Fokusiert

Intro

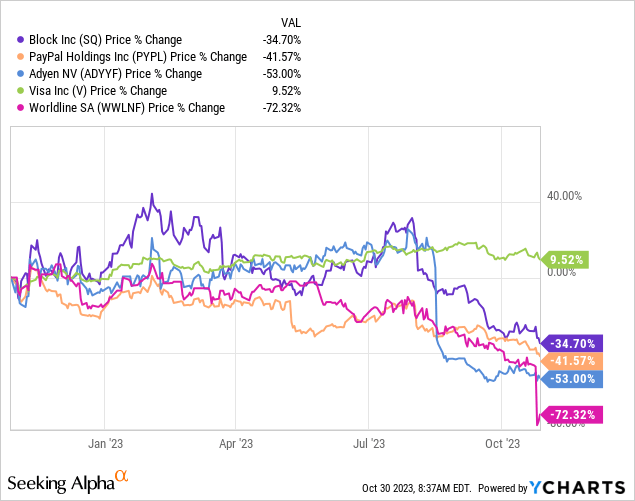

Block, Inc. ( NYSE: SQ) is reporting its Q3 incomes on November 2, post-market. Considered that the business’s stock rate has actually been pushed down to current lows of around $39, I think the approaching quarter will be accompanied by a significant rate relocation. If Block provides a strong report the stock rate has the possible to break the current rate decrease, nevertheless, a similarly weak report might bring the share rate to brand-new lowest levels. Thus, before the report, it is essential to comprehend the elements that will be critical to take a look at in Q3.

From studying Block Inc. in basic for a number of years and in more information over the previous couple of quarters, I have actually discovered the list below elements to play the biggest significance with regard to the business’s post-earnings rate motions:

- Gross Revenue Development.

- Changed Guideline of 40.

- Non-Financial Metrics Relating To Organization Development.

- Secret Item Milestones.

I will go through each of these consider information within this short article, clearly detailing previous efficiency and what to anticipate in Q3. Considered that Block satisfies efficiency expectations within each of these locations, I think that outcomes will be accompanied by a favorable post-market rate motion – nevertheless, provided the fragility of the marketplace, a miss out on in simply among these elements can have a high unfavorable result.

Getting A Feel For The Marketplace

Among the high-ends of Block’s reasonably late reporting date is that a number of noteworthy payment companies have actually currently reported their quarterly outcomes. It works to begin with earlier reports to get a feel for whether there are tailwinds or not within the payments market. I will lay out some noteworthy outcomes listed below that will assist us construct an understanding of how Q3 will play out for Block.

Fiserv, Inc. ( FI)

Fiserv runs a merchant company with a point-of-sale (” POS”) item called Clover. In their Q3 report on October 24, Fiserv reported that Clover attained the following

- Earnings development of 26% YoY.

- Gross payment volume (GPV) development of 15% YoY.

- Deal development 9%.

- Changed running margin 35.9%.

The strength of the business’s incomes and the rhetoric utilized by the CEO, paraphrased by Looking For Alpha – “Although inflation is impacting small companies, they’re still seeing development as customers are still utilizing them”, led to a favorable post-earnings rate motion for Fiserv.

Worldline SA ( OTCPK: WWLNF)

Worldline likewise attained strong efficiency within their merchant company throughout the very first half of this year:

- 13.5% natural earnings development.

- Strong in-store and online payment volume development.

- Onboarded 40,000 brand-new merchants.

( Worldline H1 Report; Looking For Alpha Revenues Records).

Regardless of the favorable news for the very first half of the year, Worldline provided assistance that showed the high likelihood of a weakening European payments market. This unpredictable assistance sustained a sell-off of over 50% on October 25.

Visa Inc. ( V)

Visa’s incomes offer a broad introduction of customer costs internationally. On top of this, the Money App debit card is provided by Visa that makes the business’s incomes report particularly pertinent. The essential outcomes were:

- 9% payment volume development.

- 10% development in processed deals.

- Comparable development in credit vs. debit card purchases.

- Lower card-present development compared to card-not-present development.

Although Visa has actually experienced some pullback in its share rate because incomes, the report reveals that payment volumes are growing in basic. Moreover, we can see that card-present development has actually been significantly weaker than card-not-present development.

Ramifications for Block

Provided all of the outcomes, we can see that the merchant company has actually carried out well in basic both in the U.S. and internationally (as exhibited by Fiserv) and in Europe (as exhibited by Worldline). Nevertheless, the U.S. appears to be experiencing more powerful costs compared to Europe and will likely have a more favorable outlook compared to the latter. This is a great indication for Block, which sourced 96% of its earnings, consisting of Bitcoin, from the U.S. in 2022 ( 2022 10-K). Another point of strength is the truth that basic costs is still growing. This is a tailwind for both Square and Money App.

While the basic image is favorable there are 2 dangers for Block based upon the realities provided above. Initially, the Square company might be negatively impacted by deteriorating costs in Europe, which might result in lower assistance. Second, the Money App company might be negatively impacted by lower development in card-present deals. One big source of Money App’s earnings is from deal charges acquired from debit card deals. A downturn here might have a big unfavorable result on the group as a whole.

1. Gross Revenue Development

The very first line product that I concentrate on throughout Block’s incomes is gross revenue development. Block management thinks about their company through a gross revenue viewpoint instead of earnings because it has an expense focus and is more representative of business due to irregular (gross) accounting for bitcoin earnings.

Previous Efficiency

In Q2 gross revenue development totaled up to 27% which was a small downturn compared to the 32% gross revenue development in Q1. Moreover, gross revenue development has actually remained in a down pattern because Q4 of 2022 – mainly due to the flourishing economy at the time, coming off of low COVID contrasts. The slowing development has actually weighed down the belief for Block. The reason that Block’s share rate reduced post-earnings throughout Q2 was mainly due to the lower-than-expected assistance in Q3 of 21% gross revenue development ( Investor Letter Q2).

The Author

Upgraded Assistance

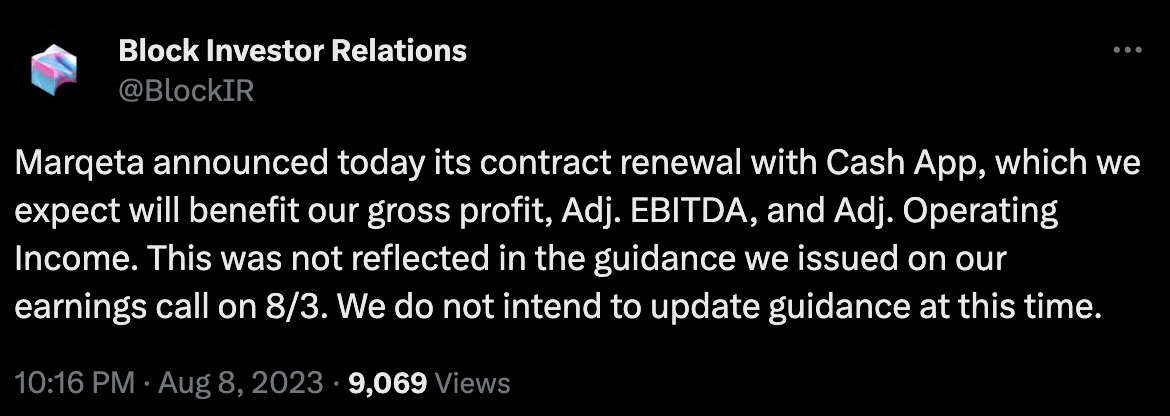

In Q3, we must anticipate a greater gross margin development than the assisted 21%. The factor for this is the upgraded terms in the Marqeta ( MQ) offer. Marqeta supplies card issuance and deal services for the Money App debit card. In August the 2 business upgraded the agreement regards to their collaboration and restored the agreement till the middle of 2027. The upgraded terms imply that Marqeta will have a lower take rate on Money App volume:

” Expecting Q3 and Q4 of 2023, we anticipate the gross revenue take rate we make on Money App volume to be roughly 40% lower as an outcome of the renewal.”

The 40% decrease in rate that Money App has actually worked out will improve margins for many years to come and will absolutely be shown in the Q3 incomes report. Block has actually even provided the following upgrade on X:

Block Inc X Account

Takeaway

Block Financier Relations chose not to upgrade its assistance despite the fact that they anticipate the offer terms to increase development revenue, Adj. “EBITDA”, and Adj. Operating Earnings. The business does not offer any indicator of just how much of an enhancement they will experience in these elements, that makes it challenging to anticipate. Nevertheless, the bottom line is that we must anticipate both a greater gross revenue development in Q3 than 21% and a greater assistance for gross revenue moving forward.

Changed Guideline of 40

Previous Efficiency

Block started suggesting previously this year that it anticipates to determine its community company systems versus the amount of its gross revenue development and changed operating earnings margin.

Throughout Q2 Block attained a gross margin development plus changed operating earnings of 28%, as specified in their investor letter. Although this lacks the business’s 40% objective, it needs to be kept in mind that this objective is a long-lasting effort. In my previous short article on Block’s Q1 incomes, “ Block: What To Search for And What To Overlook In Q1“, I kept in mind that it was prematurely to evaluate the business based upon the Adjusted Guideline of 40 in Q1 and Q2. Nevertheless, for the approaching quarters and years, I think this metric will end up being significantly essential thinking about the possible more downturn in gross revenue development.

Assistance

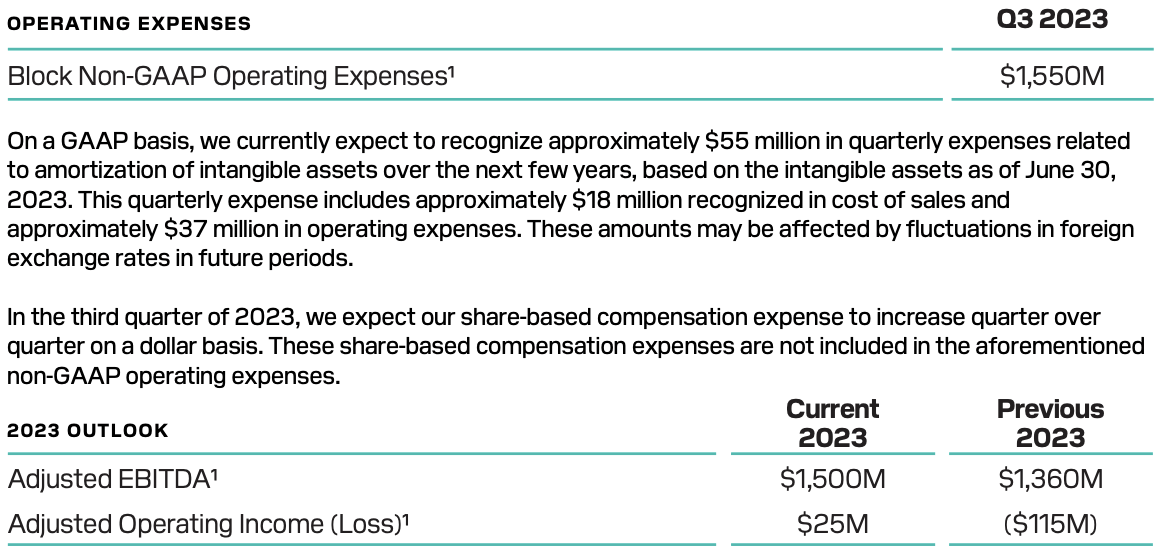

Block Inc

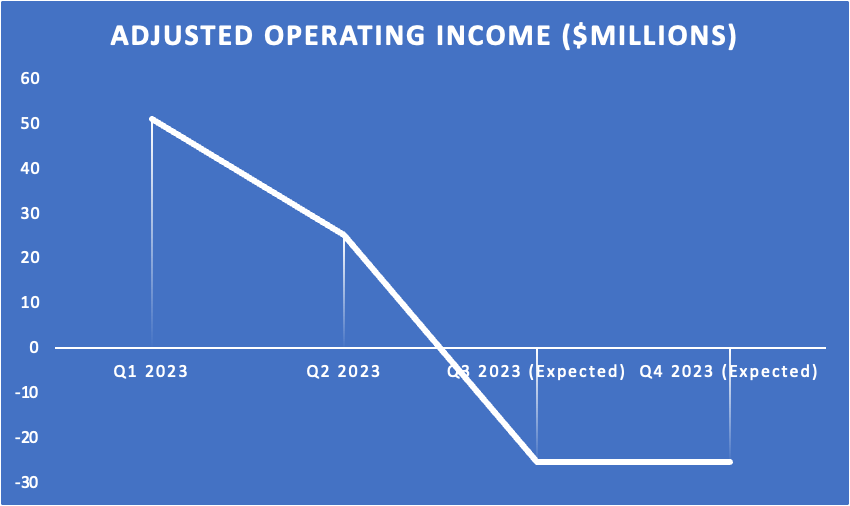

Leaving out the upgraded assistance from the Marqeta offer, Block formerly assisted for an adjusted operating earnings for 2023 to be $25 million. This represents a margin much lower than 1%, which suggests that it will not contribute meaningfully to the Guideline of 40. Moreover, because the adjusted operating earnings has actually been $72 million this year up until now, the assistance indicates that changed operating earnings will be approximately -$ 25.5 in the 2 upcoming quarters.

The Author

Takeaway

Block has actually upgraded its assistance in a favorable instructions with regard to success in Q1 and Q2, which indicates that it will offer an upgraded outlook for 2023 in Q3 also. In the previous quarter, Block forecasted that their changed operating earnings would end up being $140 million much better for the complete year compared to the assistance in Q1. This shows the truth that the business is reducing expenses, consisting of employing downturns and buying more tested marketing channels. Considered that gross revenue development will likely remain in the variety of 21-23%, it is most likely that Block will miss its Guideline of 40 target by a long shot. Although the Guideline of 40 is essential, it is essential to keep in mind that this is a long-lasting objective that needs to not be overstated in the short-term.

Additionally, in Q3 we can anticipate an additional boost in the success assistance, which would add to a favorable belief for the stock rate. Nevertheless, there is a big danger success is weighed down by a puffed up headcount. Although Block COO, Amrita, specified throughout the Q2 incomes call that they anticipate a head count boost of less than 10% in 2023, Block has yet to perform any mass layoffs comparable to what other huge tech peers such as Shopify ( STORE) and Alphabet ( GOOG) ( GOOGL) have actually done. This might even more suppress success efforts in addition to favorable stock exchange belief.

3. Non-Financial Metrics Relating To Organization Development

There are 3 essential non-financial metrics to take a look at in the approaching quarter:

- Money App inflows structure.

- Square gross payment volume (GPV).

- Square upmarket development.

1. Money App inflows structure

Money App has 3 motorists of success which are regular monthly active users, inflows per active user, and the money making rate. In June regular monthly active users totaled up to 54 million, representing a 15% YoY development. In Q3, we must be trying to find this number to continue increasing. In basic brand-new regular monthly activities might not grow considerably QoQ due to the business’s reduced marketing invest, nevertheless, considered that Money App has as much traction as Block states it does then there must be no factor for stagnancy here.

Inflows per active is a step of just how much cash each active brings into Money App on a month-to-month basis usually. In Q2 the typical inflow was $1,134, representing an 8% YoY boost and a flat QoQ modification. Money App has actually just recently broadened its discount rate offerings to a broad variety of merchants throughout the quarter which might assist draw more cash into the community. For that reason, I anticipate inflows to somewhat increase QoQ. One aspect that may work versus this nevertheless is the truth that Money App does not provide any interest-bearing cost savings accounts. In this high rate of interest environment consumers wish to make interest on cash being in their account, which is something that conventional banks in addition to the neobank SoFi Technologies ( SOFI) deal.

Lastly, the money making rate on Money App is most likely to remain flat. Amrita specified the following in Q2.

” Money making rate, which omits gross revenue contributions from our BNPL platform was 1.44%. Money making was up 16 basis points year-over-year, driven mainly by rates modifications over the previous year, and up 3 basis points quarter-over-quarter, driven mainly by the timing of strong very first quarter inflows throughout the tax season.”

( Looking For Alpha Records)

Additionally, it was kept in mind that the business just recently made rate boosts which suggests that the money making rate is most likely to remain around 1.44%.

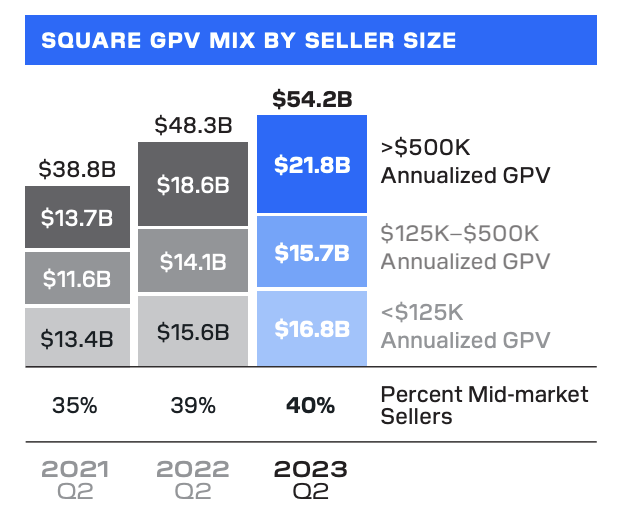

2. Square GPV

GPV is a step of the payment volumes that stream through Square. Last quarter Square had a GPV of $54.2 billion, representing a 12% YoY development. For Q3 and Q4, Amrita provided specific assistance:

” Square GPV is anticipated to be up 12% year-over-year, constant with the 2nd quarter as we have actually seen stability in GPV development over the previous 3 months from Might through July. For the 4th quarter, we anticipate gross revenue and GPV development to enhance somewhat compared to the 3rd quarter as Square take advantage of more beneficial contrasts.”

Thus, we must anticipate GPV to grow by 12% and a development rate under this might be a sign of an additional weakening macro environment. This kind of development is most likely achievable provided Fiserv’s GPV development of 15% YoY.

3. Square Upmarket Development

Lastly, Square has actually made terrific efforts to grow from serving little sellers to serving medium and large-size sellers. In Q2, 40% of the business’s GPV originated from mid-market sellers, representing a considerable enhancement from Q2 in 2021.

Block Inc

The development to larger sellers indicates that Square will be put in more long lasting chains that have more complicated software application requirements. This develops GPV development for Square in addition to margin enhancements as the business can offer more software application services to these kinds of sellers. In Q1 of 2023, this rate was at 38% for this reason the current enhancement is most likely credited to the business’s brand-new go-to-market technique. Square is now concentrated on selling in particular upmarket verticals such as big arenas, big dining establishment chains, and so on. They have actually done this by focusing on the sales force and likewise upgrading the site view to deal with the brand-new technique. For these factors, I anticipate to see a small uptick from 40% next quarter.

4. Secret Item Turning Points

There is one essential item turning point that Block lovers like myself have actually been waiting on: the combination of Square and Money App. Jack Dorsey has actually stated, at JPMorgan’s 51st Yearly Conference:

” And within the app, we have this brand-new location, which is incredibly cumbersome today called Discover that individuals today are simply utilizing to discover individuals they formerly paid or individuals that they wish to pay in their address book, however ultimately will be the merchants around them, primarily Square merchants around them.”

The business is dealing with strengthening the 2 communities by having regional offerings on the app, where Square merchants can be found and Money App customers can discover good deals. This design has the possible to be actually strong which is most likely why the business is taking its time to get this right.

Current task posts recommend that this effort is a high concern within the business. A current task description started with the following:

” We’re trying to find an Item Supervisor to lead a brand-new, 0 to 1 effort of bringing an international customer benefits program to market for Square. Reporting to the Item Lead for Consumer Experience, you will increase discovery for our Sellers, assist them bring in brand-new consumers, and improve sales. Our vision is to link Block’s Seller and Purchaser networks to construct an industry-leading money back rewards program for regional services, making every Square purchase fulfilling.”

Developing this kind of reward that “make[s] every Square purchase fulfilling” will develop an unbelievable support result on the business’s existing operating design.

Takeaway

This combining of communities has actually remained in procedure since Block obtained Afterpay in August of 2021. Thus, it is most likely that the roll-out of this combination will occur quickly. Nevertheless, there has actually been no clear indicator of when this might occur which has actually moistened financier beliefs of it taking place at all. Although it is extremely unpredictable when this will happen I think that when it does occur it will drive strong momentum for business in addition to the stock rate.

Summary: Drivers and Threats

In all, this is what to anticipate entering into Q3:

- Gross revenue development > > 21% (formerly assisted).

- Greater gross revenue assistance for Q4.

- Changed running earnings > > $25 million for 2023 (formerly assisted).

- Development in Money App regular monthly actives and inflows per active, with a stable money making rate of 1.44%.

- Square GPV development of 12% YoY.

- Square mid-market penetration of somewhat higher than 40%.

- Update on the Money App and Square Combination.

Considered That all of these elements are upfilled I think that we might see a favorable post-earnings rate action. Based upon earlier incomes outcomes of Fiserv and Visa, there appear to still be tailwinds in general customer costs in the U.S. which might support these drivers above. Nevertheless, Worldline’s unfavorable outlook on the European market where Block is likewise active recommends that headwinds are likewise impending. Because the marketplace is very conscious problem today, it is most likely that if Block misses on any of the essential expectations above the share rate will fall post-earnings. Provided the info I provided above, I hope that you can make a judgment on whether Block is most likely to satisfy these expectations or not.

I think that Block will have the ability to satisfy the expectations it has actually set out for itself, consisting of the upgraded assistance after the Marqeta offer. Nevertheless, as a long-lasting investor, I am not going to worry any quarterly outcomes. In the long term, I rate the business a strong buy due to the considerable pullback the share rate has actually experienced. Moreover, the essential drivers called above, if satisfied, can result in a rate boost in the short-term also.