Lemon_tm

By James Knightley, Chief International Financial Expert

After motivating inflation information in early summertime, development stalled in August and September amidst robust customer activity. However with tighter monetary and credit conditions set to weigh even more on business prices power, supplemented by slowing leas and falling gas and utilized vehicle rates, we anticipate to see inflation relocation close to 2% in 2Q

Development being made, however the Fed desires a lot more

At the current FOMC interview, Federal Reserve Chair Jerome Powell stated that the economy has actually “had the ability to accomplish quite considerable development on inflation without seeing the sort of boost in joblessness that has actually been really common of rate treking cycles like this one”. However, there was the recognition that “the procedure of getting inflation sustainably down to 2% has a long method to go”.

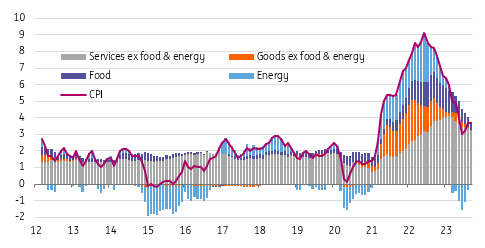

Heading United States customer cost inflation has actually certainly fallen greatly from a peak of 9.1% year-on-year in June 2022, striking a low of 3% in June 2023. Nevertheless, this stalled in August and September with the yearly rate rebounding to 3.7% as greater energy expenses and durability in a few of the core (ex-food and energy) elements reappeared amidst a strong summertime for customer costs. The yearly rate of core inflation has actually continued to soften from a peak of 6.6% in September 2022 to 4.1% presently, however it is still performing at more than double the 2% target.

In an environment where the economy has actually simply published 4.9% annualised GDP development in the 3rd quarter and joblessness is just 3.9%, there are numerous hawks on the FOMC who continue to make the case for extra rates of interest increases, arguing that they can not take possibilities and permit any chance for inflation pressures to reignite.

Contributions to United States yearly customer cost inflation (YoY%)

Macrobond, ING

However the Fed’s work is most likely done

The Fed is still formally anticipating one more 25bp rates of interest increase this year, however we question it will follow through. The Fed last treked rates in July and ever since monetary and credit conditions have actually tightened up, with domestic home mortgages and auto loan now having 8%+ rates of interest while charge card loaning expenses are at all-time highs and business financing rates are moving greater.

It isn’t simply the increase in loaning expenses that will serve as a brake on financial activity and constrain inflation pressures. The Federal Reserve’s Senior Loan Officer Viewpoint study reveals that banks are progressively unwilling to provide. This mix of greatly greater loaning expenses and lowered credit accessibility tends to be hazardous for development. The Fed itself has actually reported considerable weak point in loan need while industrial bank financing information reveals a clear peaking in the quantity of loaning performed by homes and companies. With genuine family non reusable earnings succumbing to the previous 4 months amidst proof of increasing varieties of homes having actually tired pandemic-era cost savings, we anticipate to see GDP agreement in a minimum of 2 quarters in 2024. In this environment, we see the downturn in inflation restoring momentum in early 2024.

Business prices power is subsiding

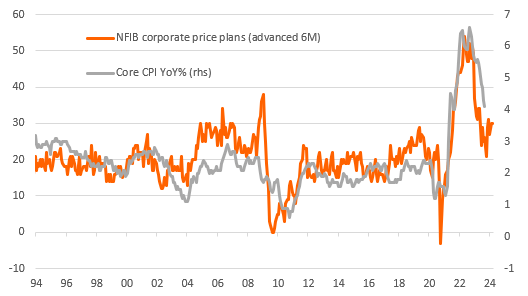

With service mindsets ending up being more careful on the financial outlook we are seeing a decrease in cost objective studies. The chart listed below programs the relationship in between the National Federation of Independent Companies (NFIB) study on the percentage of members anticipating to raise rates in coming months and the yearly rate of core inflation. It recommends that conditions are normalising, with core inflation set to go back to historic patterns.

NFIB cost intents studies recommend business prices power is normalising

Macrobond, ING

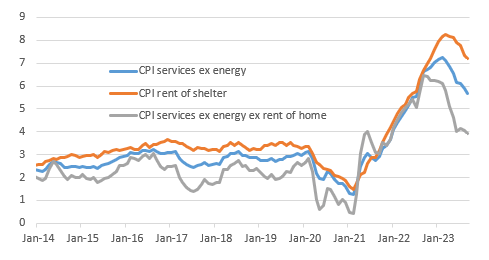

While issues about the outlook for need are an essential aspect restricting the desire for business to raise rates even more, a more benign expense background has actually likewise assisted the scenario. The yearly rate of manufacturer cost inflation has actually slowed from 11.7% to 2.2%, having actually dropped to simply 0.3% year-on-year in June while import rates are falling outright in year-on-year terms. There are likewise indications of labour market slack emerging, with joblessness beginning to tick greater and typical per hour profits development slowing to 4.1% from almost 6% simply 18 months earlier. Maybe more notably, non-farm efficiency rose in the 3rd quarter with system labour expenses falling at a 0.8% annualised rate. With expense pressures relatively easing off from all angles, this ought to argue for core services ex-housing, a part that the Fed has actually been keeping a cautious eye on, to soften rather significantly over the coming months.

Fed’s “supercore” inflation ought to slow more quickly

Macrobond, ING

Energy and car cost is up to depress inflation

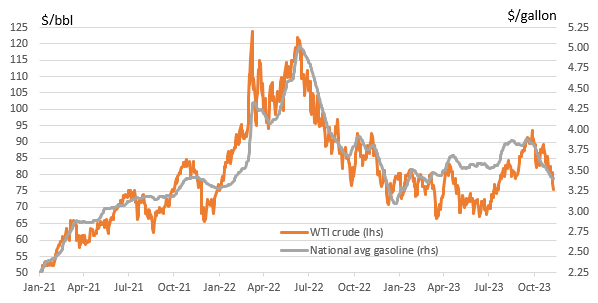

Another location of current motivation is energy rates. The worry had actually been that the dispute in the Middle East would have repercussions for energy markets however, up until now, we have actually seen energy rates soften. Gas rates in the United States have actually fallen 50 cents/gallon in between mid-September and early November, leaving it at its most affordable level considering that early March. Gas has a 3.6% weighting in the CPI basket. Our product strategists stay cautious, caution of the threat that an escalation in the dispute might result in oil and gas supply disturbances from some crucial manufacturers in the area, most especially Iran. In the meantime, however, energy rates will depress inflation rates and might imply a minimum of a couple of month-on-month straight-out decreases in heading rates with lower energy rates restricting any upside capacity from airline company fares (0.5% weight in the CPI basket).

On top of this, we anticipate to see brand-new and pre-owned car rates (integrated 6.9% weighting in the CPI basket) being susceptible to more cost falls in an environment where auto loan loaning expenses are skyrocketing. New car rates have actually increased more than 20% considering that 2020 amidst supply issues and strong need while utilized car rates increased more than 50%, according to both the CPI procedure and Manheim vehicle auction rates. Rates for utilized cars and trucks have actually fallen this year however still stand 35% above those of 2020. Experian information recommends the typical brand-new auto loan payment is now around $730 each month while for pre-owned cars and trucks it is now $530 each month.

With vehicle insurance coverage expenses having actually increased quickly too (up 18.9% YoY with a 2.7% weighting in the CPI basket), the expense of purchasing and owning a car is progressively excessive for numerous homes and we believe we will see rewards progressively topping the benefit for car rates. It is likewise crucial to bear in mind that the rise in insurance coverage expenses is a lagged reaction to the greater expense of cars – and for that reason guaranteed worth – which too ought to slow quickly (however not fall) over the coming months.

Gas rates and oil rates amaze to the disadvantage

Macrobond, ING

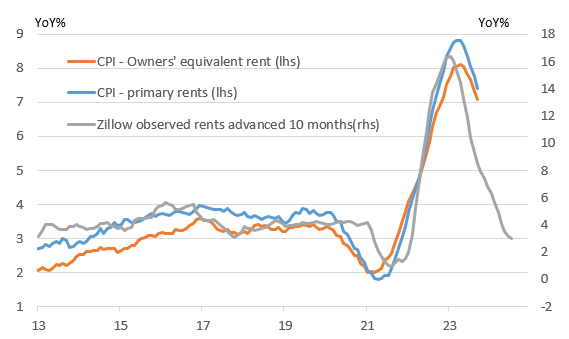

Lease downturn will be the huge disinflationary force in early 2024

The huge disinflationary impact ought to originate from real estate over the next number of quarters. The chart listed below programs the relationship in between Zillow leas and the CPI real estate elements. This is very important since owners’ comparable lease is the single greatest private part of the basket of items and services utilized to build the CPI index, representing 25.6% of the heading index and 32.2% of the core index. On the other hand, main leas represent 7.6% of the heading index and 9.6% of the core. If the relationship holds and the CPI real estate elements sluggish to 3% YoY inflation, the one-third weighting that real estate has in the heading rate and 41.8% weighting in the core will deduct around 1.3 portion points off heading inflation and 1.7 ppt off core yearly inflation rates.

Leas indicate significant real estate expense disinflation

Macrobond, ING

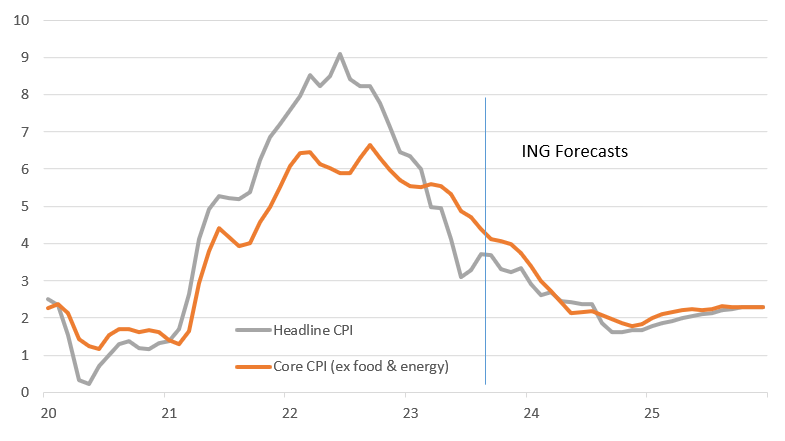

On track for 2% inflation next summertime

There are some elements on which there is less certainty, such as healthcare, however we are progressively positive that inflationary pressures will continue to decrease and this indicates that the Federal Reserve will not require to raise rates of interest any even more. Next week’s October CPI report might disappoint substantial development with heading CPI anticipated to be flat on the month and core rates increasing 0.3% month-on-month, however we anticipate heading inflation to slow to 3.3% in the December report with the yearly rate of core inflation boiling down to 3.7%.

Sharper decreases are most likely in the very first half of 2024. Chair Jerome Powell in a speech to the Economic Club of New york city acknowledged that “offered the fast lane of the tightening up, there might still be significant tightening up in the pipeline”. This will just magnify the disinflationary pressures that are integrating in an economy that is revealing indications of cooling. We anticipate heading inflation to be in a 2-2.5% variety from April onwards with core CPI screening 2% in the 2nd quarter.

With development issues most likely to increase over the very same duration, this ought to offer the Fed the versatility to react with rates of interest cuts. We would not always explain it as stimulus, however rather to move financial policy to a more neutral footing, with the Fed funds rate anticipated to end 2024 at 4% versus the agreement projection and market prices of 4.5%.

ING CPI projections (YoY%)

Macrobond, ING

Disclaimer: This publication has actually been prepared by ING entirely for details functions regardless of a specific user’s ways, monetary scenario, or financial investment goals. The details does not make up a financial investment suggestion, and nor is it financial investment, legal, or tax suggestions, or a deal or solicitation to buy or offer any monetary instrument. Find Out More

Editor’s Note: The summary bullets for this post were selected by Looking for Alpha editors.