georgeclerk

Financial investment rundown

Markets turned in practically vertical style after the Fed’s choice to pause its rates treking cycle in the November FOMC conference. This was the second time the committee chose to stop briefly tightening up monetary conditions because July. Financiers fasted to alter their threat cravings following the statement, moving the character of U.S. markets, and some international indices.

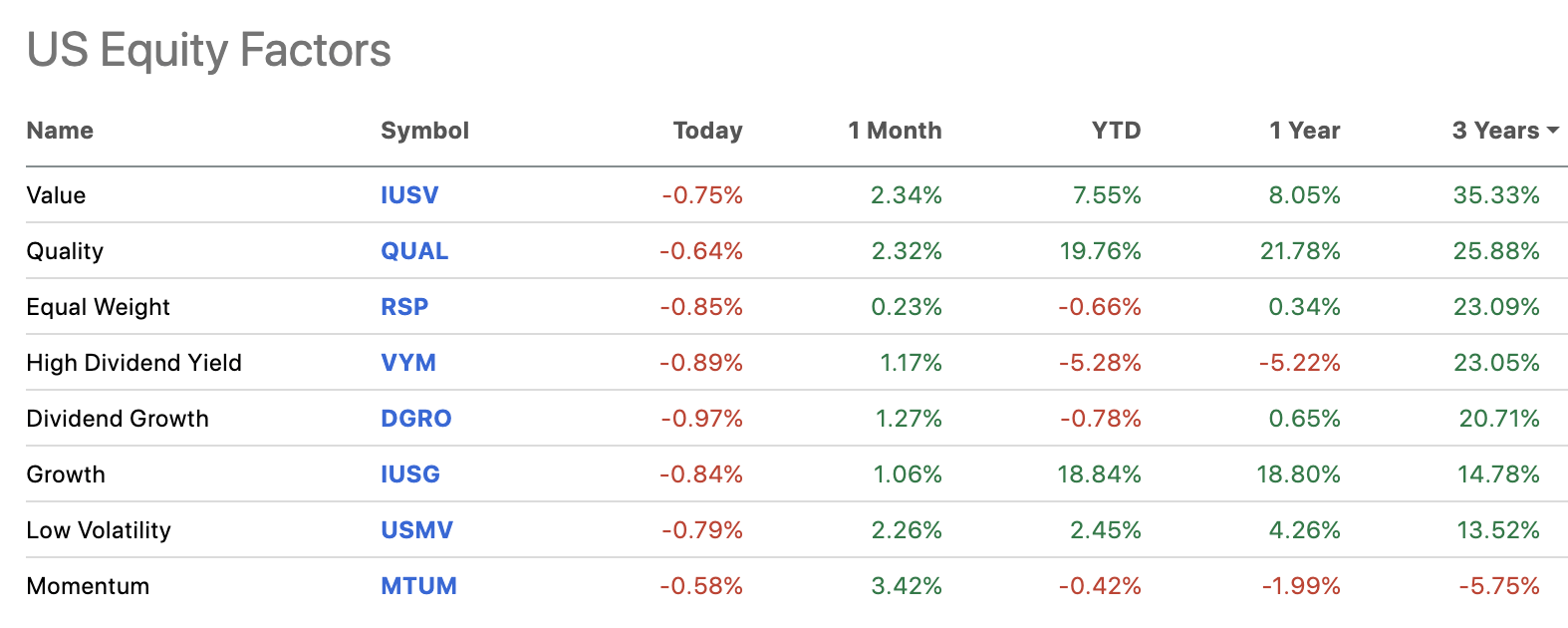

The snap-back rally was led by high beta and tech names (there is overlap in between the 2) however the majority of equity aspects + sectors have actually captured the quote in November, with market value in a duration of possible much better company in the coming 12-24 months. Seriously, the turnaround was short-term in lots of circumstances. This once again opened the dispute of “worth vs. development”, with the previous showing remarkable efficiency on a 3 year basis, however lagging this YTD (Figure 1). Nevertheless, one need to acknowledge much of this dislocation is driven by the efficiency of the “stunning 7” business leading the benchmark indices.

So the dominating concerns are 1) where to from here, and 2) how most likely are financiers to raise the quote on worth aspects progressing?

Figure 1. U.S. equity aspects, ranked by 3-year efficiency

Source: Looking For Alpha

The other consider contention is size. Big caps and mid caps have actually frequently outshined little cap peers in times of turbulence. However the mid cap area is still loaded with lots of deals. It’s simply whether these show analytical discount rates, or, whether the marketplace has actually got it best in these circumstances.

For financiers looking for varied direct exposure to both worth aspects and mid-cap equities, The Lead Mid-Cap Worth Index Fund ETF Shares ( NYSEARCA: VOE) is a holding to think about in the equity threat budget plan.

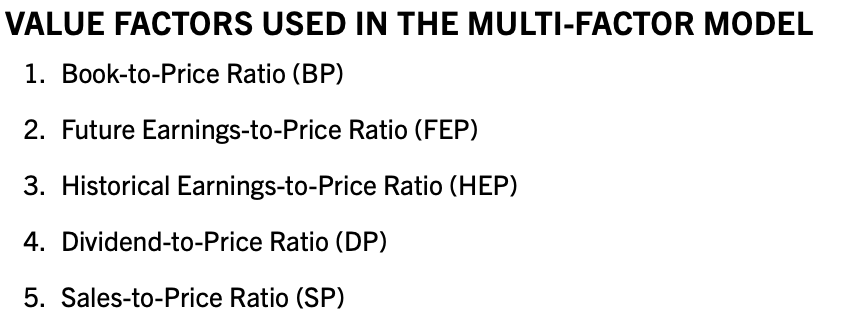

The fund tracks the CRSP United States Mid Cap Worth Index utilizing a duplication method to match this standard as carefully as possible. According to CRSP, the index is built utilizing a composite of multiples/ratios utilizing a “ composite rating a rank worth” to approximate choices and weightings. These are seen in Figure 2.

Figure 2.

Source: CRSP

The duplication method and tight direct exposure to a composite of worth aspects has numerous advantages, not in the least catching threat premia versus the present market cycle.

In spite of these truths, VOE hasn’t carried out along with other worth funds (both mid cap and blended mix of size) in current times, provided specific dangers Particularly:

- 1-year and 3-year tracking mistake of 9.8% and 8.6% respectively, positioning it in the 20th and c. 50th percentiles vs. all ETFs respectively,

- Annualized volatility of 15.7% at the time of composing,

- Turnover of around 18%, suggesting capital is turned out of carrying out names into under-performing names with more ‘appealing’ ratios in the composite.

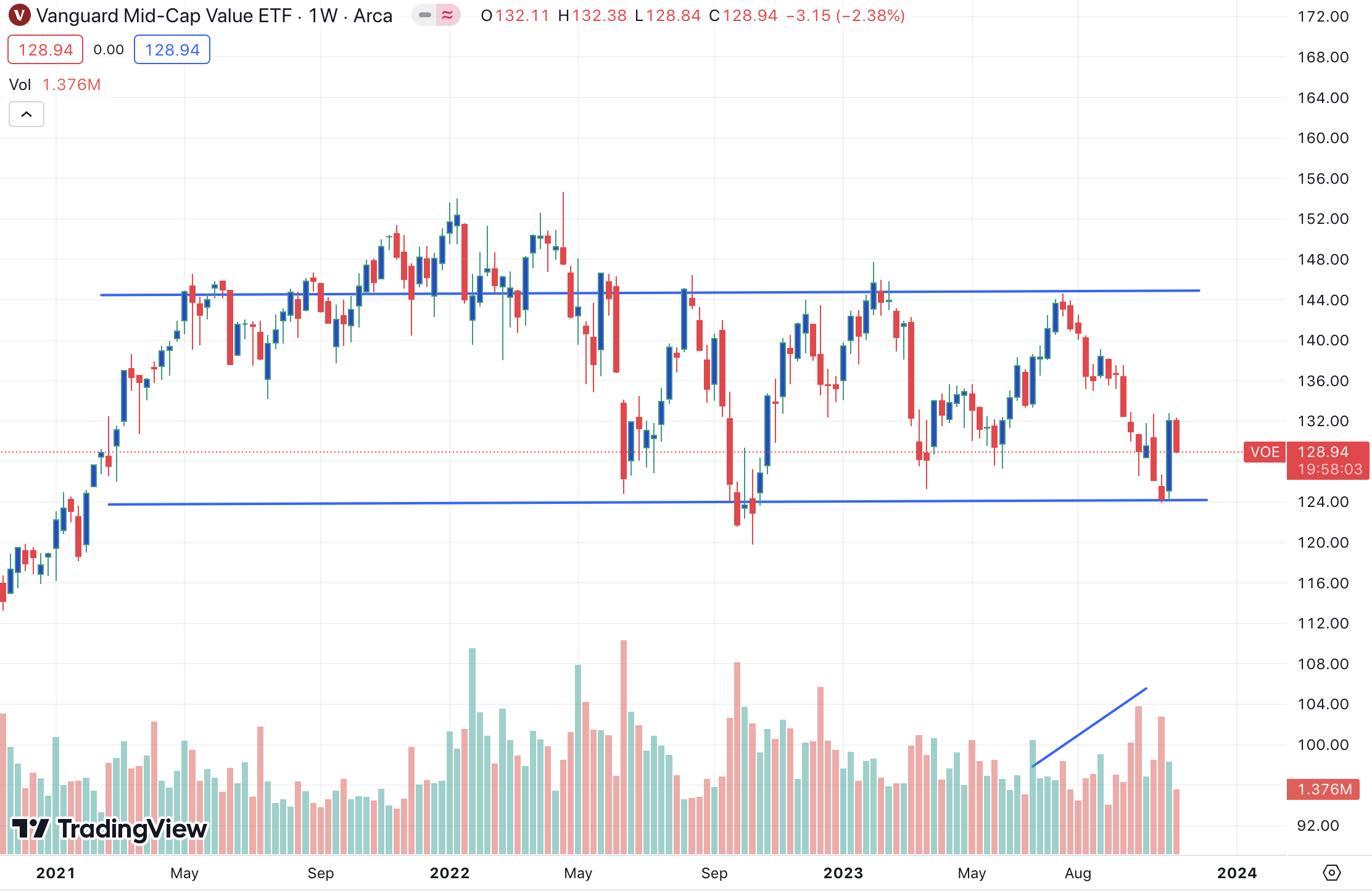

As an outcome, the fund has actually lagged equivalent names, such as IUSV ( IUSV) which buys market capitalizations’ of all sizes.

Figure 3.

Source: Tradingview

Figure 3a. VOE long-lasting cost development, 2021-date

Source: Tradingview

Still, VOE is extremely varied and has direct exposure to low-beta sectors which might decrease drawdowns and assist risk-adjusted returns for equity portfolios. It has 197 holdings divided throughout a variety of sectors, with financials (18%) and industrials (14.5%) taking one of the most weight, and innovation and customer cyclicals holding 8-8.5% of the portfolio respectively. The leading 10 holdings comprise around 12.4% of the portfolio’s overall weight.

Dividends, paid quarterly, total up to $3.38/ share in the TTM, yielding 2.5% as I compose. The fund has almost $25Bn in AUM, charging an expenditure charge of simply 7bps on this, positioning it in the 85th percentile vs. all ETFs.

The yield on expense and diversity concepts utilized by VOE do not conquer the reality it is lagging equivalent peers, specifically on the development side of the book. With financiers firing up a brand-new flame of threat cravings in U.S. markets, my judgement is that VOE will continue to lag its equivalents, which financiers might be much better served in looking for more selective chances somewhere else.

Because vein, my suggestions throughout all 3 financial investment horizons are as follows:

- Short-term (coming, 12 months) – Neutral; beginning assessments aren’t pricey however aren’t always inexpensive either at 15x revenues and the 2.5% dividend yield. The fund’s momentum aspects are missing. Momentum will be a crucial element for equity rates over the coming 12 months in my view.

- Medium term (1-3 years) – Neutral; Whilst I am positive on the mid-term outlook for U.S. equities on aggregate, those names with remarkable development economics are much better placed to capture the quote in my viewpoint. This positions a dampener on mid-cap worth proposals such as VOE.

- Long-lasting (3 years+) – Neutral; Comparable to the above. Here it ends up being more an argument of chance expense vs. more selective names with more appealing economics that comprise the fund’s constituents.

Net-net, provided the conclusion of aspects gone over in this report, I rate VOE a hold.

Talking points

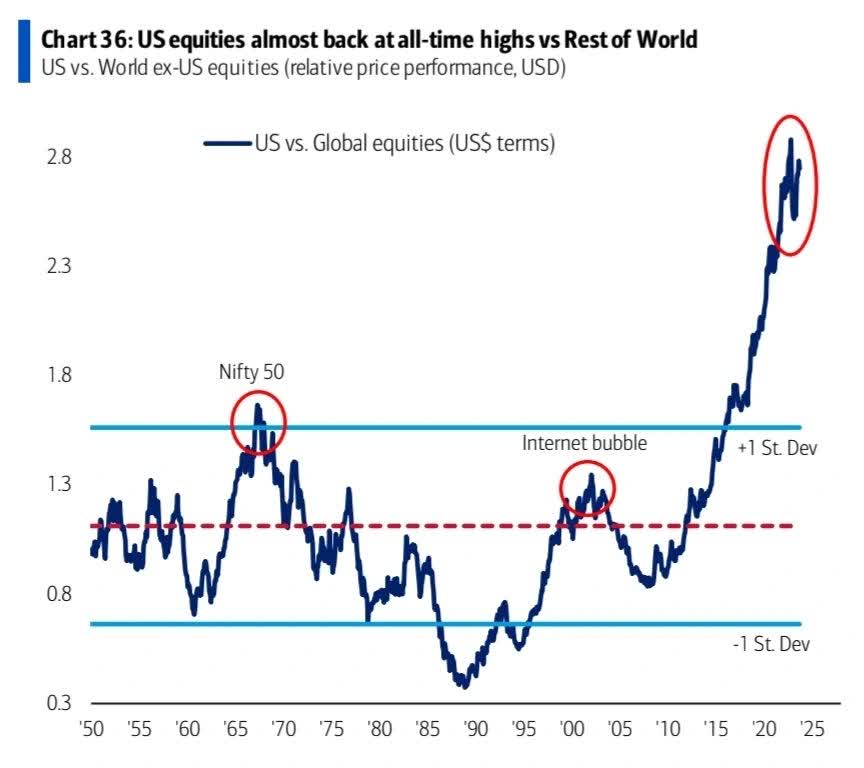

- Financiers still bidding U.S. equities greater based upon basics

As seen in Figure 4, U.S. equities are at all-time highs vs. international peers in regards to stock returns. Because 2013, this space has actually broadened at an increasing rate. One may question the credibility of this progressing however the truths are clear based upon economics.

For one, U.S. GDP drew in at 4.9% annualized last quarter, and according to a UBS report, U.S. customers remain in good condition, revealing “customer strength”. In a different note, the financial investment bank reported that Q3 revenues plainly highlight that noted business remain in similarly as leading shape progressing.

” It’s clear to us that the revenues economic downturn is over as revenues are set to grow for the very first time in 4 quarters”, it stated.

In aggregate, revenues are beating by 5.5% and business earnings are on speed to grow by 4%- in line with our preliminary expectation of 3-4% development.

Although the 4Q23 S&P 500 EPS quote has actually been modified lower, it hasn’t deviated considerably from the historic pattern after representing some non-recurring products”.

Second Of All, FactSet reports that Q4 this year, the mean of Wall Street expert approximates YoY revenues development of ~ 4% and incomes to grow by 3.5%. For FY’ 24, agreement approximates projection ~ 12% revenues development and 5.5% in sales upside.

As a result, despite the fact that U.S. equities are still priced at a premium to international peers, in my judgement this shows the marketplace’s view on the continued outperformance of the U.S. vs remainder of the world. This is an useful point for VOE. It supports the reality that it might continue to stay appealing for value-orientated gamers progressing.

Figure 4.

Source: Bank of America

- Beginning assessments stay a talking point in between worth vs. development

For what it deserves, VOE is priced at a relative discount rate to large-cap peers in the benchmark indices. The fund trades at ~ 15x revenues, behind the S&P 500 index’s 17.8 x forward revenues numerous as I compose. Nevertheless, it is still above the classification avg. of 11.4 x, and above FactSet’s section average of 11.4 x too. Coming 12-month returns are greatly affected by beginning multiples, and beyond that, sales and revenues development is the significant lever. So the belief is blended here in my analysis. On the one hand, you have actually got VOE fairly priced, however not at a significant discount rate. On the other, you have remarkable basics watching out 12 months or two in the big cap area, with multiples a couple of points ahead of the curve. Without a broad evaluation detach, my financial investment cortex is not shooting for VOE provided (i) its current efficiency in trending markets, and (ii) potential customers for development in higher-growth locations of the marketplace. Because vein, the fund’s low weighting to tech and other cyclicals might serve to be a relative hinderance.

Figure 5.

Source: Goldman Sachs Financial Investment Research Study

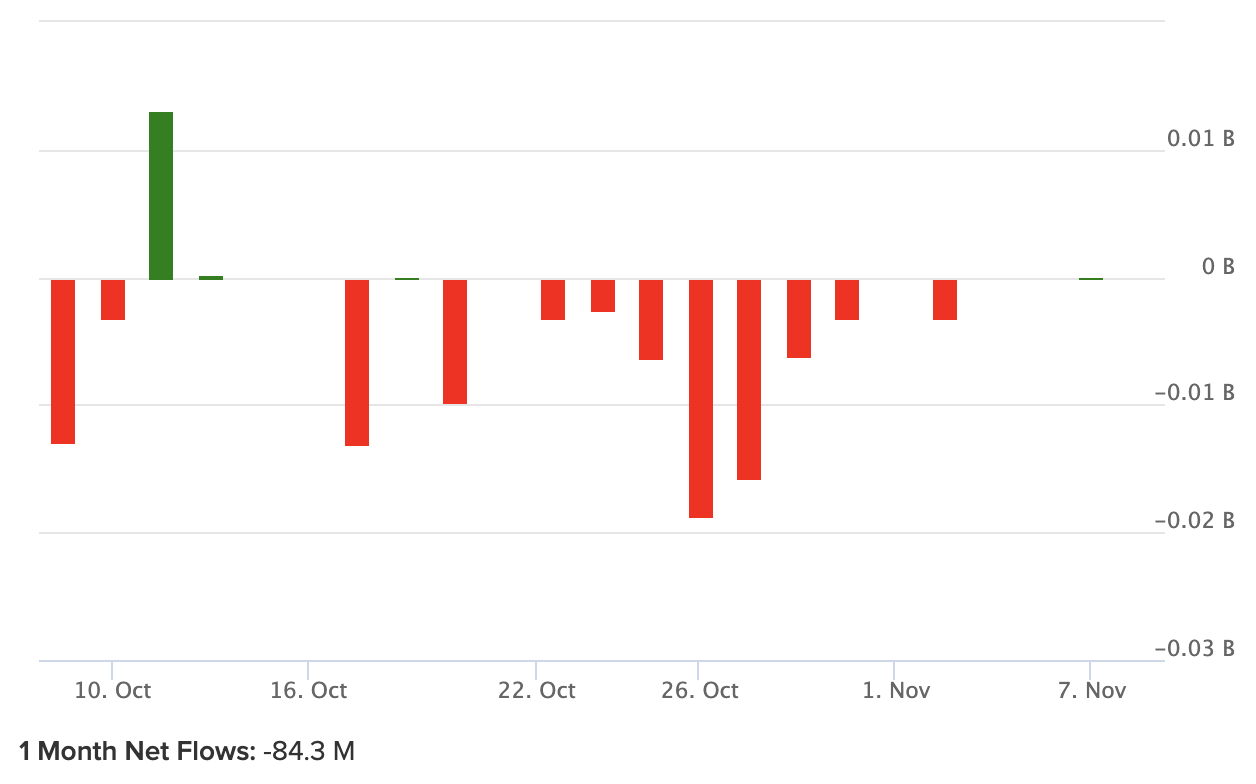

- Fund streams a weakening element

Connected to the point above, capital streams into/out of VOE has actually been weak in the last 12 months. If financiers remained in reality purchasing mid-cap stocks at little discount rates, then I ‘d anticipate to see more favorable circulations into VOE to represent this.

Rather 1-month net circulations are unfavorable $84mm as I compose, and financiers have not raised the quote on VOE in the middle of the current snap-back rally in equities. To me this suggests 2 things:

( 1 ). Financiers do not value the fund’s capability to intensify wealth, and

( 2 ). Financiers are assigning to more selective chances somewhere else.

We can’t ignore these concepts. Rather, we need to accept the cash streams, and regard the reality things have actually altered in the financial investment dispute for big caps and development names. This supports a neutral view on the fund.

Figure 6. VOE 12-month fund streams

Source: VettaFi ETF Database

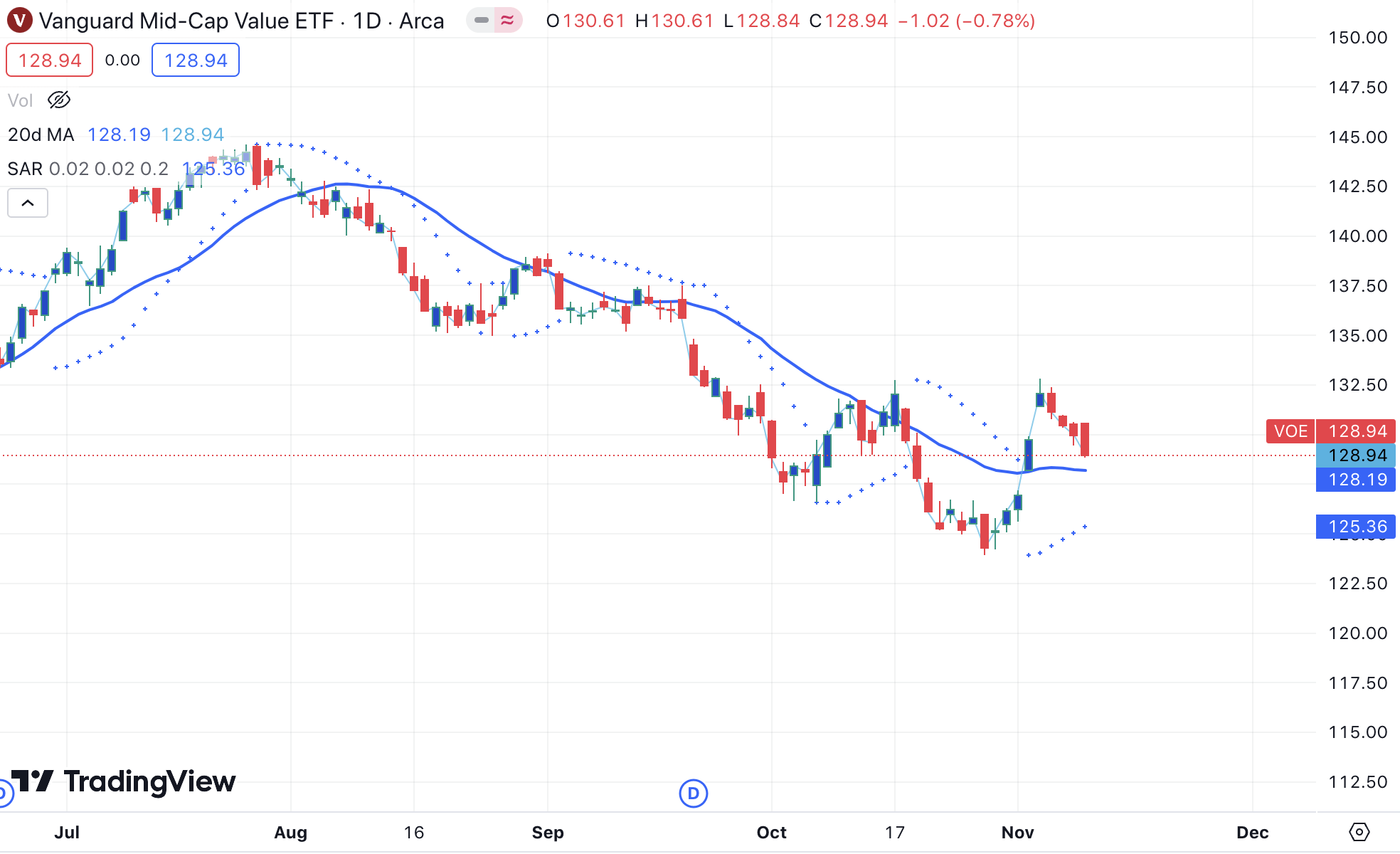

Technical aspects for factor to consider

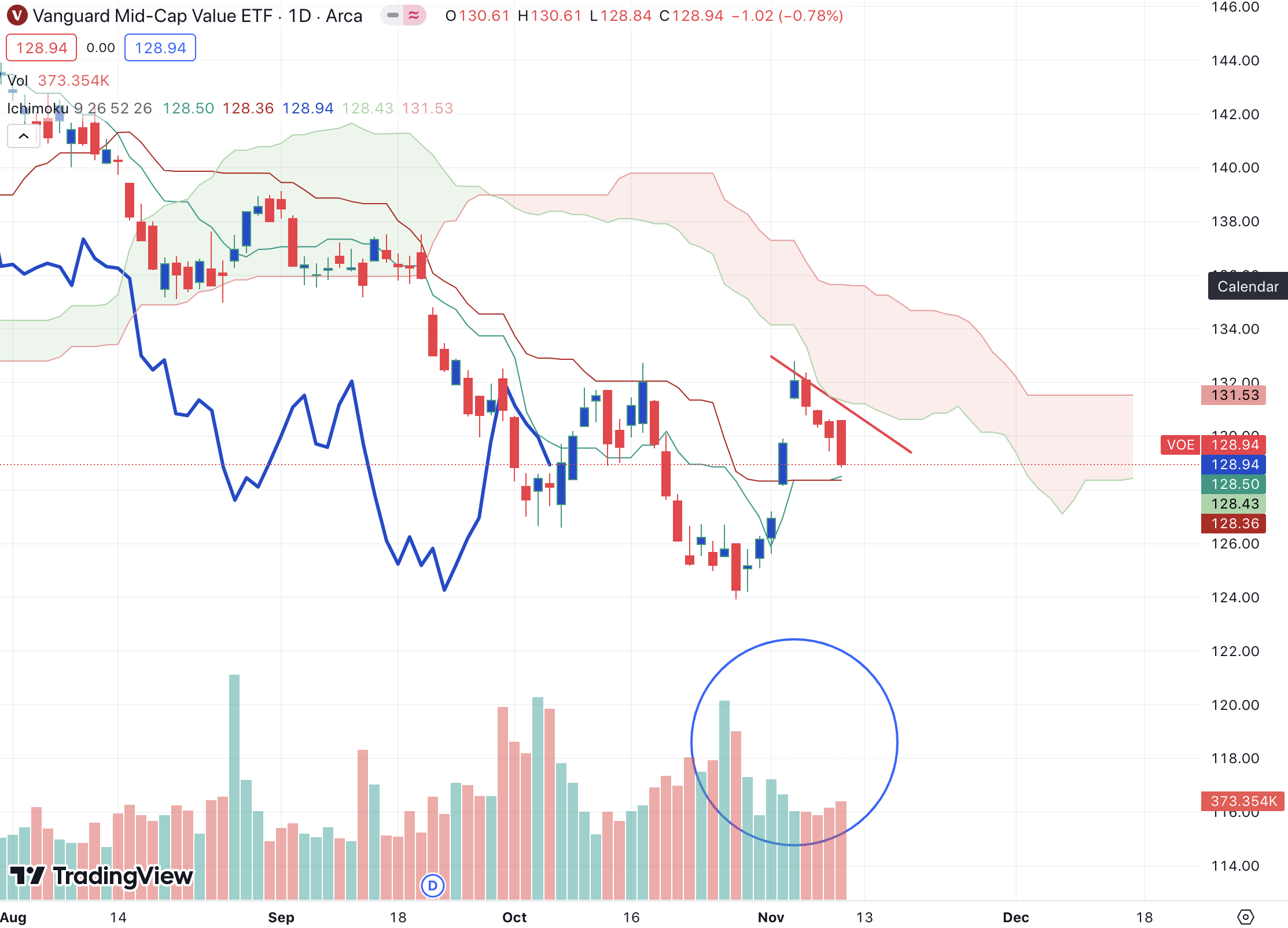

1. Relating to momentum

The current cost action in VOE has actually left lots of benefits on the table in my viewpoint. It gapped above its 20DMA this month however has actually backtracked towards this level in subsequent days. The Parabolic SAR has actually revealed a short-reversal, however absolutely nothing exceptional to show the fund will continue its variety extension greater. We are now in line with October variety once again.

Figure 7.

Source: Tradingview

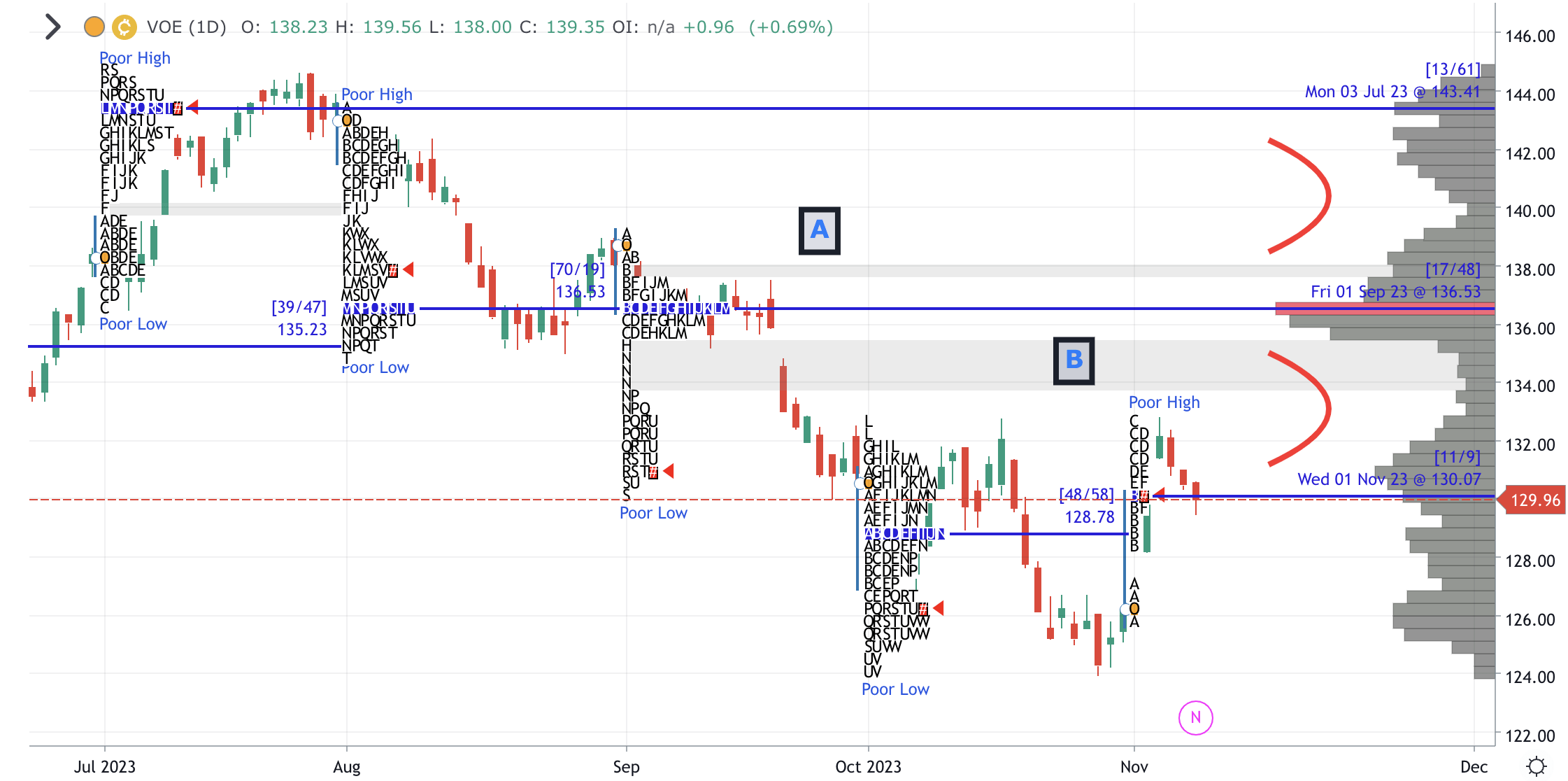

2. Alter, Cost circulation

Observations: There are 2 pockets of low use in the $134s and the $140s. Both consist of single print vacuums at A and B, which might bring in cost even with the current pullback. However we can’t neglect the underdeveloped ledge forming at the $128-$ 129s either. Financiers seem filling this ledge to match the remarkable ledge as I compose. This location might be have cost control till the ledge is matched, before financiers choose to fill the low use pocket from $132-$ 136. This is a multi-modal circulation with numerous peaks, sporting the concept of additional sideways trade.

Secret levels: Financiers must view the $128-$ 129 area carefully as we might turn around this location to finish the ledge to match it to the one above. On the advantage, $135 is considerable, whereas anything listed below the $128s on the drawback is a soft result for the name.

Actionable technique: The bell curve is not yet formed to show cost approval, so there might be additional competitors around the $129s. Variety trade is for that reason supported vs. a directional view.

Figure 8.

Source: Go charting

3. Directional predisposition of patterns

Pattern action is plainly blended for VOE, evidenced in the following 3 charts.

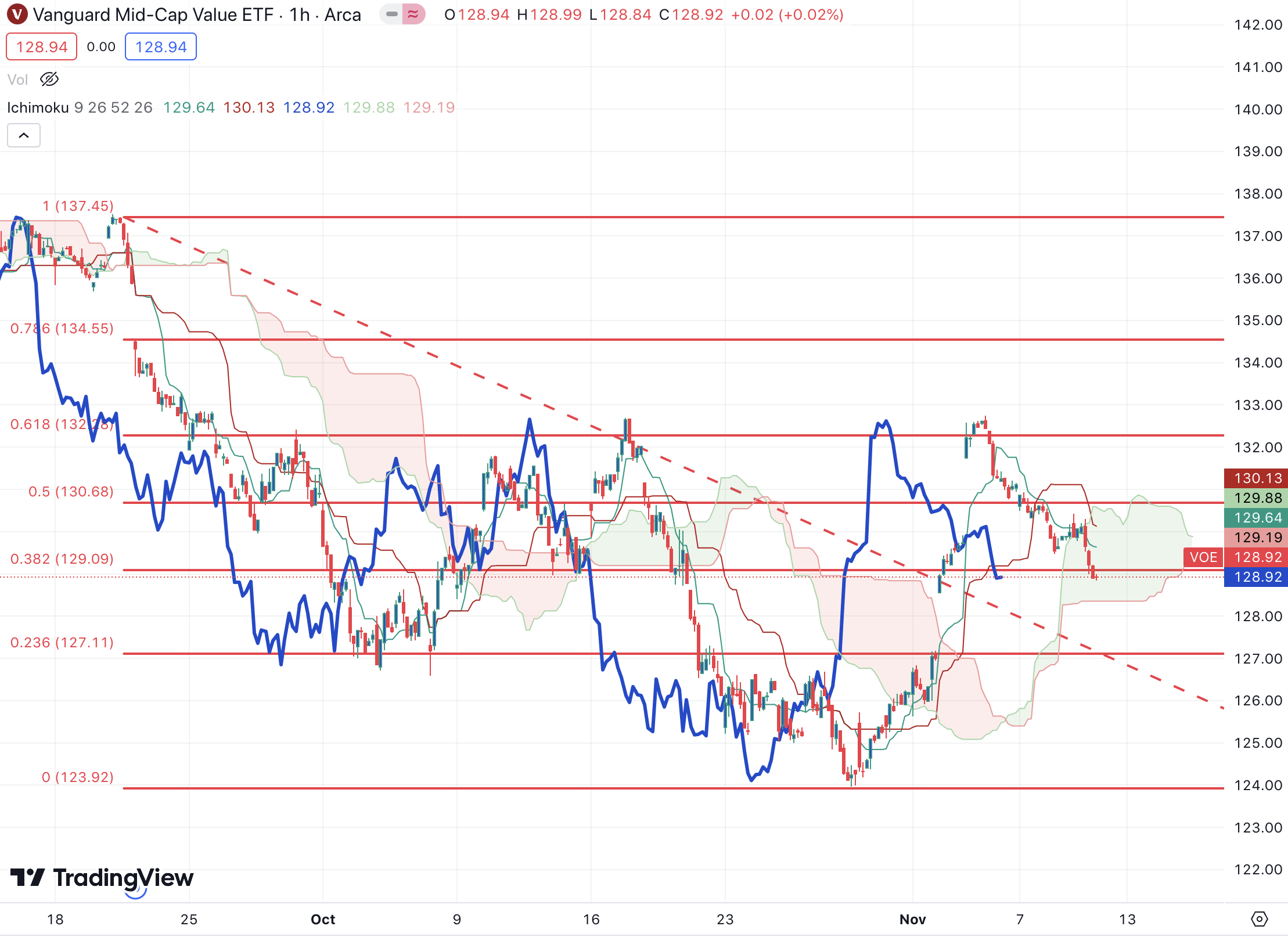

Figure 9 Short-term (60-minute chart, wanting to coming days)-

- Pressing back into the cloud, with both cost and delayed line in countertrend to the bullish cloud. Turning line and conversion line are now down dealing with, suggesting the momentum turnaround.

- We took the October high and after that sold greatly, likely an institutional seller. This is not unexpected, seeing that (a) VOE was greatly offered in October, and (b) financiers most likely took capital off the table when this level was reached when again.

- Tracing the fibs from the September high, we took the 61.8% mark at $132s before advancing south once again.

Secret levels: $127 is the next level on the drawback to keep an eye out for. Taking this, we ‘d be far less positive. On the advantage, $129-$ 132 are the crucial levels to regain.

Source: Tradingview

Figure 10. Medium-term (day-to-day chart, wanting to the coming weeks)-

- Plainly screening + declining the cloud base with the last 4 days of trade. Evening star development suggested the turnaround as purchasing volume dried up as the relocation started to remove.

- We closed the second cap greater with this bearish turnaround and are now evaluating the marabuzo line at $128.

- Seeking to cross the turning + conversion lines with another decrease.

Secret levels: The cloud is coming down from $128-$ 126 throughout the course of November-December, so this is the crucial level to break. If it does not, we might evaluate the $124 lows. On the advantage, a break to the $130-$ 132s by December would have us above the cloud, however the delayed line has more to do.

Source: Tradingview

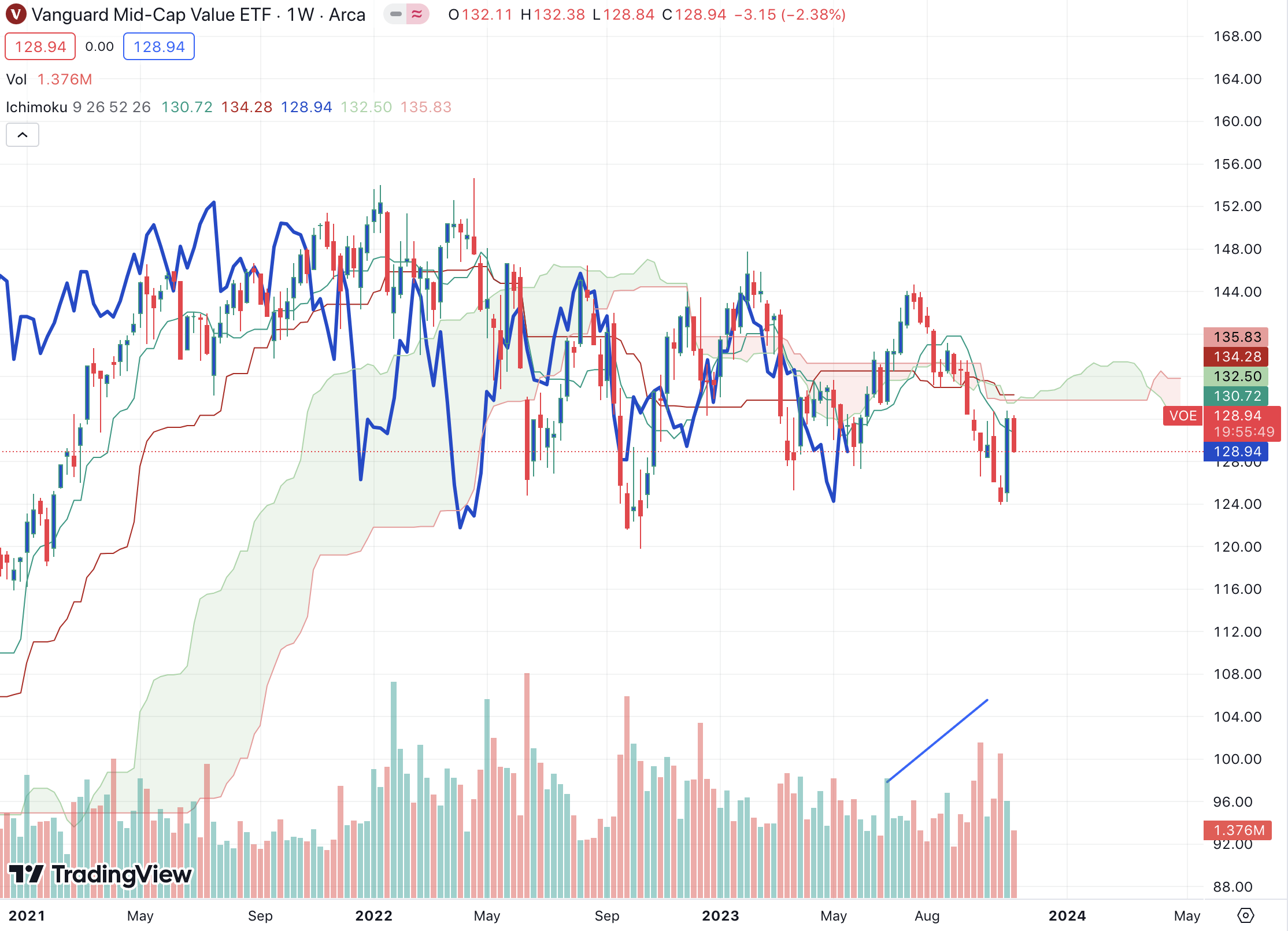

Figure 11. Long-lasting (weekly chart, wanting to coming months)-

- Rangebound trade from bulk of ’23 looks set to continue with blockage around $128-$ 135. Cloud pinch this month minimizes quantity of work required, however momentum simply isn’t there.

- The bullish swallowing up candle light of recently hasn’t contributed to require, in spite of securing the last 5 weeks variety.

- Offering volume still extremely high, purchasers aren’t provide today.

Secret levels: $135 on the advantage, $124 at the previous short on the drawback.

Source: Tradingview

Conversation summary

Simply put, VOE hasn’t gathered the very same attention as its big cap and development peers. This signifies the present threat belief that’s accompanies the marketplace’s modification in character because November 1st. Seriously, the case for VOE to intensify investor wealth is moistened by the list below aspects:

- Low weighting to momentum and development aspects,

- Constituent sectors lagging in earnings/sales development + forecasts,

- Beginning multiples not at a broad discount rate to other problems,

- Soft technicals.

Together, these aspects suggest a neutral outlook on VOE, and my judgement shares this view. Net-net, rate hold.