FluxFactory/E+ by means of Getty Images

I just recently composed an post describing the financial investment case for Kamada Ltd. ( NASDAQ: KMDA), a little maker of plasma-based pharmaceuticals. This is an all of a sudden fast upgrade following Kamada’s statement of a significant business arrangement

As discussed in my initial post, the anti-rabies drug Kedrab is among the primary sources of both income and development for Kamada. It is dispersed in the United States by Kamada’s bigger plasma peer Kedrion and has actually been among the significant development motorists for Kamada in 2022 and 2023.

Kamada has actually now revealed a growth of the circulation handle Kedrion that extends it for 8 more years and surprisingly likewise includes a minimum income warranty for the next 4 years.

The marketplace has actually responded extremely favorably to the statement of the prolonged handle the share increasing ~ 20% on the news. I can comprehend why: the income warranty efficiently secures a considerable part of the development I was basing my financial investment case for Kamada on. As such, it deserves investing a little time to take a look at the information.

Background on Kamada and Kedrion

Kedrab/Kamrab is an anti-rabies immunoglobulin plasma drug established by Kamada which they accredit to Kedrion in the United States (Kedrion is maybe the tiniest of the “big” plasma gamers and has a big portfolio of plasma-based treatments). Kamada produces Kedrab for offering to Kedrion and likewise markets it themselves in other parts of the world where it passes Kamrab.

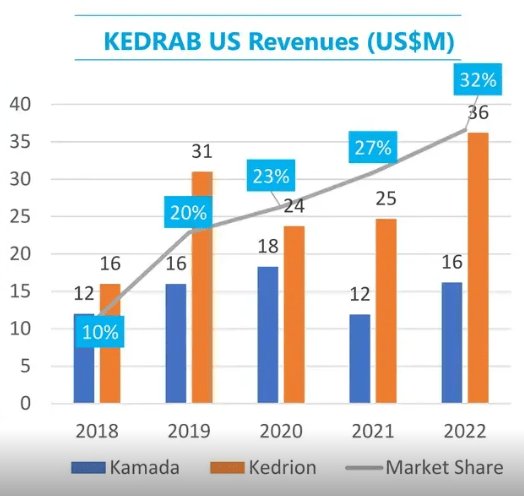

Kedrab is the present primary motorist of Kamada’s development in general. It created sales for Kamada of $16 million in 2022 (at 50% plus gross margin) and is on course to do substantially more than that in 2023. Management does not break out sales by item on a quarterly basis, however based upon commentary in incomes calls, Kedrab is the biggest development motorist presently.

Kedrab sales 2018-2022 (Kamada Financier Discussion)

The motorists for that development are several based upon commentary in Kamada’s incomes calls: a post-covid United States rebound in use, a contending item from Sanofi having actually been withdrawn from the United States market and Kedrab having a business benefit in being the only item clearly suggested for usage in kids.

Kedrion had actually just recently worked out an alternative to extend their United States circulation arrangement up until 2026, however this has actually now been changed with a more thorough growth of the partnership.

Information of the brand-new arrangement

The brand-new arrangement is set to begin at the start of 2024 and will run for a duration of 8 years. On a teleconference going over the statement, Kamada management discussed the offer has an alternative for an additional two-year extension.

Many intriguing is the truth that for the very first 4 years of the arrangement, Kedrion has actually dedicated to purchasing a minimum of $180 countless Kedrab from Kamada. Likely that $180 will not be equally divided over the 4 years, however to keep things easy, in the meantime, I’m presuming it will be.

That indicates $45 million annually of ensured Kedrab purchases by Kedrion from 2024 to 2027. As can be seen in the chart above, in 2022 Kedrion just purchased $16 countless Kedrab. While Kamada has actually suggested the 2023 number will be greater without divulging specifics (I’m presuming ~$ 25-30 million), $45 million annually still represents substantial extra development.

It is not completely clear why Kedrion and Kamada are so positive about ongoing development for Kedrab in the United States, however offered the warranty in the brand-new arrangement, it is to some degree now a theoretical issue just. Kamada management did discuss on the teleconference that Kedrion anticipates Kedrab to continue acquiring market share in the United States, albeit without defining if that is the primary motorist of the anticipated volume development.

Kamada management likewise stated on the teleconference that the brand-new arrangement has actually “enhanced monetary terms” and they anticipate their margins for Kedrab sales to Kedrion to enhance from the present ~ 50% gross margin without entering into specifics.

The statement likewise points out that Kedrion may begin offering Kedrab in nations aside from the United States. Kamada currently makes ~$ 6 million every year from offering Kedrab outside the United States, however it does not seem like this will be cannibalized. Kamada management stated at the conference the conversations with Kedrion have to do with locations where Kamada presently does not offer Kedrab, so any broadened geographical circulation through Kedrion would be genuinely brand-new income.

Lastly, the statement likewise points out Kamada’s Israeli circulation organization will begin marketing Kedrion items in Israel. No information were supplied and up until tested otherwise, I would anticipate the circulation organization to stay of little significance to the Kamada financial investment case (see my very first post for why I believe so).

Conclusion

My position on Kamada stays the same from my initial post. I discover the business to be underestimated for the mix of revenues and development available and rate it as a buy with a cost target of $7 (which is still ~ 20% upside from the present share cost).

The growth of the arrangement with Kedrion in my view substantially derisks the financial investment case. A big part of the development I was basing my financial investment case on is now actually ensured thanks to the brand-new agreement with Kedrion. I believe Kamada is well placed for a rerating by the market: the business has a beautiful balance sheet, is producing substantial capital, and can now include this arrangement on top.

Kamada now has actually 2 efficiently ensured income streams: ~$ 45 million every year at 50+% gross margin from Kedrab and ~$ 10-20 million every year in Glassia royalties which is pure gross earnings. At the minimum this limitations disadvantage threat.

If Kamada can likewise carry out similarly well for its other income streams, as explained in my very first post, I believe the marketplace will respond favorably. I anticipate to review my cost target when Kamada launches assistance for 2024, as I anticipate something greater than my present target of $7 can likely be warranted.