deepblue4you

In this day and age, it sort of feels that the inventory marketplace has little or no persistence for turnaround tales. Traders latch onto the most recent expansion tales and pay little or no consideration to corporations which might be suffering with trade transitions.

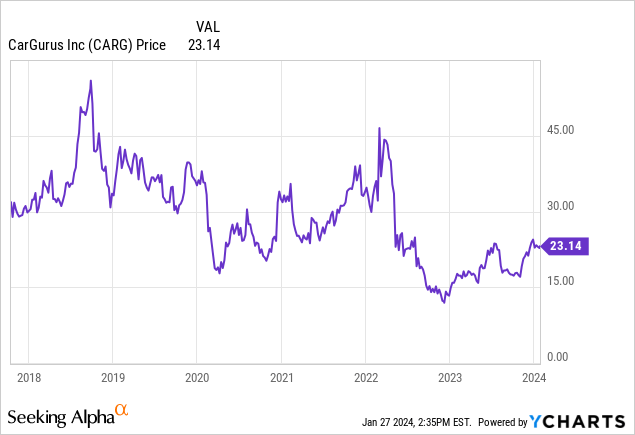

CarGurus (NASDAQ:CARG) falls squarely into this bucket. Coping with softer post-pandemic call for for used automobiles, plus managing its rushed access into the wholesale trade, income and benefit expansion has stalled. Nonetheless – there may be hope, because the inventory is up greater than 30% over the last 12 months, reflecting fairly of a go back to self belief in CarGurus’ basics.

I remaining wrote a impartial article on CarGurus in July. Since then, two issues have happened:

- CarGurus’ market trade is returning to boost up expansion charges. The corporate is keeping up #1 proportion in U.S. website online visits, and a possible building up in call for for used automobiles amid falling costs might assist to spur further expansion for the corporate in 2024.

- The corporate has stabilized its wholesale arm. Earnings are clinging round breakeven in spite of a way smaller scale, with CarOffer now not burning a hollow thru CarGurus’ base line.

Go back to expansion on the market section is particularly necessary as a result of it is this kind of excessive margin income for CarGurus. This trade necessarily attracts promoting bucks from sellers hoping to put it up for sale their stock on CarGurus’ website online, which for a few years has been the go-to vacation spot for used vehicle customers researching automobile purchases. Paying trader counts have returned to expansion; as has reasonable spend in step with trader. And because promoting area prices little or no for CarGurus to promote, this income flows instantly into the corporate’s base line.

With all of this in thoughts, I am elevating my score on CarGurus to bullish. This 12 months, with the S&P 500 drifting close to all-time highs round 4,900, I believe contrarian performs are going to be important elements of our portfolios if we need to beat the wider markets: and this can be a turnaround tale with sturdy fresh datapoints to financial institution on.

Down ~2% year-to-date already, I will take the following dip on this inventory as a possibility to shop for.

This autumn profits preview

The following catalyst for CarGurus might be its This autumn profits free up (and FY24 outlook free up), which is predicted for early February.

Whilst profits is after all a wildcard for an organization in a transitory state like CarGurus, we be aware that CarGurus has overwhelmed Wall Boulevard’s expectancies in every of the previous 4 quarters:

CarGurus profits historical past (In search of Alpha)

We will have to be aware as smartly that past CarGurus’ fresh monitor report, there are a variety of macro drivers that are meant to improve energy in This autumn. Headlines have flooded in all over the fourth quarter on y/y decreases in used vehicle costs. With affordability and excessive rates of interest being the main headwind in opposition to vehicle gross sales over the last 12 months, moderation in costs (and extra consideration towards value cuts) will have to assist to get used-car consumers off the sofa, reaping rewards sellers who will in flip spend extra to function their stock on CarGurus’ website online.

Aid in fuel costs may be some other favorable mover, guidance extra consumers clear of EVs and hybrids and favoring the used-car marketplace (as maximum of this stock has a tendency to be conventional combustion engine).

Bettering metrics all around the board

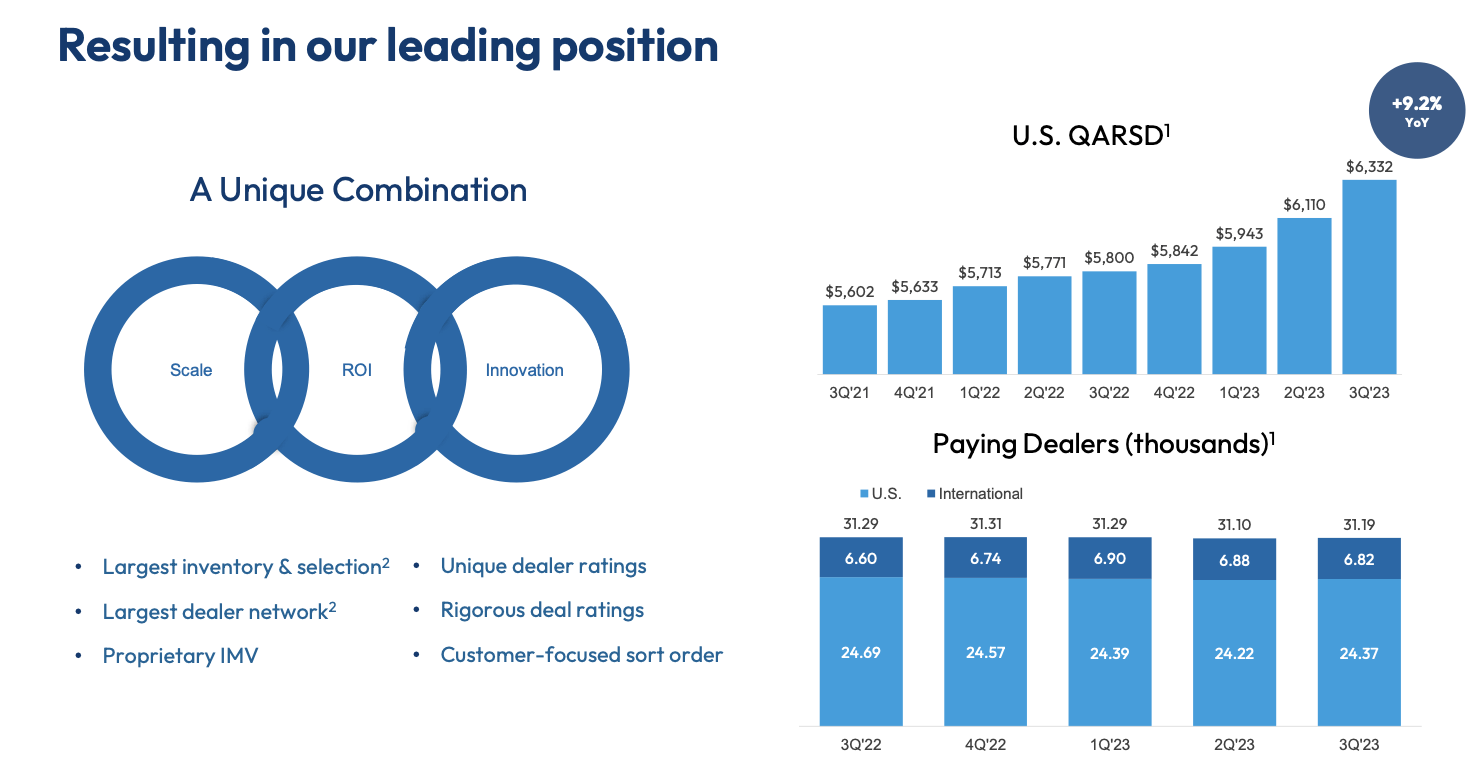

Let’s now illustrate how precisely CarGurus has controlled to show its basics round thru its most up-to-date quarter. After a couple of quarters of decline in paid trader counts, CarGurus has controlled so as to add paid sellers for the primary time since 2022, up ~9k quarter-over quarter to 31.19k paying sellers.

CarGurus market metrics (CarGurus Q3 profits deck)

Now not simplest that, however quarterly income in step with paying trader has additionally greater 9% y/y (and four% sequentially) to a excessive of $6,332. All in all, market income greater 8% y/y to $177.9 million, an acceleration over flattish expansion within the earlier two quarters.

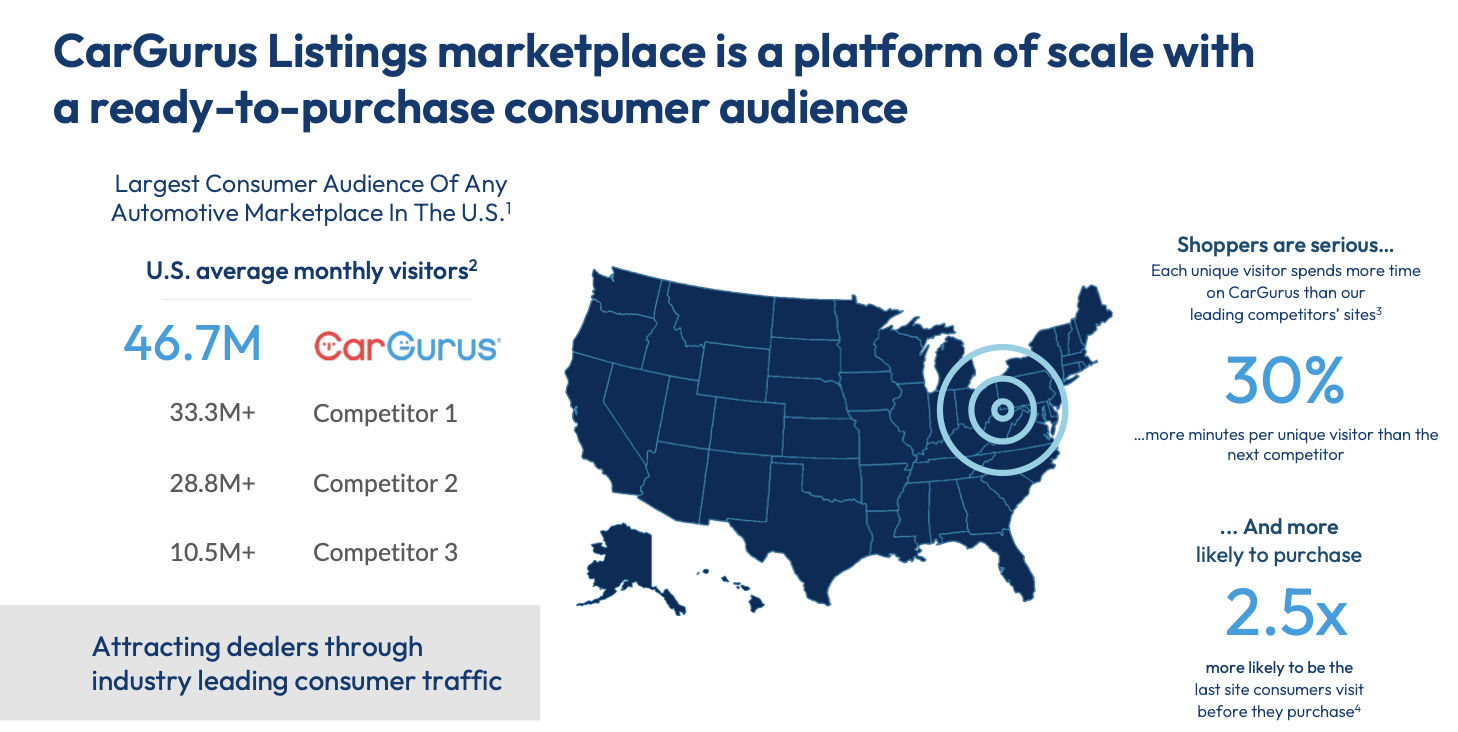

Market income is available in at a 92% GAAP gross margin. This can be a extremely scalable trade that attracts on CarGurus’ immense visitors proportion amongst used vehicle consumers. The chart underneath showcases that CarGurus’ 46.7 million reasonable per thirty days guests towers over its competition.

CarGurus visitors stats (CarGurus Q3 profits deck)

Consistent with CEO Jason Trevisan’s remarks at the Q3 profits name:

In the USA, we proceed to ship extra price to our sellers, which is mirrored in upper quarterly reasonable income in step with subscribing trader or QARSD, and we imagine will make stronger buyer retention and long-term growth.

Expansion in QARSD comes from including new sellers at upper marketplace charges and growth of present trader pockets proportion thru checklist upgrades, product innovation and adoption, renewals, lead amount and lead high quality. One fresh expansion lever of QARSD is our annual trade evaluations, or ABRs, which delivered leads to Q3, in keeping with the prior quarter.

We proceed to look a powerful proportion of sellers accepting our renewals movement and a strong win again charge for many who had churned within the prior quarter. Moreover, we have now additionally observed wholesome product connect charges and better adoption of annual contracts.”

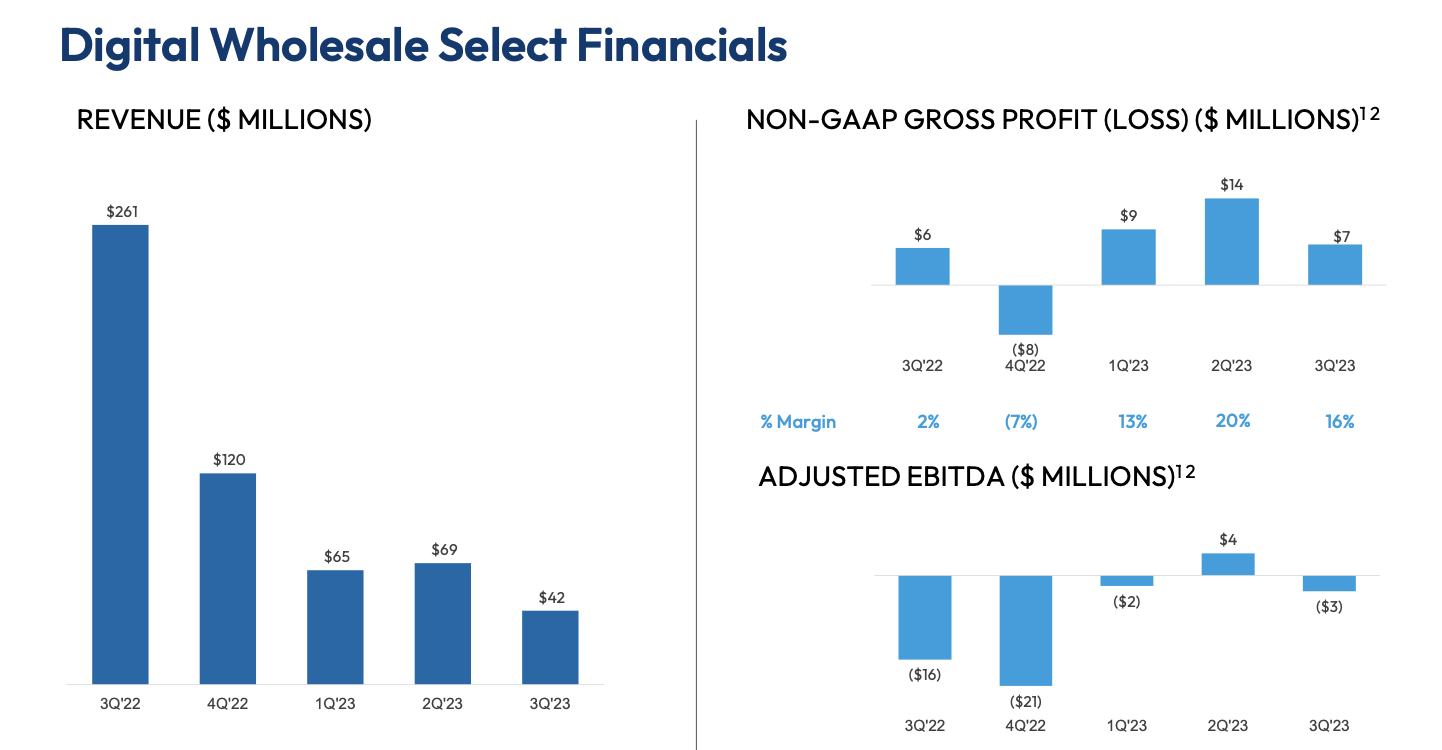

Secondly: control has additionally been ready to handle ~breakeven profitability within the wholesale and product segments. As further background right here, recall that the corporate offered Speedy Max Money Be offering to immediately purchase automobiles from customers, and purchased CarOffer to facilitate dealer-to-dealer transactions. Despite the fact that income scaled temporarily in those hands, earnings sunk: and so CarGurus made the verdict to decelerate those segments, to some extent the place it is a minimum of now not impacting the base line as proven underneath:

CarGurus wholesale metrics (CarGurus Q3 profits deck)

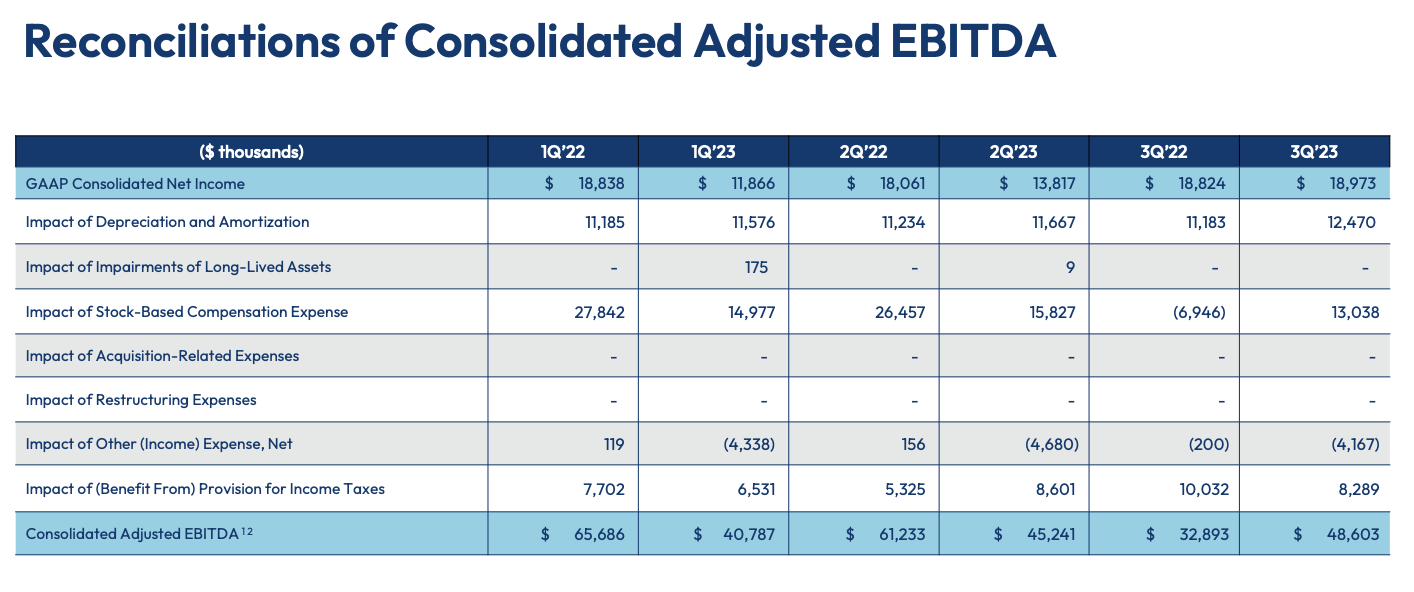

General adjusted EBITDA in the latest quarter jumped 48% y/y to $48.6 million, or a 22.1% adjusted EBITDA margin – which I view to be extra consultant of the corporate’s margin possible going ahead as extra of its income mixes again into high-margin market income.

CarGurus adjusted EBITDA developments (CarGurus Q3 profits deck)

Valuation and key takeaways

CarGurus’ go back to significant adjusted EBITDA profitability, personally, creates an excellent chance for traders to financial institution in this turnaround – and nonetheless at affordable valuations.

At present proportion costs close to $23, CarGurus trades at a $2.60 billion marketplace cap; and after netting off the $447.1 million of money on its most up-to-date stability sheet (in opposition to 0 debt), its ensuing endeavor price is $2.15 billion.

In the meantime, for FY24, Wall Boulevard analysts predict CarGurus to generate $985.9 million in income, representing 8% y/y expansion. Once more, if we suppose that {the marketplace} trade continues to develop, its high-margin contribution will have to permit CarGurus to a minimum of handle its Q3 ranges of adjusted EBITDA margin. Preserving its ~22% margin profile on FY24 income with out assuming any further margin leverage (which is cheap as the corporate scales trader transactions again up on CarOffer), we get to $217 million of adjusted EBITDA in FY24, and a a couple of of 9.9x EV/FY24 adjusted EBITDA.

There may be extra upside right here, personally, as CarGurus continues to lean again on its unique high-margin market trade and proceed to power its wholesale segments towards profitability. Particularly as CarGurus is favorably arrange for a This autumn profits beat within the subsequent month, it is sensible to hop within the educate right here prior to CarGurus inventory makes an additional restoration.