Starting our protection of the very first revenues season of the year for the tech market, we as constantly begin with Intel. The blue-hued blue-chip is the very first out of eviction to report their outcomes for the very first quarter of 2023, with Intel getting the pieces after a rough end to 2023, and a rather agonizing start to 2023. With income down on an annual basis practically throughout the whole board thanks to a significant, market broad downturn in customer and server sales, Intel’s focus has actually been on securing the hatches to weather this rough duration, while getting ready for an ultimate (if modest) upturn in the market later on this year.

For the very first quarter of 2023, Intel reserved $11.7 B in income, a sheer 36% drop from the year-ago quarter. As held true in Q4, Intel remains in the middle of a significant market downturn, which has actually struck profits tough and operating/net earnings even harder. Intel closed the quarter at a loss on an operating earnings basis, losing $1.5 B, and the business’s general bottom line was an incredible $2.8 B on a GAAP basis.

| Intel Q1 2023 Financial Outcomes (GAAP) | ||||||

| Q1′ 2023 | Q4′ 2022 | Q1′ 2022 | Y/Y | |||

| Profits | $ 11.7 B |

$ 14.0 B |

$ 18.4 B | -36% | ||

| Operating Earnings | -$ 1.5 B |

- $ 1.1 B |

$ 4.3 B | -134% | ||

| Earnings | -$ 2.8 B | -$ 661M |

$ 8.1 B |

-134% | ||

| Gross Margin | 34.2% | 39.2% | 50.4% | -16.2 ppt | ||

| Customer Computing Group |

$ 5.8 B(* ) . |

. | . | . | ||

| . | .(* )$ 4.3 B | $6.0 B(* ) . | .(* ) . | Network and Edge Group | ||

| $ 2.1 B | . | . | Mobileye(* ) . | . | ||

| . | . | . | . | . | ||

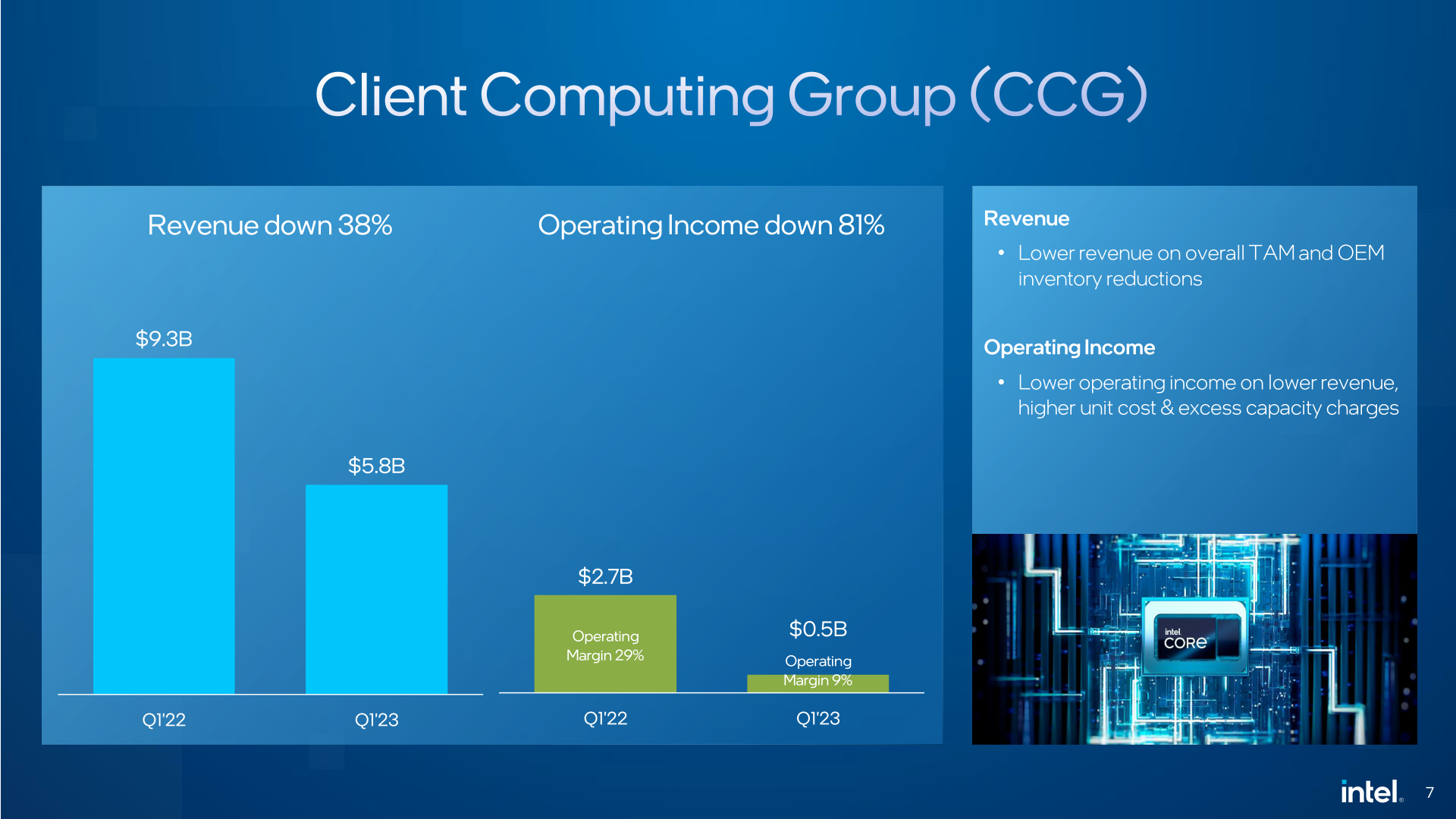

| . | . | . | And yet, in spite of all of this, this quarter went much better than anticipated for Intel. The business had actually alerted financiers early-on that it would be harsh, and while Intel provided on those pledges, it surpassed its income and EPS forecasts from earlier in the quarter. So while the business is far from running out its existing downturn, there are some indications that it might be nearing the bottom. | To that end, Intel reserved $5.8 B in customer income for the quarter, which is down 38% from the year-ago quarter. In spite of all of this, the CCG preserved a favorable operating margin, coming out ahead by $0.5 B, for a 9% margin. Taking a look at Intel’s in-depth report, laptop computer sales dropped more difficult than desktop sales, though both were down substantially. At this moment Intel’s downstream OEM clients are still burning through formerly bought stock, which indicates that Intel is offering far less chips than is normal. Intel stopped offering ASP info a long time back, so it’s uncertain just how much a modification in chip prices is likewise an aspect. | ||

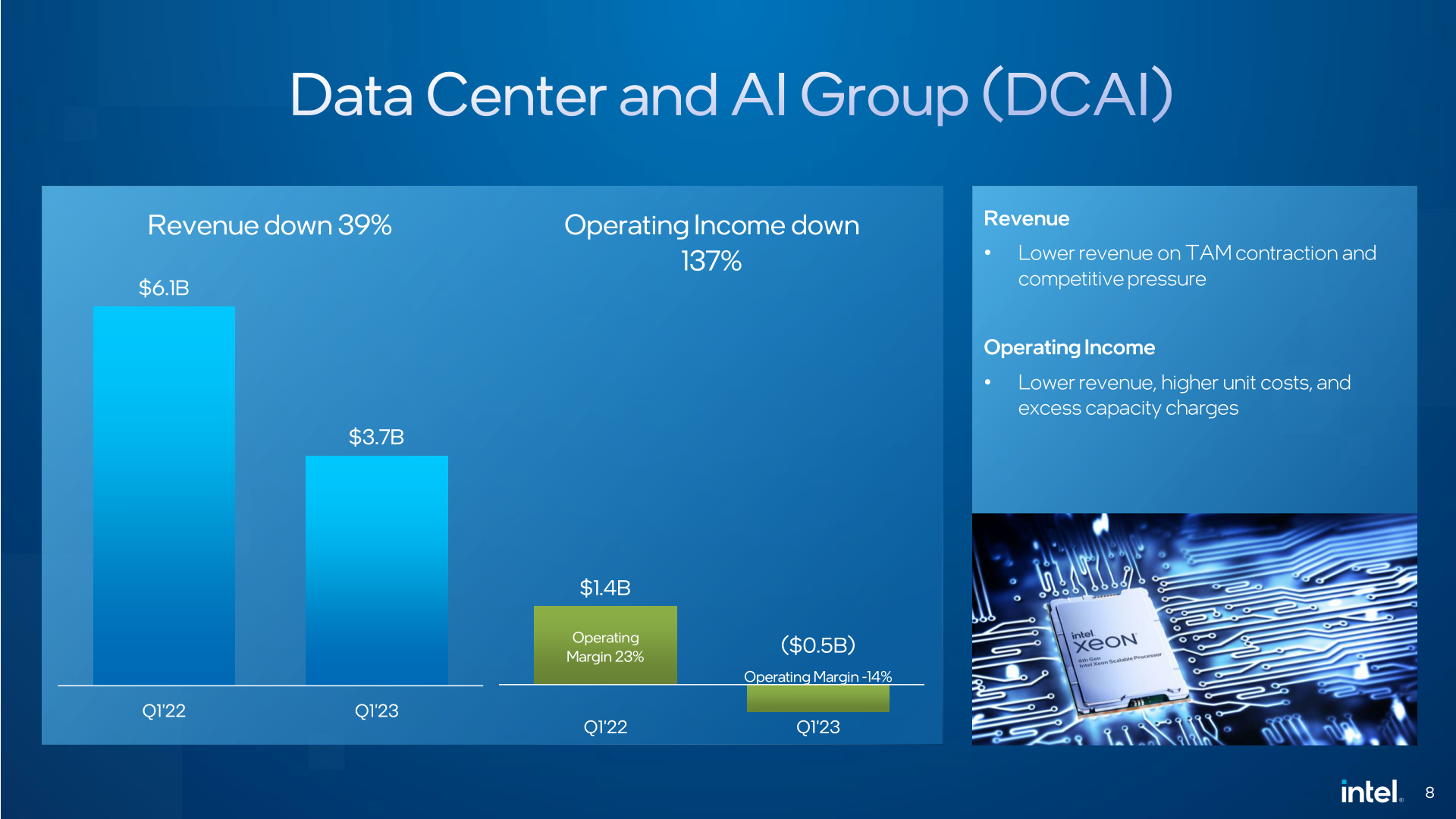

, this appears to be appropriate. In spite of being what’s generally Intel’s greatest margin service system, Intel was not able to eek out even a functional earnings on server parts for the quarter.

Making complex matters rather has actually been yet another organizational modification within Intel. The Accelerated Computing and Graphics Group (AXG), which was formerly a top-line service system, was broken up and subsumed late in December by the CCG and DCAI service systems, with each taking their particular half of business. The contemporary version of AXG is now exclusively concentrated on datacenter parts, and belongs of DCAI. I bring this up because as a new service system, AXG itself was running an operating loss in 2022. Per Intel’s modified figures to permit like-for-like, year-over-year contrasts with their modified service systems, the combined service system shift knocked almost $300M off of DCAI’s operating earnings for Q1′ 2022. There’s no chance to inform what the effect was for 2023, however it appears not likely that AXG was favorably adding to DCAI’s success.

The last of Intel’s huge groups is the Network and Edge Group (NEX), which covers Intel’s networking, connection, and IoT items, and is where Intel records sales of other silicon such as Xeon SKUs for networking items. NEX has actually taken a comparable hit as Intel’s other top-line groups, with profits falling 30% to $1.5 B. This sufficed of a drop to likewise press NEX into the red, losing $300M for the quarter. According to remarks from Intel CEO Pat Gelsinger, the NEX consumer base is enacting comparable stock corrections as a few of the other chip systems, which will continue for a couple more quarters.

Completing Intel’s portfolio, Mobileye was the one unique intense area in Intel’s revenues report. The vehicle group has actually seen income grow year-over-year by 16%, reaching brand-new records for the quarter. And while running earnings were down by 17%, it’s still running in the black. Intel Foundry Provider (IFS) on the other hand remained in the red, though this isn’t unforeseen as Intel is still in the middle of a multi-year financial investment method to retake fabulous efficiency management. Profits dropped 24% year-over-year, however Intel has actually made it clear that IFS is a long-haul possibility that they will continue to invest greatly in.

Looking forward, while Intel is suggesting that parts of its service sections have actually bottomed out (or almost so), Q1 was not the last bad quarter for Intel. For Q2′ 2023 the business is forecasting profits of $11.5 B to $12.5 B, which would be a 22% YoY drop. Gross margins are anticipated to drop even more also, to a GAAP gross margin of simply 33.2%. As kept in mind previously, the business is forecasting a modest healing in the 2nd half of the year, however they will still need to survive Q2 to arrive.

Following Q1, Intel’s significant general efforts stay the same, both with concerns to item strategies and functional expenditures. As revealed in 2015, the business is carrying out efforts to substantially cut expenditures; and according to Pat Gelsinger, Intel is “well on our method” towards lowering expenses by $3B in 2023, reaching a yearly cost savings of $8B to $10B by the end of 2025.

Otherwise, Intel does not have any significant item launches on its public roadmap for Q2 to substantially alter the status quo. Nevertheless, one intense area in regards to hardware advancement is that Intel’s next-generation Intel 4 production procedure and associated Meteor Lake customer CPU have actually gotten in production, with additional ramping occurring throughout the year. As Intel requires to provide on 5 nodes in 4 years to have a major opportunity at retaking management in the fabulous market, this is an appealing indication that they are certainly on track.