Vladdeep/iStock by means of Getty Images

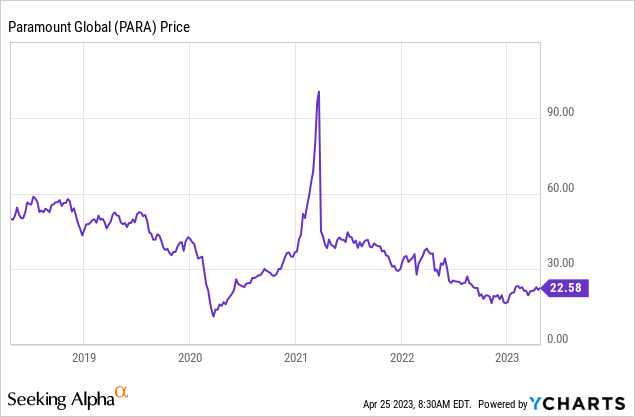

Among my more aggravating financial investments over the previous 4 years has actually been Paramount Global ( NASDAQ: PARA) ( NASDAQ: PARAA). The stock cost has actually made wild swings with cycles in the economy and Wall Street thinking about the minute. It’s traded as low as $10 after the COVID pandemic began to as high as $103 on a meme-led brief capture in early 2021. Yet, for the many part, the quote has actually hovered in the $20s and $30s.

YCharts – Paramount Global, Cost Modification, 5 Years

W hat’s altered because my last bullish post on Paramount in 2015? The response is an overly-confident and substantial brief interest position has actually been developed over the last 9 months. Similar to the 2020 pandemic economic downturn triggered brief sellers to stack into bets on a lower Paramount stock quote, the middle of 2022 to early 2023 has actually experienced a comparable belief from bearish traders. In result, today’s brief position approaching 20% of share float has actually “oversold” the stock cost beyond where it would be trading otherwise.

If and when traders choose to cover their shorts (putting in buy orders), a genuine imbalance in share supply/demand might support a beast upmove back to $30 and even $40, all other variables staying the exact same. Plus, this spike in cost might take place in the face of a bearishness normally for the U.S. stock exchange (which is my present projection), and even throughout growing report of an economic downturn.

Background

Among the leading media business worldwide, owning an important significant U.S. tv network in CBS, the business has actually branched off to streaming media material through Paramount+ and the complimentary to customers advertising-based Pluto Television, which is a cross in between Alphabet/Google‘s ( GOOG) ( GOOGL) YouTube and cable (having an objective of lots of countless channels eventually).

Warren Buffett‘s Berkshire Hathaway ( BRK.A) ( BRK.B) has obtained a product stake due to the fact that of Paramount’s worth attributes, along with a high dividend yield (4.3% presently). And, with veteran managing investor Sumner Redstone passing a couple of years back, the chances of a separation or takeover of the business have actually increased drastically. I have discussed and continue to think Paramount possessions would make a fantastic suitable for Netflix ( NFLX), which might highly gain from a broadening moat of owned material plus a live streaming network for paying customers.

The evaluation story is still engaging, although revenues have actually remained in decrease throughout 2022-23 due to the fact that of a rotten online and tv advertisement market entering into a possible U.S. economic downturn. The business does bring a high level of financial obligation, with increasing interest expenses. So, a double whammy of increasing expenditures for labor, material development and financial obligation service have actually integrated with weaker top-line sales to actually crunch margins. Wall Street is anticipating business setup will just be somewhat lucrative in 2023.

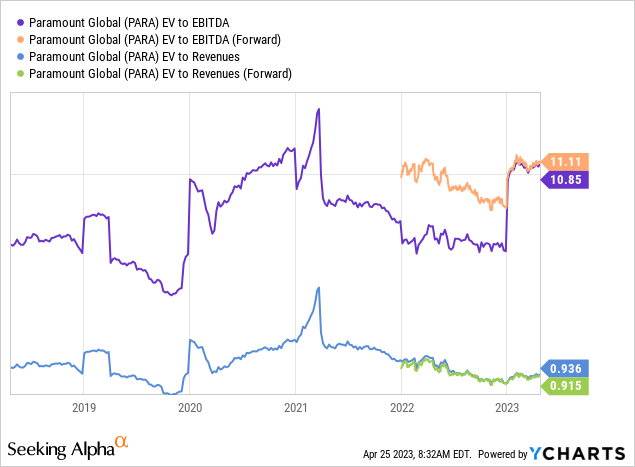

Below are charts of the business worth photo on EBITDA capital (11x) and incomes. You will discover the evaluation on sales is getting exceptionally depressed for a media company, with an EV ratio now well under 1.0 x, even lower than the pandemic panic selloff.

YCharts – Paramount Global, Business Valuations, 5 Years

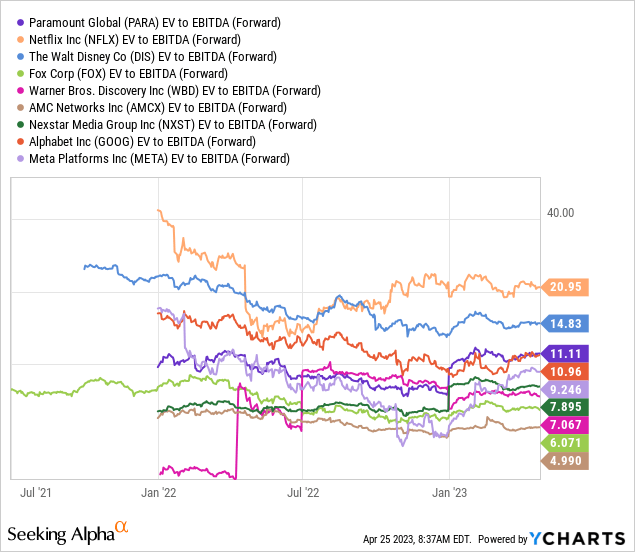

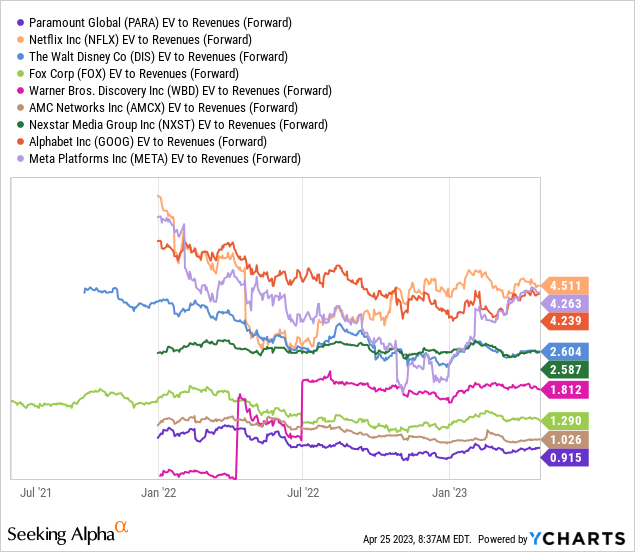

Comparing these all-encompassing numbers with financial obligation and money figured into the evaluation, peer media services as a group are priced at lower multiples of EBITDA, however much greater ratios on sales. My sort list for a competitor/peer group consists of Netflix, Walt Disney ( DIS), Fox ( FOX) ( FOXA), Warner Bros. Discovery ( WBD), AMC Networks ( AMCX), Nexstar ( NXST), Alphabet/Google, and Meta Platforms ( META).

YCharts, Tv and Online Media Leaders, EV to Forward Approximated EBTIDA, Considering That January 2022

YCharts, Tv and Online Media Leaders, EV to Forward Approximated Sales, Considering That January 2022

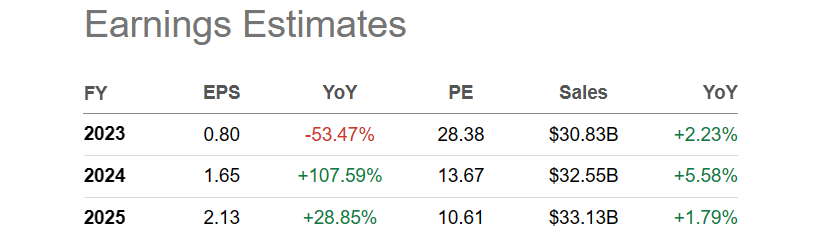

Fortunately is margins and revenues are forecasted to increase significantly after 2023’s near catastrophe. Wall Street expert quotes are requiring a strong upturn in earnings, based upon presumptions of a much better advertisement market and small raises in streaming membership charges per client.

Looking For Alpha Table – Paramount Global, Expert Price Quotes 2023-25, Made on April 24th, 2023

Brief Capture Approaching?

So, if operating company results bottom in 2023, what driver could assist fire up an increase in the share quote? For Paramount in specific, the increasing brief interest position is a really bullish advancement, in my view.

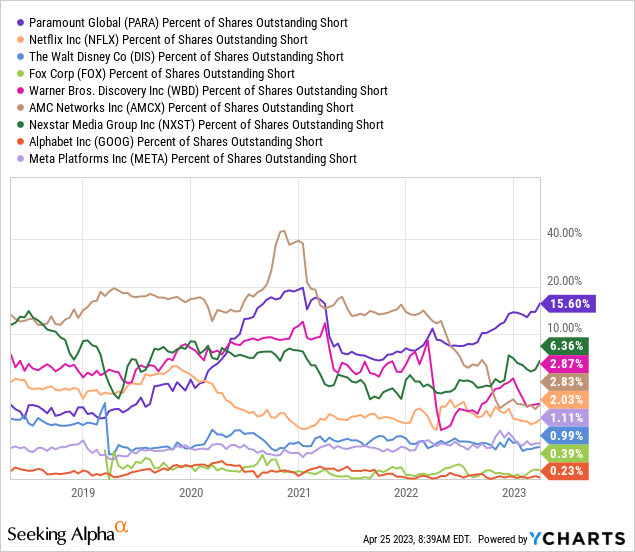

Think it or not, the brief position overall as a portion of exceptional shares released has actually approximately doubled because August to nearly 16%. The raw size of the brief interest is now on a par with late 2020. And, these bearish bets are quickly 5x the rate experienced by other media peers typically.

YCharts, Tv and Online Media Leaders, Short Position vs. Impressive Shares, 5 Years

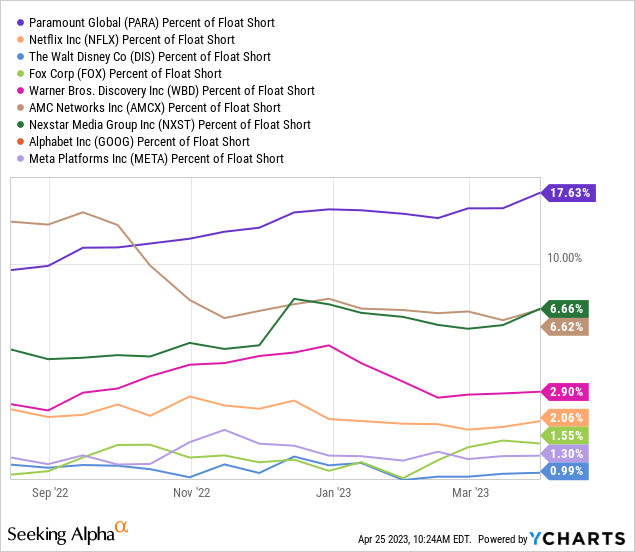

When you deduct the Redstone household ownership stake, the percent of share “float” offered brief is even higher at almost 18% (in the April exchange report). Utilizing this information point, the brief position is a great 3x greater than any other peer.

YCharts, Tv and Online Media Leaders, Short Position vs. Share Float, Considering That August 2022

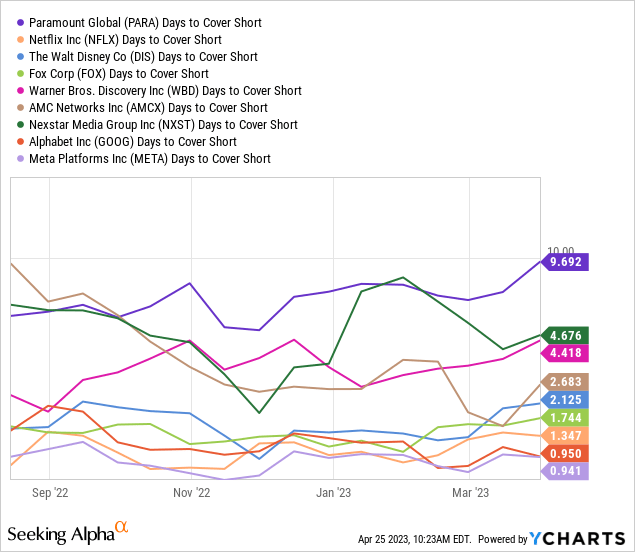

Lastly, the days to cover ratio (which takes a look at typical trading volume vs. the entire brief position) has actually increased to roughly 10x, which has to do with the like the greatest bear readings of late 2020 (not envisioned). This ratio is double any other peer/competitor and nearly 5x the typical average for the group. Naturally, if favorable operating news is our future, sellers will go back and desire greater costs at the exact same time as brief sellers rush to purchase.

YCharts, Tv and Online Media Leaders, Theoretical Days to Cover Short Position, Considering That August 2022

2020-21 Short-Squeeze Moonshot

Why are extended brief positions crucial to think about for cost projections? Essentially, additional selling (with obtained shares) in a lucrative and important hidden company reduces cost to a level far lower than would otherwise hold true. In the end, any factor for shorts to cover operate in the opposite method, where it presses cost greater to discover supply to perform deals. If you have two times as lots of purchasers as sellers one day, for instance, nervous brief purchasers might want to pay a considerably inflated cost to leave their presold and obtained positions. In theory, brief seller losses might be “limitless” if they can not discover shares to cover their position.

The once-in-a-generation GameStop ( GME) brief capture of early 2021 is real-world evidence of what can take place to cost when a beast imbalance of nervous purchasers vs. no share supply exists.

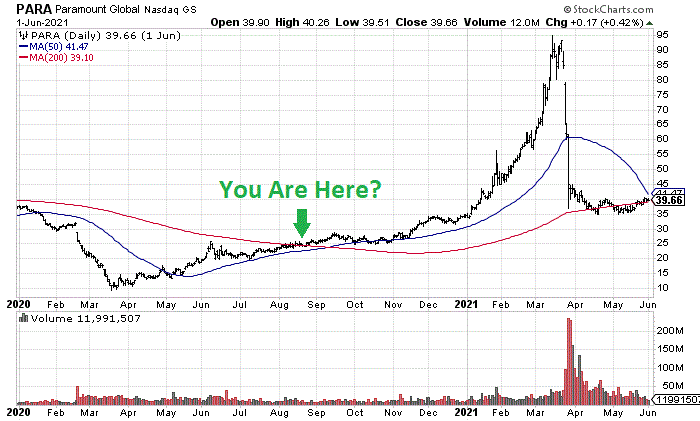

Anyhow, Paramount did experience a rather robust brief capture at the exact same time as GameStop, drawn listed below. On the dividend-adjusted chart of day-to-day trading action in between January 2020 and June 2021, we can examine the entire overstated short-selling cost result in the very first half of the chart, vs. the brief covering rally into March 2021. Unusually big swings in cost are what brief sellers achieve in the end.

StockCharts.com – Paramount Global, Daily Cost & & Volume Modifications, Author Recommendation, Jan 2020 to June 2021

In my mind, we might be getting in the exact same point on the chart today as August 2020, marked with the green arrow. Paramount is attempting to get above its 200-day moving average in April 2023, with the net brief position reaching a comparable extreme as 2020.

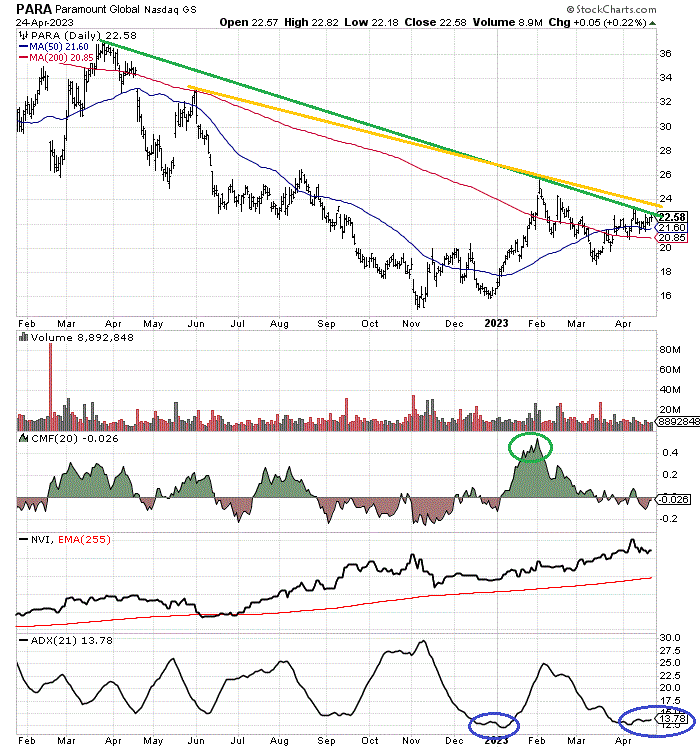

On the existing chart, you can see Paramount is likewise trading simply listed below a number of trendlines (green and gold) that can be drawn linking the high sell cost over the last 13 months.

Taking a look at some bullish momentum indications, the 20-day Chaikin Cash Circulation reading reached its greatest level throughout January in years (circled around in green). The Unfavorable Volume Index is highlighting a healthy purchasing pattern on weak point. And, the 21-day Typical Directional Index is recommending a low-volatility balance in between purchasers and sellers, comparable to the late 2022 bottom in cost around $16 (circled around in blue).

StockCharts.com – Paramount Global, 15 Months of Daily Cost & & Volume Modifications, Author Recommendation Points

Buy Strategy

For traders, the very best method to play an establishing brief capture might be to wait on a rate break above $23.50 to $24 per share. That method if an economic downturn pulls cost lower very first (which is totally possible), you will not be stuck to a short-term loss waiting on much better days to appear. The most convenient strategy would be to position a stop-buy order in this variety, holding your brokerage money earning interest till a clearer cost turnaround ends up being truth.

I do own a little position presently and am weighing when and how to increase my position size. Missing my bearish market view today, I would likely be including shares today. So, it might depend upon your take on total market dangers. For sure, if Paramount can break above $24, the thumbs-up to include shares will be harder for me to overlook.

What could fail? Essentially, the extension of increasing rates of interest and/or a deep economic downturn in America would act to hold the value/price of Paramount under $25 to as low as $15 the remainder of the year (last November’s low cost). For worth financiers and bottom fishers, costs under $20 might show a fantastic entry zone for long-lasting thinkers. That’s why it’s challenging to offer in the low-$ 20s. You might actually kick yourself if a quote above $40 is can be found in 2024.

The benefit bullish argument is a brief capture, property sales to decrease financial obligation, and even a merger arrangement with a larger entity like Netflix, Amazon ( AMZN), Google, or Apple ( AAPL) sends out the Paramount quote drastically greater. With a variety of prospective drivers and a low property evaluation for this leading media company, I would rather hold shares and concentrate on purchasing a bigger position.

Thanks for reading. Please consider this post an initial step in your due diligence procedure. Consulting with a signed up and experienced financial investment consultant is suggested prior to making any trade.