Richard Drury/DigitalVision by means of Getty Images

Shares of Heron Therapies ( NASDAQ: HRTX) have actually recuperated a fair bit in the last couple of months, however the stock is just somewhat above the levels it traded at the time of my last short article’s publication in April 2023. The business changed CEO Quart at the time and was essentially in survival mode in the last number of quarters due to Zynrelef’s absence of traction in the post-operating discomfort market, and I argued that it can produce worth however that it deals with a difficult roadway ahead which it requires to attend to the low money balance.

I should state I am impressed by the development on a number of fronts– the fortifying of the balance sheet and costs cuts that have actually ended the survival mode, and the regulative and advancement execution to get the broadened label for Zynrelef as quickly as possible which the business has actually done and to get a more easy to use variation of Zynrelef on the marketplace which is still not there yet however getting more detailed.

Nevertheless, no considerable development was made on the most essential front– earnings development of the item portfolio. Aponvie’s launch appears like a bust for the avoidance of post-operative queasiness and throwing up (‘ PONV’) and getting traction with Zynrelef will still need the pointed out item discussion enhancement and considerable marketing efforts. The roadway ahead is still hard however I think Heron is now in a much better position than it was a year back.

Money burn to drop significantly due to cost cuts and gross margin enhancements

Heron ended September 2023 with $77.5 million in money and equivalents. The business handled to raise $30 million by watering down the investor base and it protected a $50 million loan of which $25 million is still offered. Supporting the balance sheet was extremely essential as money was running low– it would have been just $22.5 million if the business did not raise money and down to around $10 million at the end of 2023.

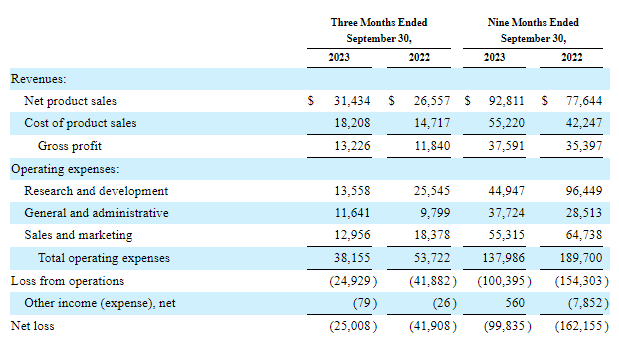

Cutting costs hurt however essential. Management states overall operating costs (leaving out share-based settlement, devaluation, and amortization) will drop from $182 million in 2022 to $135 million in 2023 and to $108-116 million this year. These enhancements have actually ended up being noticeable in the earnings declaration as the bottom line has actually narrowed in the last noted quarter and the very first 9 months of 2023.

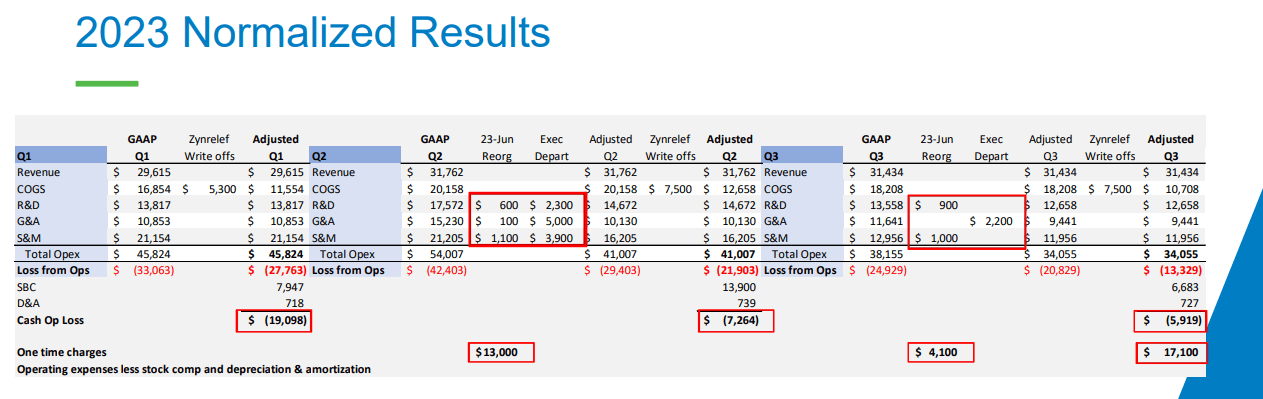

Heron Therapies Q3 2023 report

And while the earnings declaration still reveals a $25 million loss in Q3 and $99.8 million for the very first 9 months of 2023, running money burn was just $7.3 million and $5.9 million in Q2 and Q3 of in 2015, respectively, and a great piece of the bottom line was because of Zynrelef stock writedown and one-time charges connected to layoffs and expense cuts.

Heron Therapies financier discussion

Surprisingly, the considerable decrease in costs had no considerable unfavorable result on the item portfolio’s development rates. I seriously question the numbers would have been substantially much better if costs hugged $200 million in 2023.

Heron’s gross margins have actually been either not fantastic or awful since the launch of Cinvanti in 2018. It dropped from the 70s variety in 2018 to the low 40s at one point in 2022, regardless of the business’s guarantees for enhancements. The brand-new CEO Craig Collard sounded more reasonable in 2015 and while there were no enhancements in the next 2 quarters due to Zynrelef’s stock writedowns, he anticipates the gross margin to reach 62% in Q4 2023, 68-70% in 2024, and over 75% in 2025 and beyond, driven by increased batch sizes, functional effectiveness, and say goodbye to stock writedowns.

The enhanced gross margin and modest earnings development in 2024 might get the business to the assisted capital breakeven and if the trajectory continues to enhance, it must end up being lucrative in 2025.

I likewise think there is extra space to cut R&D costs (which will be north of $50 million in 2023 even if we omit share-based settlement) as the business does not have a pipeline beyond the Zynrelef item discussion jobs such as the Vial Gain Access To Needle for which FDA approval is anticipated later on this year and the prefilled syringe with the advancement anticipated to end at some point in 2026. As each of these jobs is finished, R&D expenses need to even more reduce.

These actions were important for Heron to make it through and the stabilization stage is most likely over. The business can now concentrate on going back to more powerful development, a piece that is still missing out on which stays important if we are to see considerable worth production in the following years.

Zynrelef– label growth and CrossLink collaboration protected and need to assist speed up development in 2024

Last month, Zynrelef got FDA approval to broaden the item label to consist of “soft tissue and orthopedic surgeries consisting of foot and ankle, and other treatments in which direct exposure to articular cartilage is prevented.” It was formerly authorized for foot and ankle, small-to-medium open stomach, and lower extremity overall joint arthroplasty treatments in grownups. The business approximates the broadened label now covers 13 million treatments a year, up from 7 million.

This and the just recently revealed collaboration with CrossLink might cause some development velocity of Zynrelef moving forward, however I am not anticipating wonders. Not up until the item discussion enhances. The primary step because instructions is the prospective approval of the Vial Gain Access To Needle (‘ VAN’) later on this year as it might accelerate the Zynrelef withdrawal time from one minute or more to 20-30 seconds. Heron’s marketing research and consumer feedback because launch suggest the present Vented Vial Spike (‘ VVS’) can be troublesome which enhanced withdrawal would be considerable and boost adoption.

Nevertheless, I am constantly mindful about putting excessive faith into marketing research, particularly thinking about Heron’s previous research study that suggested Zynrelef would be chosen over Pacira BioSciences’ ( PCRX) Exparel. Exparel is still a half-a-billion-a-year item while Zynrelef’s run rate is hardly in the double-digit millions after almost 3 years on the marketplace.

Getting to the prefilled syringe stage is most likely important and need to represent the last and crucial action, however it is not anticipated before September 2026.

I am still doubtful of Zynrelef’s prospective to go back to more considerable development up until (a minimum of) the approval of the VAN, and (most likely) up until the approval of the prefilled syringe, however I do anticipate development to speed up in the following quarters.

Aponvie appears like a bust

I stated in 2015 that the launch of Aponvie was a wild card, however I was extremely doubtful of its capacity up until it was verified in the quarterly numbers. Numerous quarters in, Aponvie is hardly offering with less than $1 million in net sales in the very first 9 months of 2023.

The business shared some favorable signs such as the growing variety of purchasing accounts and some favorable early experiences driving increased usage, however since today, I do not see Aponvie sales coming close to Zynrelef, not to mentioned ending up being considerable in the following years. This is still quite a “reveal me” story.

Upside prospective

Back in 2022, I decreased my 2027 overall net sales price quote variety from $500-600 million to $400-450 million, and the appraisal variety from $15-20 to $9-11 per share.

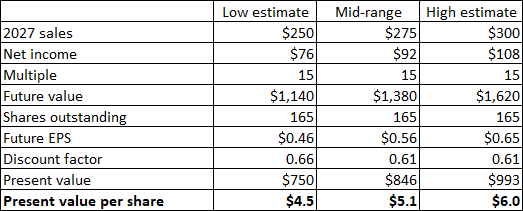

Even this decreased circumstance appears extremely not likely now, and I am additional lowering it to $250-300 million with a presumption of Zynrelef getting to more than $100 million in yearly sales, driven by the broadened label, the CrossLink collaboration, the prospective approval of Vial Gain access to Needle in the 3rd quarter and of the prefilled syringe in 2026. The appraisal variety presumes gross margins will reach or surpass 75% which running expenses will somewhat reduce from 2024 levels as an outcome of lower R&D costs which I anticipate will be partly balanced out by increased SG&An expenditures. These presumptions equate to a net present worth of $4.5 to $6 per share.

Author’s price quotes

The decrease is not just driven by decreased net sales and lower net margin presumptions however likewise by the increased share count as the business was required to water down the investor base to get the much-needed money. The appraisal likewise presumes the business will either re-finance or repay in money the $150 million in impressive 2026 convertible notes which Heron will have a favorable net money position by the end of 2026.

Dangers

The majority of today’s short article had to do with the troubles and dangers, however I will sum up and point out other dangers:

- The business might run out the woods economically with the conditioning of the balance sheet, enhanced gross margins, and potential customers for capital breakeven by the end of 2024, however reaching capital favorable is by no methods ensured, and arriving might not lead to share rate gains in the lack of topline development.

- I have actually not pointed out the oncology items Cinvanti and Sustol. Their net sales require to stay steady or grow somewhat moving forward to guarantee ongoing stability as they still represent most of Heron’s net sales. Cinvanti is still, without a doubt, Heron’s biggest item, and the business will require to safeguard its patents in court versus a number of generic filers. Losing in court would be ravaging for Heron and, in the lack of development from other items, would put the business at threat of destroy. The Markman hearing last summertime appeared to have actually worked out and it has actually enhanced Heron’s legal position in the approaching trial.

- For the pointed out upside prospective to be emerged, we would require to see more than simply cost-cutting and better gross margins. If Zynrelef’s sales development does not speed up regardless of the current label growth, CrossLink collaboration, and the anticipated VAN approval later on this year, I am skeptical there will be other opportunities for worth production aside from the not likely abrupt rise in net sales of Aponvie.

- If the development and gross margin trajectory do not go as prepared, Heron might require to raise money once again and at extremely undesirable terms to existing investors.

Conclusion

Heron might run out the woods in regards to near and medium-term threat of insolvency, however it still requires to cross a number of barriers before it can end up being a real development stock. The dangers are still considerable, however I can see a course to good and possibly considerable worth production in the following quarters and years.

The broadened label of Zynrelef and the collaboration with CrossLink are actions in the best instructions and could, together with Vial Gain access to Needle approval later on this year put the item on a course to development velocity in 2025 and possibly more considerable development velocity if the prefilled syringe variation is authorized in 2026.