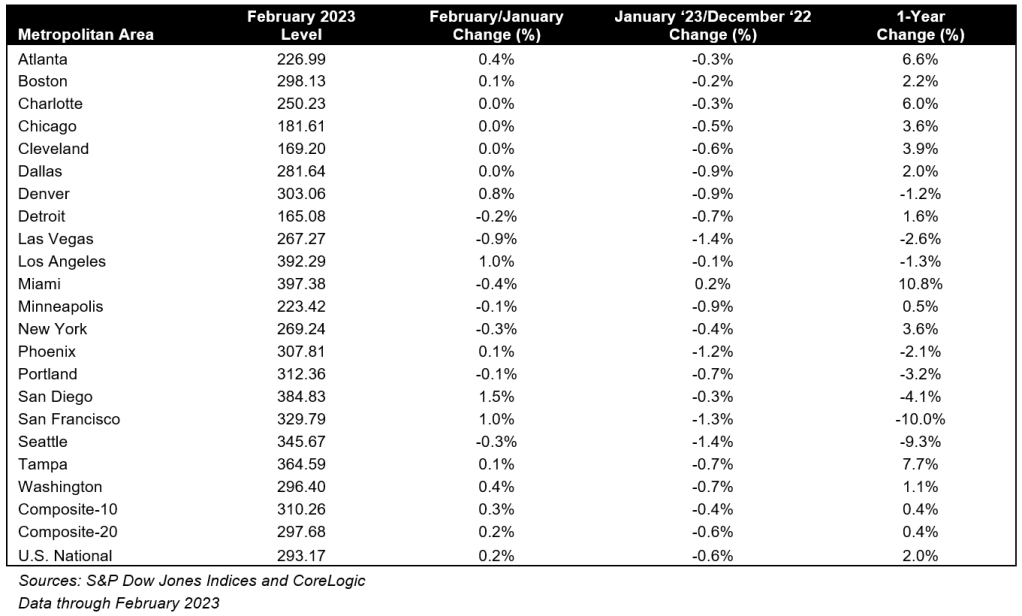

House rate development cooled even more in February, being up to a yearly development rate of 2.0%, according to the S&P CoreLogic Case-Shiller National House Cost Index, launched Tuesday. The yearly development rate in January was 3.7%.

The nationwide index was available in at a reading of 293.17 in February. On a month-over-month basis, the index was up 0.2% prior to seasonal modification.

” House rate patterns moderated in February 2023,” Craig Lazzara, the handling director at S&P DJI, stated in a declaration. “The National Composite, which had actually decreased for 7 successive months, increased a modest 0.2% in February, and now stands 4.9% listed below its June 2022 peak.”

The February information pre-dates the obstacles in the industrial banking market, which began in early March, nevertheless, market forecasters expect that rates of interest will stay raised as the Federal Reserve continued to concentrate on its inflation-reduction targets.

“ Home mortgage funding and the possibility of financial weak point are for that reason most likely to stay a headwind for real estate rates for a minimum of the next numerous months,” Lazzara stated.

Nevertheless, in spite of the current uptick, the continued low stock conditions are anticipated to keep house rates raised nationally.

” Stock has actually stayed low as sellers are locked into their low home mortgage rates, even as lots of house purchasers are turned away from this market due to price restraints amidst unstable home mortgage rates,” Nicole Bachaud, Zillow‘s senior financial expert, stated in a declaration. “No matter slower than normal need, the low stock environment is producing more competitors on less houses, resulting in rates reversing their descent from in 2015’s peak, which will likely continue in the coming months. To stay in the market and remain competitive, lots of purchasers are taking a look at lower priced houses to survive, with houses in the most affordable rate tier seeing the most competitors and rate development early this spring.”

The Case-Shiller house rate indices for February is a three-month average of closing rates in December, January and February. Since a lot of house sales take numerous months from agreement to closing, the information most likely consists of some offers struck in October and November.

House rate development in the 20-city composite index likewise slowed in February, tape-recording a yearly gain of 0.4% to a reading of 297.68. In January, the 20-city index published a yearly boost of 2.6%. Compared to a month prior, the 20-city index published a 0.2% boost prior to seasonal modification.

The S&P CoreLogic Case-Shiller 20-city composite house rate Index is a value-weighted average of the 20 city location indices. The indices have a base worth of 100 in January 2000; simply put, a present index worth of 150 translates to a 50% gratitude rate given that January 2000 for a normal house situated within a specific market.

The 10-city house rate index likewise published a 0.4% annual boost, below 2.5% in January, bringing it to a reading of 310.26. Month over month, the 10-city index increased 0.3% prior to seasonal modification.

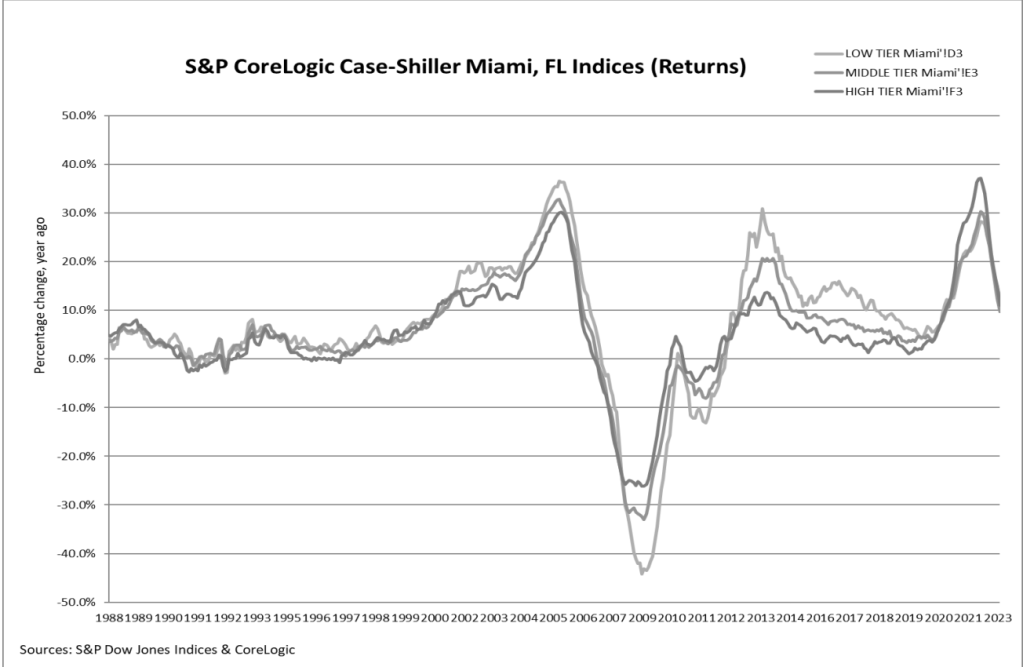

Yet once again, Miami (10.8%), Tampa (7.7%) and Atlanta (6.6%) once again reported the greatest yearly rate gains amongst the 20-cities examined. All 20 cities published lower rates in the year ending February 2023 versus the year ending January 2023, however on a month-over-month basis 12 of the 20 cities published rate gains, compared to simply one in January.

At the other end of the spectrum, San Francisco (-10.0%), Seattle (-9.3%), and Portland (-4.1%), published the biggest yearly reductions amongst the 20 cities. Phoenix, as soon as the star of the Case Shiller index, published a 2.1% yearly rate reduction in February.

” February’s outcomes were most fascinating since of their plain local distinctions. Miami’s 10.8% year-over-year gain made it the best-performing city for the seventh successive month. Tampa (+7.7%) and Atlanta (+6.6%) continued in 2nd and 3rd location, with Charlotte (+6.0%) close behind. Outcomes were various in the Pacific and Mountain time zones,” Lazzara stated. “Last month, 4 West Coast cities (San Francisco, Seattle, San Diego, and Portland) remained in unfavorable year-over-year area. In February they were signed up with by 4 of their western next-door neighbors, as Las Vegas (-2.6%), Phoenix (-2.1%), Los Angeles( -1.3%), and Denver (-1.2%) all tipped into unfavorable area. It’s unsurprising that the Southeast (+7.8%) stays the nation’s greatest area, while the West (-4.2%) continues as the weakest.”