Tim Boyle

Intro

My routine readers understand that I am long-lasting bullish on the significant U.S. home enhancement merchants The Home Depot, Inc. ( NYSE: HD) and Lowe’s Business, Inc ( LOW). Nevertheless, in my very first post on HD stock in August 2022, I made it clear why I am not dismissing short-term discomfort and why the financial investment needs perseverance. In my last post, released in Might 2023, I went over 4 crucial ramifications of rate of interest for the 2 home enhancement merchants.

I still just have a relatively little position in HD stock (about 0.8% of my overall portfolio worth) and have not purchased the stock in a while. Nevertheless, with the stock under restored pressure due to the sharp increase in long-lasting rate of interest (the 30-Year Treasury briefly yielded 5.1% in late October) and the business reporting its third-quarter revenues next week on November 14 (pre-market), it’s a great time to re-evaluate.

In this upgrade, I’ll have a look at what financiers can anticipate from Tuesday’s upcoming revenues release and, more notably, whether I believe the stock is a buy provided the truth that it’s now trading fairly near to its 52-week low. To put the present share cost of $288 in point of view, I will provide an upgraded reduced capital appraisal (consisting of level of sensitivity analysis), taking into consideration the current sharp boost in the safe rate, and a multiples-based appraisal technique from a range of angles. I will likewise share my ideas on Home Depot’s dividend and elaborate on why financiers need to look beyond the simple truth that HD stock presently yields 185 basis points less than the 30-Year Treasury.

Did Home Depot Beat Profits Before And What To Anticipate From Q3 Profits?

The Home Depot has a history of beating the agreement quote for revenues per share (EPS). In the last sixteen quarters, price quotes have actually just been missed out on as soon as, in the very first quarter of financial 2020, which ended on Might 3, 2020 – in the middle of the early stage of the pandemic:

Figure 1: The Home Depot, Inc. (HD): Profits per share surprises on a quarterly basis (Looking for Alpha)

Nevertheless, typically, the business has actually beaten experts’ EPS agreement by more than 5%, which is an indication that management is rather conservative in its projections and is performing extremely well. Naturally, one might argue that revenues per share are rather simple to handle, however the business has actually likewise beaten price quotes for quarterly sales in 13 out of 16 quarters, or by +2.9% typically:

Figure 2: The Home Depot, Inc. (HD): Income surprises on a quarterly basis (Looking for Alpha)

I do not believe the strong performance history is exclusively due to the pandemic-related tailwind – after all, it was clear quite early on that the mix of lockdown steps and greater non reusable earnings (which was additional increased by stimulus checks) would benefit HD (and naturally LOW). In addition, the business’s performance history is likewise strong from a long-lasting point of view. Even on a two-year basis (as revealed by the FAST Graphs expert scorecard in Figure 3), experts have actually frequently undervalued the business’s revenues power. Over the previous 10 years, management has actually beaten revenues per share price quotes 58% and 42% of the time, respectively:

Figure 3: The Home Depot, Inc. (HD): Expert scorecard on a two-year forward basis (quickly Charts)

Offered this information, it is just sensible to anticipate management to report another revenues beat on Tuesday. The expert agreement for revenues per share is presently $3.78, down 11% year-over-year. Net sales are approximated at $37.7 billion, down 3% from the 3rd quarter of financial 2022. Modifications to EPS and earnings price quotes have actually stayed practically flat over the previous 3 months, while there were rather noticable unfavorable modifications in Might. Nevertheless, this is barely unexpected as the business reported a miss on same-store sales and reduced its full-year sales and EPS assistance throughout the very first quarter revenues call.

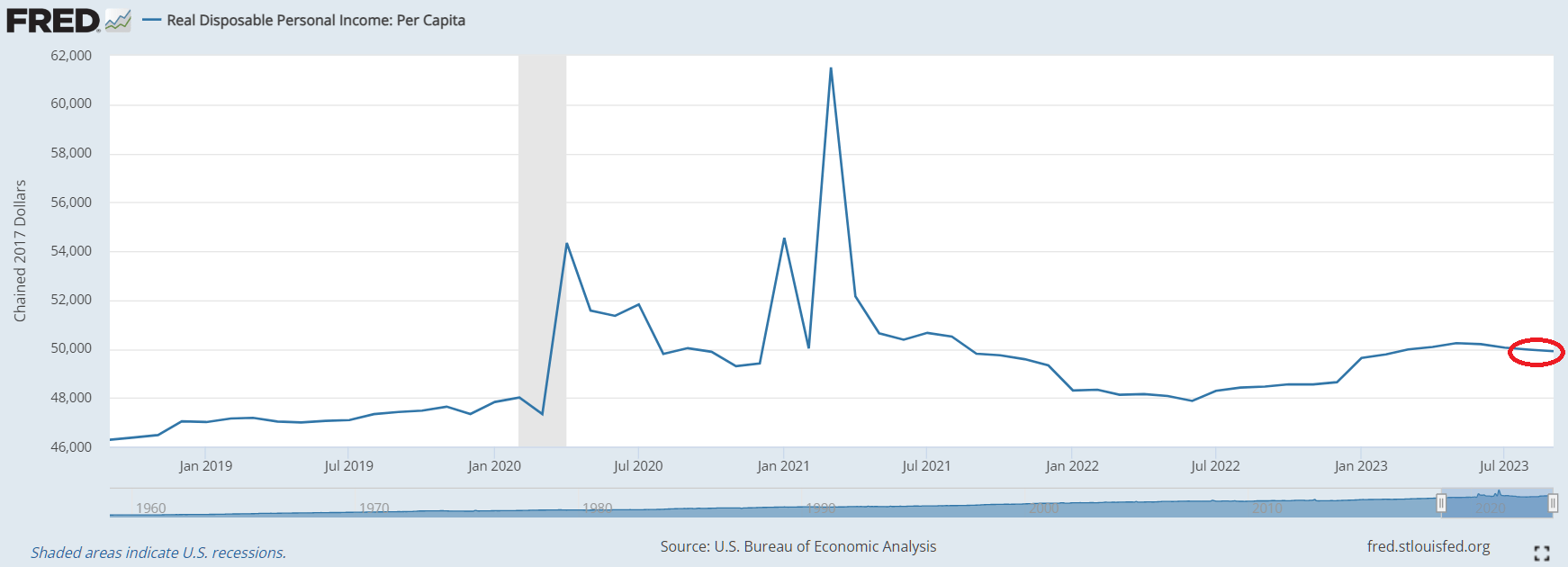

With this in mind, one might conclude that it is excessively dangerous to purchase HD stock ahead of the revenues release. Nevertheless, provided the truth that customer self-confidence has actually continued to increase given that the July 2022 low, I believe it is most likely that management under-promised a bit in the FQ1 2023 revenues statement. Apart from that, the minor decrease in genuine non reusable earnings per capita in the 3rd quarter of HD’s (validated by the increase in a number of CPI classification signs) might indicate a minimum of “viewed” greater inflation and for this reason possibly weaker quarterly sales efficiency at HD.

Figure 4: Genuine non reusable individual earnings on a per-capita basis (U.S. Bureau of Economic Analysis, Real Disposable Personal Earnings [DSPIC96], recovered from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/DSPIC96, November 8, 2023)

It reveals as soon as again that it does not make much sense to overanalyze things, specifically as a long-lasting financier. Personally, I believe a dive in the share cost is most likely than a fall due to the anticipated revenues beat, however I truthfully do not believe it makes much distinction whether the stock is purchased today’s cost or at a somewhat greater cost after revenues. Thinking about that The Home Depot is a really reputable home enhancement seller with a strong financial moat that is really successful and frequently produces strong excess returns on invested capital, it is challenging to refute the quality of the financial investment per se (see my previous posts).

A Word On HD Dividend Versus The Background Of Greatly Increased Safe Rates

From a historic point of view, HD’s present dividend yield looks rather appealing. A dividend yield of 2.9% is considerably greater than the five-year average of 2.3% however is naturally overshadowed by the present safe rates of interest of long-lasting federal government bonds. However, financiers need to not straight compare a stock’s dividend yield with a bond yield for a number of factors.

The dividend yield (on expense) usually increases with time, offered one purchases premium business with shareholder-friendly management and board of directors. I believe this is definitely the case with The Home Depot, which is exceptionally effectively run, has a well-thought-out footprint, and has oligopolistic propensities. In this method, stock financiers who depend on dividend earnings (now or in the future) have intrinsic inflation defense ( see my post here on a typical misunderstanding). If a business has the ability to dependably grow its dividend above the rate of inflation, it implies that the acquiring power of earnings really increases with time – something that is not possible with standard bonds.

Even presuming a rather conservative dividend development rate of 3% annually (HD’s long-lasting dividend CAGR remains in the high teenagers), the yield on HD shares bought today would surpass the yield on the present 30-year Treasury after 16 years (Figure 5, blue). The cumulative earnings (before taxes – bear in mind that dividends are possibly taxed more positively compared to bond discount coupons) would have to do with the exact same after thirty years, however it is necessary to keep in mind that stock financial investments bring no reinvestment threat.

In a more positive circumstance, presuming HD’s dividend grows by 5% a year (Figure 5, gray), financiers will make 35% more cumulative earnings over thirty years than those purchasing the 30-Year Treasury.

Figure 5: The Home Depot, Inc. (HD): Theoretical dividend yield on expense compared to the present yield on the 30-Year Treasury (own work, based upon business filings and information from treasury.gov)

Furthermore, typical stocks are the only ones amongst the standard possession classes that are “efficient”. So if the business’s principles stay undamaged, revenues grow and the business does not pay all its revenues, the share cost need to likewise increase, resulting in basically substantial capital gains in addition to dividend earnings.

Nevertheless, it is necessary to bear in mind the noticable volatility of stocks and the associated essential threat capability (monetary side) and threat tolerance (mental side), along with the in-principle discretionary nature of dividend payments. Naturally, I do not wish to be misinterpreted as a challenger of bond financial investments.

HD Stock – A Strong Buy Under $300?

Beginning with an evaluation from an earnings-per-share point of view, HD stock presently trades at 18.5 times mixed revenues, taking into consideration the most just recently reported revenues and the agreement for the approaching quarter. That’s definitely not low-cost for a business that eventually runs an intermediary’s company, however provided HD’s high earnings margins, outstanding return on invested capital, and the truth that it runs in what can be thought about an oligopoly, I believe some premium is warranted. It’s likewise worth bearing in mind that Home Depot’s revenues have actually grown at a typical yearly rate of 11% over the last twenty years, which relates to a PEG (price-to-earnings development) ratio of 1.7 – once again, not low-cost, however not actually costly either. If we presume that the marketplace continues to award HD stock a premium revenues numerous, a financial investment at a cost of $288 today would imply an annualized return of 8% if expert price quotes are appropriate (which is not an impractical expectation provided the exceptionally strong performance history, see above):

Figure 6: The Home Depot, Inc. (HD): FAST Graphs chart, based upon adjusted operating revenues per share (quickly Charts)

That stated, I stay rather mindful about anticipating HD stock to continue to trade at a considerable premium – after all, the typical revenues numerous at which the stock altered hands in between 2002 and 2015 was around 17, and let’s not forget that low or perhaps no rate of interest have actually offered a tailwind in the past. If expert price quotes for Home Depot’s revenues over the next 2 years show to be fairly precise and the marketplace numerous agreements to a worth of 17, HD stock would represent basically “dead cash” if one were to purchase it today for $288 (Figure 7).

Figure 7: The Home Depot, Inc. (HD): Forecasting chart, based upon adjusted operating revenues per share and a several contraction to 17x revenues (quickly Charts)

Likewise, taking into consideration the dominating rates of interest environment over the previous 10 years, Figure 8, which compares numerous appraisal multiples with their long-lasting averages, recommends that HD shares are relatively valued today:

Figure 8: The Home Depot, Inc. (HD): Multiples-based appraisal (own work)

From an affordable capital (DCF) point of view, HD stock does not look like a deal either. Personally, I believe an equity threat premium of 4.0% is sensible for a financial investment in a business like The Home Depot. Considered that a long-lasting safe rate of 4.75% can presently be secured for thirty years, my expense of equity for HD stock is 8.75%. Figure 9 reveals the outcomes of a DCF estimation, recommending that it is somewhat misestimated today (reasonable worth of $266). The appraisal is based upon the short-term complimentary capital approximates according to FAST Graphs/FactSet. Nevertheless, stock-based settlement (SBC) has actually been subtracted from these figures, as management will eventually require to invest complimentary capital to balance out the dilution from efficiency shares approved. That being stated, SBC at The Home Depot need not be over-interpreted considered that it just represents roughly 2.1% of unadjusted operating capital (financial 2017 to financial 2022 average).

Figure 9: The Home Depot, Inc. (HD): Marked down capital analysis (own work, based upon business filings and own computations)

Nevertheless, thinking about that the DCF design is considerably depending on money streams far in the future (weighting the terminal worth at 56% of the amount of reduced capital), it makes good sense to carry out a level of sensitivity analysis. Undoubtedly, such a technique does not take into consideration the short-term price quotes, however I would argue that this is a “incorrect accuracy” anyhow provided the substantial weight of the far in the future capital.

With a standard complimentary capital of $17.0 billion for financial 2023, the marketplace presently anticipates The Home Depot to grow its complimentary capital in eternity at a rate of 3.2%, presuming an expense of equity of 8.75%. As displayed in Figure 10, the appraisal of HD stock is extremely conscious the indicated development rate.

Figure 10: The Home Depot, Inc. (HD): Marked down capital level of sensitivity analysis (own work, based upon business filings and own computations)

Offered the long-lasting typical complimentary capital development rate of 11% (average for financial 2004 to financial 2022, Figure 11), a continuous development rate of 3.2% naturally sounds really conservative. Nevertheless, bear in mind that home enhancement merchants have actually benefited enormously from the low-interest rate environment and typically low inflation after the Great Economic downturn, along with from combination. I extremely question that a low double-digit (or perhaps high single-digit) complimentary capital development rate can be sustained in eternity.

Figure 11: The Home Depot, Inc. (HD): Free capital, after changes for stock-based settlement and working capital motions (own work, based upon business filings and own computations)

Conclusion

The Home Depot, the U.S. home enhancement heavyweight with present yearly sales of around $155 billion, will launch its third-quarter outcomes on Tuesday, November 14, before the marketplace opens. Offered the business’s strong performance history in the past and management’s propensity to under-promise and over-deliver, I believe a revenues beat on Tuesday is highly likely – likewise provided the truth that projections were cut previously this year and macroeconomic principles do not look regrettable. Nevertheless, it’s too simple to get brought away and overanalyze things.

In the long run, purchasing HD stock a couple of percent more costly or less expensive does not make much of a distinction. Thinking about that The Home Depot is a really reputable home enhancement seller with a strong financial moat that is really successful and frequently produces strong excess returns on invested capital, it’s tough to refute the quality of the financial investment itself.

From a dividend point of view, it is likewise crucial not to just compare the present dividend yield with the rate on long-lasting federal government bonds (or premium business bonds). It is sensible to presume that HD will have the ability to continue to grow its dividend at a healthy rate, so the created earnings needs to ultimately go beyond that created with a long-lasting bond financial investment. This is a crucial factor to consider from the point of view of keeping (or much better increasing) the acquiring power of one’s dividend earnings. In addition, one need to think about the possibly more beneficial tax treatment of dividend earnings along with the absence of reinvestment threat when purchasing stocks.

From an evaluation point of view, I believe it would be an overstatement to call HD stock misestimated at listed below $300. Shorting the stock at this level would be a substantial bet on the collapse of the U.S. real estate market as rate of interest continue to increase, loan defaults skyrocket and existing house owners struggle with constantly weak non reusable earnings. As I have actually mentioned in my previous posts on home enhancement merchants along with homebuilders Lennar Corp ( LEN, LEN.B) and KB Home ( KBH), I think the long-lasting principles are undamaged and I can not visualize such a strong unfavorable circumstance.

Although my position in HD is still rather modest at just 0.8% of my overall portfolio worth, I am not aiming to contribute to my position ahead of revenues. I remain in no rush to contribute to my position provided the tense environment, and I understand that from a long-lasting point of view, purchasing a somewhat greater or lower cost will not make much of a distinction. I think that the stock exchange presently provides much better chances in other places (pharmaceuticals, tobacco stocks, and picked defense business), however I might see myself increasing my direct exposure to home enhancement merchants before completion of the year. I for that reason rate HD stock as a moderate buy.

Thank you for putting in the time to read my most current post. Whether you concur or disagree with my conclusions, I constantly invite your viewpoint and feedback in the remarks listed below. And if there’s anything I need to enhance or broaden on in future posts, drop me a line also. As constantly, please consider this post just as an initial step in your own due diligence.