

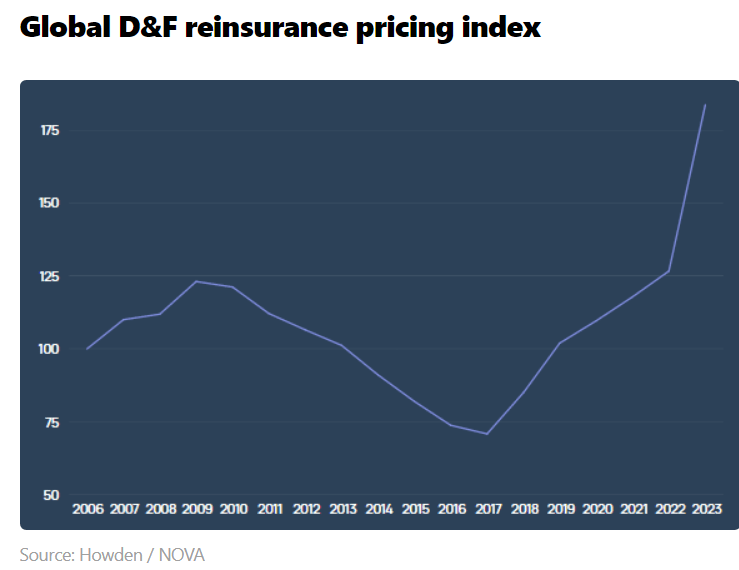

Favorable for Brit’s outlook is that the rates characteristics detailed above are highly affecting the London insurance coverage market. I will not duplicate the reinsurance disaster rates outlook, listed below is the D&F equivalent:

Howden/Nova

In addition to costs, policy conditions have actually relocated insurance companies favour, which need to lead to lower total claims versus the much greater premium swimming pool.

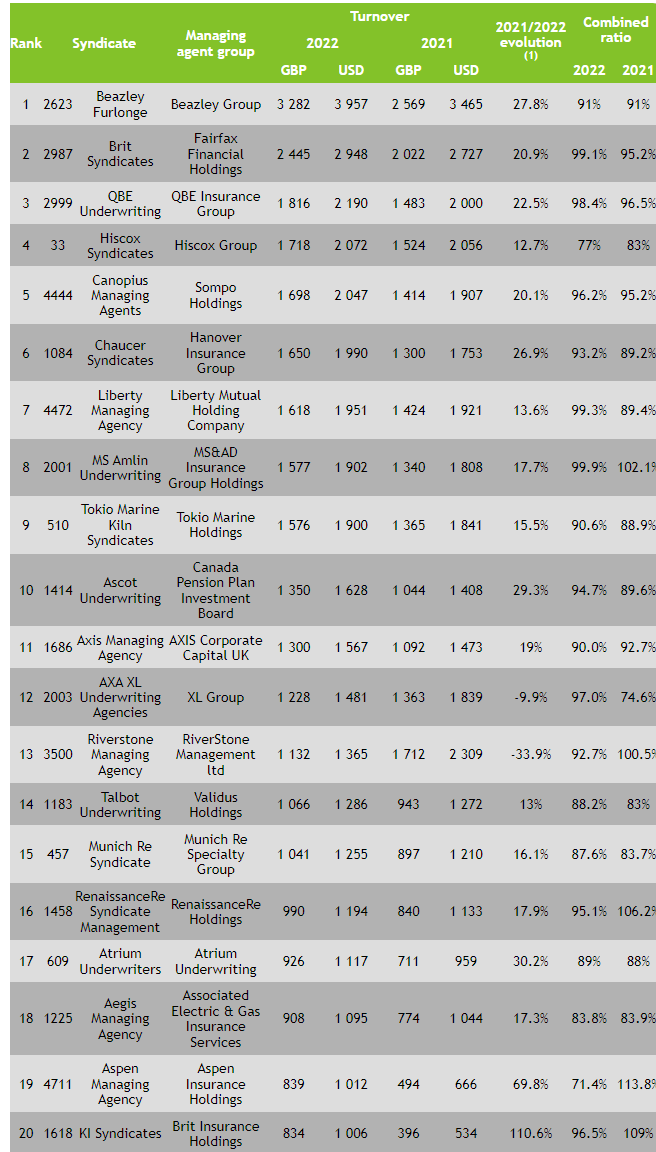

Brit reports its outcomes to Lloyds of London, which manages the ‘distributes’ that run in the market. Its core distribute, number 2987, was among the leading 20 most lucrative of the distributes at Lloyds of London. While the print was a dull 99%, the strong turn-around of the Lloyds market in 2023 produces a Q2 reported combined ratio of 85.2% I would anticipate Brit 2987 to report a substantially lower combined ratio for 2023.

Lloyds of London

Number 20 on the chart is Ki, another Brit distribute. Ki is an amazing development, making use of A.I. and online innovation to interrupt the London market threat positioning procedure. Lloyds of London is a market where insurance coverage offers are done collectively by numerous distributes. One distribute ‘leads’ by setting the terms and costs, and participating of the threat, and the Lloyds brokers run around other distributes to finish the handle ‘following’ distributes. Ki utilizes a web user interface on the brokers desktop to automate the procedure of functioning as a fan, utilizing a maker finding out algorithm to decide, which is anticipated to enhance the loss ratio and expense ratio. Development has actually been extraordinary, and the economies of scale need to continue to drop the expense ratio and drive the combined ratio down.

In my viewpoint, Brit will produce considerably enhanced outcomes, and strong development for 2023 and beyond.

Northbridge Insurance Coverage

Northbridge Insurance coverage is among the earliest properties in the FFH steady, representing 8% of total premiums. Northbridge is mostly a Canadian business lines insurance provider. The primary focus is on the specialized and small company insurance coverage sectors, with some home and vehicle insurance coverage.

The balance of the premiums are produced from a variety of business that are generally situated in emerging markets.

In General, the FFH stable of business is normally complementary, however runs in often overlapping sectors. From my observation, they are handled as self-governing shareholdings, with minimal group oversight. In this method, FFH might be taken a look at as an Insurance coverage and Possession fund supervisor as much as an insurer. The design appears comparable to Berkshire Hathaway because regard.

2023 outcomes at Q3

Considered that Q4 incomes are due quickly, I have actually concentrated on my view of the forward incomes and favorable outlook for FFH. The proof of these tailwinds came through in the Q3 reported numbers, and I anticipate there to be more enhancement to come.

Q3 outcomes were strong – some highlights:

- YTD gross premiums increased 7.5%.

- Integrated ratio a healthy 94% (FFH internal targets for its insurance coverage systems are sub 95% Combined Ratio).

- Share repurchases 1% of float in 2023.

- Indicated Return On Equity of 20%.

- The dividend was raised by 50% simply last month.

- All in all, a record arise from a growing company.

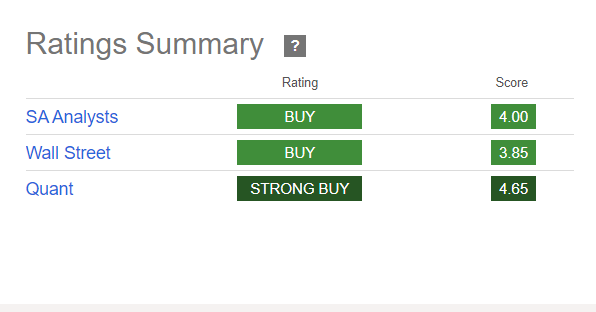

Looking for Alpha experts are bullish.

Looking For Alpha

Quant Aspect Grades are strong, revealing high marks for whatever other than evaluation.

Looking For Alpha

This isn’t unexpected offered the strong run the stock has actually had more than current years.

Assessment

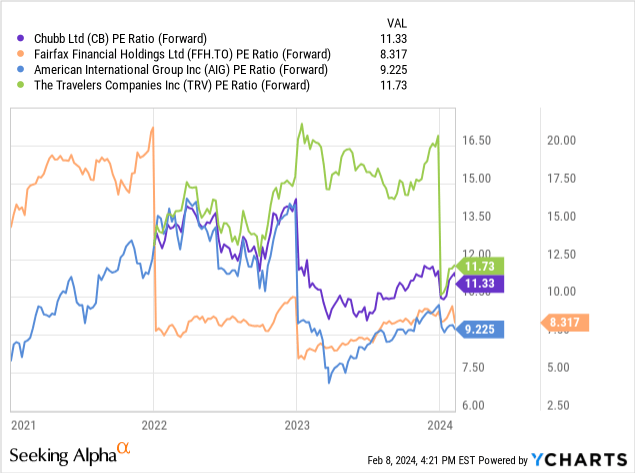

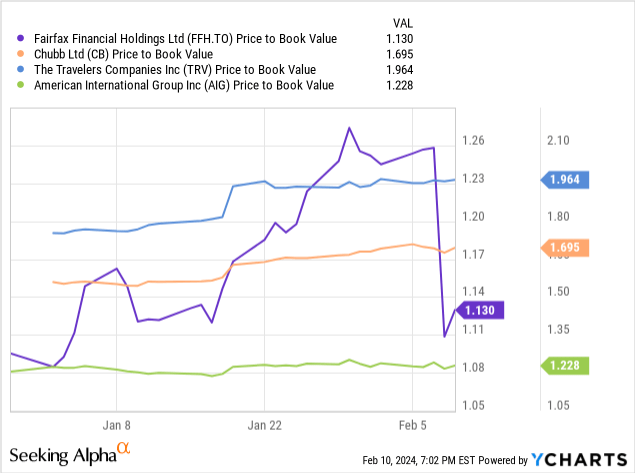

Compared to peers, FFH evaluation is still appealing on a price/earnings basis. On a cost to book worth basis, the evaluation is a bit richer, with the run-up over the current months leading the rate to book prior to the current drop. The rate to book variety is quite tight.

FFH is an Industrial Residential Or Commercial Property and Casualty Insurance Company and Reinsurer, running in a market which has actually been coming off a cyclical slump given that the post-COVID age. The market has actually had a tough couple of years, showing the high volatility of business. Market value are modest throughout the section. Leading entertainers like The Travelers Companies, Inc. ( TRV) and Chubb Limited ( CB) have a price/earnings multiple of around 11.5. FFH P/E after recently’s drop is just 8.3. This is low for a service which has actually doubled in size given that 2017 and produced constant revenues.

The favorable market conditions are anticipated to continue through 2024.

I anticipate the FFH Q4 results to continue to reveal this, and for future incomes to speed up. In my view, FFH ought to trade at a P/E of 10x, which suggests 20% upside from the existing rate on recognition of the efficiency patterns.

The bear case

FFH analysis was widely favorable till a bear case emerged recently (the week before incomes).

Brief seller Muddy Waters (MW) revealed a brief position on FFH throughout a CNBC interview with Carson Block, the company’s creator.

MW declares that by accounting adjustment, FFH is overemphasizing its book worth by 18%. FFH has actually increased reported book worth by 9% given that the monetary crisis.

MW thinks that accounting controls have actually developed 60% of this boost. This suggests that their view of the real book worth CAGR is just 5.4%.

There are 3 parts of the bear case:

- Aggressive book brings of independently held properties.

As independently held properties are brought at management’s worth price quote instead of marked-to-market rates, there is some discretion in evaluation. MW reports several properties which they think to be miscalculated in MW books.

One example offered is that of Dish – a dining establishment stock which FFH took personal. MW views the real worth of this possession to be lower than brought in the FFH accounts.

FFH owns a ‘run-off reinsurer’ called Riverstone, which Block declares is merely off-balance sheet financial obligation dressed up as equity.

J.V. Riverstone is a J.V. formed with OMER, a Canadian pension fund, to decrease the run-off liabilities being brought by FFH on its balance sheet. I have the benefit of substantial experience with run-off reinsurance, so let me unload this.

Run-off transfers are a typical tool for P&C insurance companies to make their balance sheets leaner and assist them fund brand-new company.

They are generally structured as either Loss Portfolio Transfers, which move the whole insurance coverage liabilities from one business to another, or Unfavorable Advancement Covers, which put a cap on the prospective drawback of reserve insufficiency.

Deals undergo stringent accounting requirements to guarantee that there is proper threat transfer. For any accounting geeks checking out, FAS 113 is the United States GAAP basic threat transfer test. This requirement was presented to prevent reinsurance deals being abused to dress up financial obligation. As gone over listed below, IFRS17 has comparable safeguards.

In my view – while the Riverstone deal was structured in an uncommon method, forming a J.V. with a financier, – the total objective of the deal appears quite vanilla, and rather typical in the insurance coverage market.

Another criticism is around the adoption of IFRS 17 accounting. This is an extremely complicated accounting modification which is ending up being a basic replacement for United States GAAP accounting for insurance provider throughout much of the world, consisting of Europe, Canada, and the UK.

IFRS17 ended up being the reporting requirement for Canadian P&C insurance companies from Jan. 1st 2023.

The bear case is that the favorable effect of IFRS17 application on book worth was overemphasized when compared to the effect on some other insurance provider when they carried out IFRS17

The concept behind IFRS 17 is that capital and margin development are formulaically stemmed from the profile of the insurance coverage liabilities.

There is specific acknowledgment of the ingrained worth of business. While United States GAAP accounting utilizes premiums and reserves on a relatively generic basis, IFRS is far more attuned to the underlying modelling presumptions of each portfolio. The approach takes a ‘net present worth’ of the particular portfolio to examine the worth of business.

It is not unexpected to me to see a huge variation in effects in between various insurance provider, specifically in between reinsurers, individual lines insurance companies, and business insurance companies, as the margin profiles, and period of liabilities are extremely various.

In my experience, the international audit companies have actually been laser-focused on handling IFRS17 application, and guaranteeing finest practice.

Preparations for IFRS17 were thoroughly handled by OFSI, the Canadian regulator, with half-yearly reporting of effects and modelling presumptions in application development reports from 2020 onwards.

Appropriate to the subject of run-off deals above, IFRS17 likewise has a specific charge for ’em bedded warranties’ which would nullify the favorable effects of non-risk transfer deals represented under IFRS17.

A more concern is presented on the governance side, where obviously the FFH auditor has actually been PWC for a long period, and the Board of Directors consists of not simply member of the family of Prem Watsa, the creator, however likewise a previous senior executive of PWC. I would concur that it is uncommon to see audit period of this period.

FFH reaction

FFH provided a quite simple reaction to the brief report. Generally rejecting any accounting abnormalities, and appropriately concentrating on the strong Q3 incomes, which produced a record outcome, and advising investors that the Q4 incomes are due for release after the marketplace closes on 15th February.

It would have been more engaging if they had the ability to offer an outlook to the approaching outcomes, and/or reveal a purchase of shares by the business, or essential executives, however offered the distance to incomes, neither of these actions is possible.

An independent view

In my view, while the MW report raises some intriguing concerns on accounting and governance, the bear case is overemphasized. Fairfax, as a Canadian Insurance provider, goes through guideline by OFSI, the Canadian monetary services regulator. From my experience, OFSI is extremely persistent. The relevant accounting requirements are IFRS 17, which are rather authoritative.

I have little issue over the IFRS 17 application concern, or the Riverstone management of liabilities.

The evaluation of independently held properties may raise legitimate inquiries on book worth computations.

Even the brief thesis puts the amount of all the MW obstacles at 18% prospective overvaluation of book worth. If certainly the declared overvaluation of the personal properties does develop a partial overvaluation of say 5% of book worth, I do not see an engaging brief case.

I would put more concentrate on the underlying company efficiency and outlook, which as I discussed above are extremely favorable.

Dangers to the thesis

In addition to the claims of accounting adjustment, I see threats to business efficiency as:

- Possession threat. The FFH possession base is not as diversified as a lot of insurance companies.

- Environment and disaster threat. The threat of rates gains being surpassed by loss patterns.

- Inflation threat Just like environment and disaster threat, rate boosts are surpassed by inflation patterns.

- Regulative threat. OFSI examination of accounting practices hindering business.

- Booking threat. Understatement of liabilities. This is alleviated by the active run-off management.

In summary

- While FFH’s evaluation has actually increased, business is healthy and growing.

- Much of business is taking pleasure in multi-year record favorable incomes tailwinds.

- The brief thesis does not in my view represent the underlying company strength.

- Accounting and deal practices of FFH do not look amazingly uncommon from a specialist perspective.

- I see no factor for financiers to stress entering into incomes.

- I see FFH as a hold pending Q4 incomes and a more extensive counterclaim of the brief thesis from FFH.

Editor’s Note: This short article talks about several securities that do not trade on a significant U.S. exchange. Please know the threats connected with these stocks.