Darren415

Invite to another installation of our CEF Market Weekly Evaluation, where we go over closed-end fund (” CEF”) market activity from both the bottom-up – highlighting specific fund news and occasions – along with the top-down – offering an introduction of the more comprehensive market. We likewise attempt to supply some historic context along with the appropriate styles that seem driving markets or that financiers should bear in mind.

This upgrade covers the duration through the 2nd week of January. Make sure to take a look at our other weekly updates covering business advancement business (” BDC”) along with the preferreds/baby bond markets for viewpoints throughout the more comprehensive earnings area.

Market Action

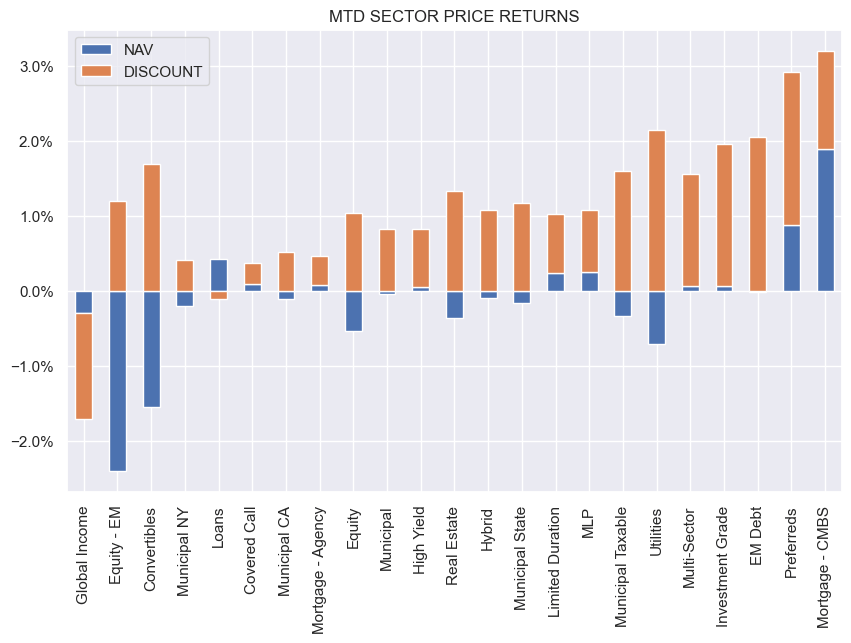

Many CEF sectors were up on the week as both stocks and Treasuries rallied. Month-to-date, nevertheless, NAV efficiency is combined. CMBS has actually up until now provided the very best return – a sharp turn-around of its 2023 relative efficiency. Discount rates, nevertheless, have actually tightened up throughout all however one sector, showing restored financier self-confidence in the area.

Methodical Earnings

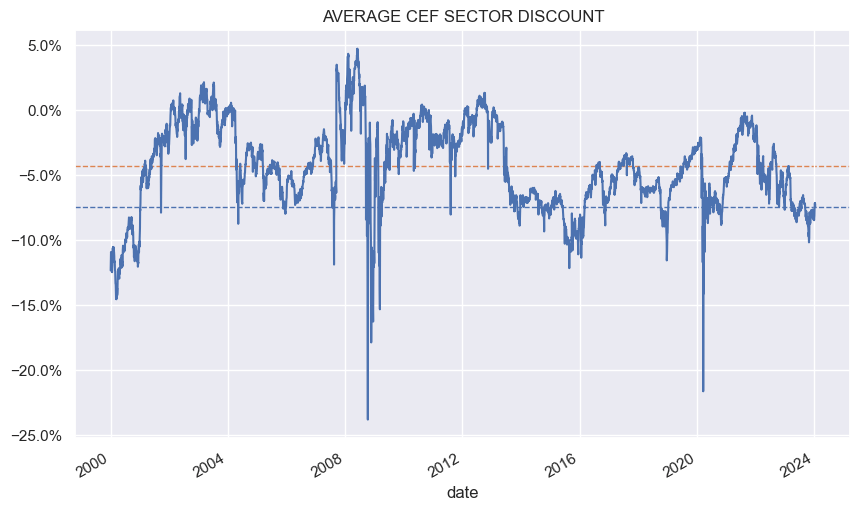

On a typical sector basis, discount rates have actually tightened up a couple of portion points considering that the bottom in 2015.

Methodical Earnings

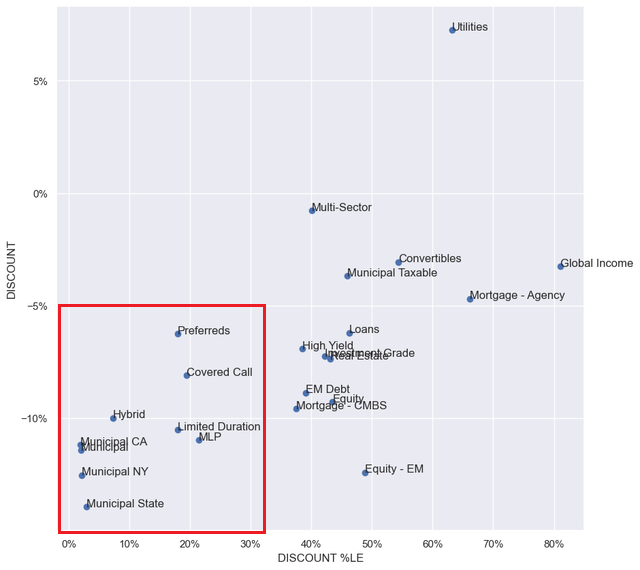

Sectors like Munis, Hybrids and Preferreds continue to trade at double or high single-digit discount rates. They likewise trade at low discount rate percentiles, suggesting their discount rates are large relative to their own history.

Methodical Earnings

Market Styles

Today CEF sector classifications began up on the service. Particularly, there was a concern of why a fund like the DoubleLine Earnings Solutions Fund ( DSL) is positioned in the Multi-Sector classification in our CEF Tool while it beings in Worldwide Earnings on CEFConnect.

In reality there are numerous distinctions in between our sector positioning which of CEFConnect. This is due to the fact that of, approximately speaking, simple cases and difficult cases. For example, a fund like John Hancock Premium Dividend Fund ( PDT) is positioned in the Preferreds sector by CEFConnect whereas we have it in the Hybrid sector. PDT is a simple case – its allotment is almost half in typical stock with preferreds comprising less than a quarter of the portfolio. There is no other way it ought to be designated to the preferreds sector.

JH

There are likewise difficult cases such as the Ares Dynamic Allowance Fund ( ARDC). Its allotment has actually been approximately uniformly split in between set and floating-rate properties. For instance, it was 40% repaired in 2019 which increased to 50% repaired in mid 2021 and is now 45% repaired. CEFConnect positions the fund in the Loan sector whereas we have it as a Multi-sector CEF.

The Loans sector positioning is undoubtedly doubtful as financiers would be comparing it to funds that are mainly designated to loans. Multi-sector is perhaps the ideal location for it though it’s not best as numerous Multi-sector CEFs tend to assign to several kinds of credit sectors such as ABS, Agencies, investment-grade and high-yield business bonds, Treasuries, Munis and others – properties which ARDC mainly prevents.

Returning to DSL – what is the ideal sector for the fund? DSL is another difficult case in our view. The factor we do not see Worldwide Earnings as the ideal sector for the fund is that Global Earnings tends to stand in for non-US industrialized market bonds which DSL does not hold a lot of.

Approximately speaking, there are 3 worldwide bond sectors – United States, established non-US and Emerging Markets. Funds that mainly assign to EM bonds such as EDF or EDD being in the EM CEF sector as anticipated. Funds that assign to high or medium-quality bonds of G7 (and comparable) nations tend to be positioned in the Worldwide Earnings sector.

From its allotment, DSL might perhaps be positioned in the EM sector instead of Worldwide Earnings which tends to be a synonym for industrialized non-US. Nevertheless, its EM allotment is listed below 40% which recommends that it is much better referred to as a Multi-sector fund especially as it holds numerous other credit sectors such as loans, ABS, MBS and CLOs. This point is plainly arguable however either Multi-sector and EM are much better suitable for DSL than Worldwide Earnings.

DoubleLine

The effect of this conversation is two-fold. One, CEFs that can be completely positioned in their sectors are perhaps in the minority. Some sectors like Munis and Equity are relatively “tidy” from this point of view however numerous credit funds are less so. And 2, this suggests comparing funds within the sector is difficult as both efficiency and assessment might be affected by variations in allotment. Financiers ought to know an offered fund’s allotment profile and how it varies from its sector equivalents when assessing its metrics.

Market Commentary

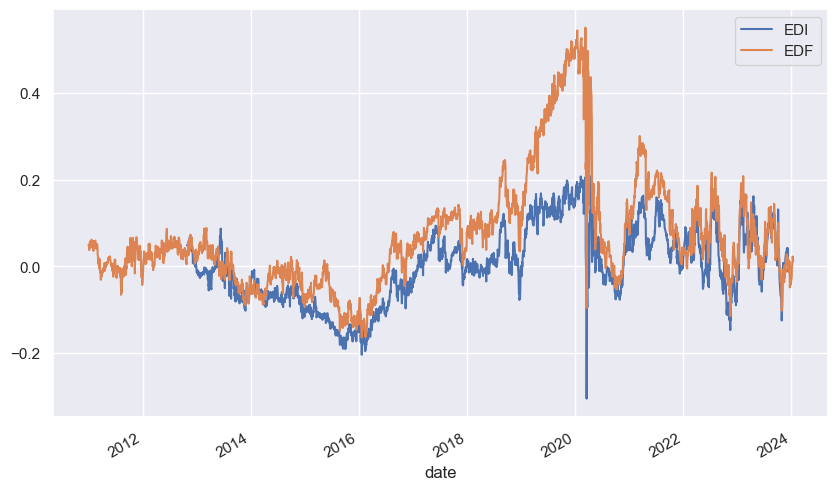

Last month 2 Virtus Stone Harbor Emerging Market financial obligation CEFs – ( EDI) and ( EDF) – combined with the latter being the enduring fund. The 2 funds have actually been an useful curio in the area for numerous factors.

For one, they have actually tended to trade at really high premiums, investing much of their time at double-digit levels and seldom trading at discount rates. This is regardless of quite abysmal returns. For example, EDF has a 5Y overall NAV return of around no while its 10Y overall NAV CAGR is around 1%. A huge part of this pertains to the battles of the fund’s more comprehensive sector – hard-currency and local-current Emerging Market financial obligation – however a few of it is plainly due to the funds’ absence of alpha.

2, due to the fact that the funds’ EM financial obligation holdings are fairly high beta they have actually experienced serial forced deleveraging which consistently required the funds to offer low and buy-back greater, harming the NAV.

3, their low circulation protection highlighted the reality that the high circulation rates were unproven. Poor longer-term overall NAV returns, serial deleveraging and low circulation protection ultimately required the funds to cut their circulations a couple of times, pressing the premiums lower and securing long-term financial losses for holders.

Another curiosity is that, regardless of being almost similar funds, they have actually tended to trade at really various assessments. This pertained to really unusual circulations where EDF’s NAV circulation rate was much greater than EDI’s for no excellent factor. This triggered EDF to regularly trade at a greater premium than EDI – often leaving to a premium 25% greater than EDI.

Methodical Earnings

Undoubtedly this ultimately and completely remedied with the merger statement, additional penalizing financiers who believed they were getting a juicier yield.

Position And Takeaways

The current run-up in CEF efficiency has actually been great to see nevertheless we are not chasing after the rally. That stated, we continue to see worth in funds like the CLO Equity-focused Carlyle Credit Earnings Fund ( CCIF) and the credit and energy focused PIMCO Dynamic Earnings Technique Fund ( PDX) along with the Flaherty suite of favored CEFs like ( PFO) whose assessments have actually pressed out to double-digit levels. When the Fed starts with its policy rate cuts, PFO and its sibling funds ought to begin to reverse their previous circulation cuts.

Editor’s Note: This post covers several microcap stocks. Please know the dangers related to these stocks.