AM-C

Last November, I released “ Credit Suisse: Bank Failure Is Not Off The Table,” which comprehensive my bearish outlook for Credit Suisse ( CS) and my view that the bank might stop working in 2023. Naturally, that post fulfilled some debate, as, at the time, the possibility of such a big bank stopping working appeared too severe. Today, the stock is approximately 75% lower as the bank falls apart, with UBS ( UBS) purchasing the rest of its company at an exceptionally high discount rate

If I were to make a style for 2023, it would be to “anticipate the unanticipated.” Thinking about the tremendous degree of off-balance sheet losses in lots of United States and European banks, financiers would be a good idea to brace for a continual boost in volatility and unpredictability. As detailed in “ KRE: The Banking Crisis Has Actually Slowed, However It Can not Be Stopped” relating to the local bank ETF ( KRE), lots of United States banks have a net possession worth near absolutely no today if we represent the ~$ 2.2 T in latent losses on securities positions. As banks deal with deposit outflows (due to low cost savings rates, increasing living expenses compared to incomes, and a falling cash supply from QT), they’re required to offer these properties at considerable losses. The United States Fed’s motivation of the “Discount rate Window” and the ECB’s comparable relocations have actually briefly assisted the liquidity lack; nevertheless, the crucial concern of excess overall public and personal financial obligation, integrated with increased interest expenses on that financial obligation, can not be fixed so rapidly.

The reality that inflation is constantly high in both the United States and Europe makes it hard for federal governments to offer the essential stimulus, as doing so might threaten the currently damaging position of Western currencies (compared to BRICS). Appropriately, the Fed, ECB, and their particular federal governments are strolling on a delicate tightrope in between supporting a (predominately) “zombified” monetary system (which has actually depended on federal government assistance because 2008) and possibly triggering completion of the United States and Euro’s supremacy as global currencies. While permitting banks to stop working might trigger considerable problems for the monetary system, the exact same can be stated for allowing currencies to pump up exceedingly – especially offered the United States and Europe import reliance. Undoubtedly, there is no simple service to this scenario as the long-held effort to “kick the (financial obligation) can down the roadway” will no longer are sufficient.

Financiers might wish to focus less on the local banks and more on the big systemic banks, consisting of those of Europe. The ripple effects of Credit Suisse’s “failure” have actually been restricted through considerable federal government intervention, likewise needing doubtful legal actions that totally neglected financiers’ rights The Swiss federal government rapidly neglected the typical due procedure in this scenario to reduce the crisis. Obviously, if this takes place once again, for instance, in Deutsche Bank ( NYSE: DB), financiers must most likely not anticipate to exercise their investor rights. Obviously, DB’s scenario is various than Credit Suisse’s, so the business might handle to prevent this situation.

Will Deutsche Bank Do The Same?

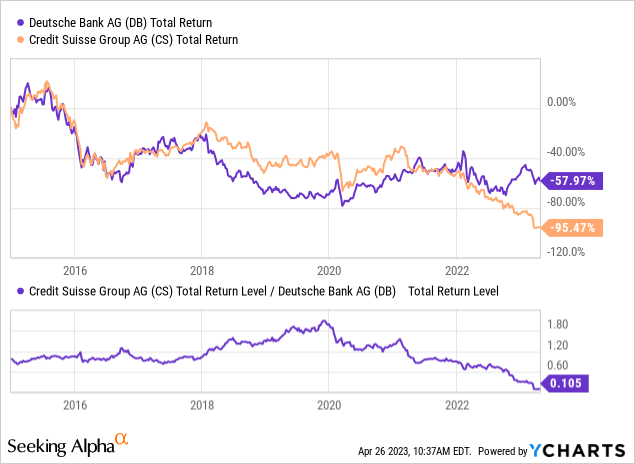

DB and CS sold lock-step for the majority of the years following the European Financial Crisis of ~ 2011. Both banks were discovered to have tremendous non-performing loans and considerable threats within their derivatives portfolios. Nevertheless, because 2019, the tide has actually moved as Deutsche Bank closed lots of tradition services and significantly minimized sales & & trading and financial investment banking services. This modification has actually offered DB with a reasonable quantity of seclusion from the present crisis, as the sharp downturn in IB and S&T activity in 2015 was the preliminary main offender in CS’s fast failure. See their relative efficiency listed below:

Deutsche Bank is a benefactor of Credit Suisse’s collapse as it looks for to absorb its running away customers and has actually had an eye on a few of its properties Obviously, the basic boost in stress and anxiety in European and United States monetary markets does not bode well for the business due to its bad historic performance history. The expense of guaranteeing DB versus default (credit default swap) has increased significantly this year and is the greatest because 2016 While DB and CS are now really various services, the marketplace is worried that the ECB and SNB will not include the contagion element.

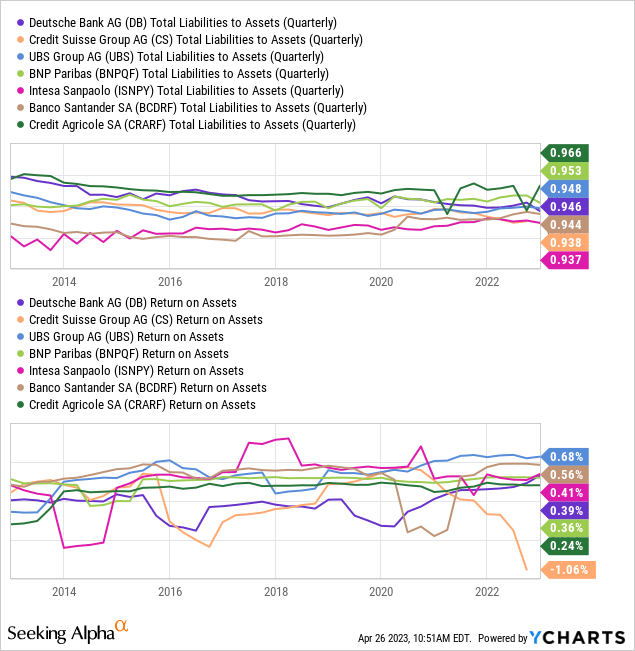

Surprisingly, Deutsche Bank ranks around the middle of the pack in regards to total financial obligation take advantage of and returns on properties compared to the other biggest European banks. See listed below:

Significantly, the French banks BNP Paribas ( OTCQX: BNPQF) and Credit Agricole ( OTCPK: CRARF) rank the worst due to their high financial obligation take advantage of levels and lower possession returns. High take advantage of is not always a problem, however when ROA levels are low, and deposit loaning expenses are increasing, it can cause considerable losses. Still, those 2 banks have usually steady earnings levels, while Deutsche Bank’s ROA volatility is the greatest after Credit Suisse. DB’s earnings has actually been especially unstable over current years as it moved its focus far from monetary services and closed tradition services.

Deutsche Bank has actually prospered regardless of stress in a number of its peers. The bank’s financial investment banking revenue stayed typical in 2015 at ~ E3.5 B while its business and personal earnings grew. Its possession management earnings decreased by 27% in 2015, however that might reverse as it gets a few of Credit Suisse’s customers. DB’s CET1 ratio was 13.4%, lower than Credit Suisse’s at 14.1%; nevertheless, CS’s failure is generally attributable to a loss of self-confidence and losses on monetary services, not insolvency (as in SIVB and others in the United States). DB’s CET1 ratio is a bit greater than the majority of United States banks; nevertheless, as seen in SIVB, CET1 ratios are tricking because they do not represent the majority of sovereign financial obligation (which underwent considerable latent losses in 2015).

At the end of 2022, DB reported having EUR1.32 T in properties and EUR1.26 T in liabilities, with EUR72B in net equity. The bank is huge, however it is not completely clear what fixed-income securities direct exposure it holds today. Its last yearly report ( Pg. 180) revealed EUR491B in overall monetary properties (leaving out loans); of those, EUR299B consisted of derivatives positions, while around EUR100B were fixed-income trading properties. This information shows that the bank’s direct exposure to latent losses on bond properties is likely lower as a portion of equity than we see in the majority of United States banks today. Relatively, European and UK pension funds are most likely bring more considerable sovereign financial obligation loss direct exposures.

Still, we must not cross out the possibility of DB suffering considerable losses due to a sharp increase in danger. Germany’s 10-year bond has actually not increased as much as United States bonds and is presently at 2.37% today, up from -60 bps in 2020. Because Germany’s yields stay so low, its inflation has actually been greater at 7-9% year-over-year over current months, showing German and European bond yields and rates of interest might require to climb up far more. The ECB is raising rates of interest, however that figure is still around 1.25% listed below the dollar’s

Since Europe has lower rates of interest and greater inflation today, I think it will require to see a sharper increase in both long-lasting and short-term rates to tame its inflation. Because rates of interest on German fixed-rate financial obligation were so low in 2020 (usually unfavorable), the “period effect” from an increase in rates of interest will be far more considerable on European financial obligation than United States financial obligation, especially if rates of interest continue to increase in Europe.

The Bottom Line

In General, Deutsche Bank is not Credit Suisse. The bank’s monetary services company carried out better than its Swiss peers did in 2015 due to the business’s proactive transfer to combine operations in 2019. The total scenario produces some “loss of self-confidence” danger for Deutsche Bank; nevertheless, this is minimal since financiers and customers have less locations to go today, and there are basically no “really safe” European or United States banks to change towards.

While the bank’s default danger has actually grown substantially, it is still lower than in 2016 and much lower throughout the European financial obligation crisis. Unlike Credit Suisse, the bank does not seem dealing with a big wave in possession and customer outflows that might bring it under; in reality, it might take advantage of the circulations from Credit Suisse. Even more, due to its bad historic performance history, DB continues to trade at a considerable discount rate to its peer group, at a terribly low “price-to-book” of simply 0.28 X, compared to a sector mean of 1.01 X. The majority of its other appraisal metrics are in between 33% and 66% listed below the sector mean, showing DB is trading at a significant discount rate today compared to peers.

Offered the boost in quality and stability of DB’s company and its huge discount rate, a prolonged outlook on the stock would be sensible. That stated, I am neutral about the stock and am not bullish on DB. While the bank has lots of favorable characteristics, I think the total systemic danger in the European monetary system is really high today, originating from the continent’s enormous inflation level (due to its direct exposures to Russia-Ukraine) and the requirement for a sharper increase in EU rates of interest. Banks with big acquired books, like DB, can bring nontransparent instructions to such a considerable and sharp increase in rates, especially thinking about EU rates were unfavorable simply ~ 18 months back.

If the European bank crisis continues to grow, I question DB will be the beside go. I think DB will rank much better than the majority of in this regard because financiers and experts ignore the business and might overstate other EU and UK banks, such as NatWest Group ( NWG). Obviously, offered any European, UK, and most likely United States bank that is “systemically crucial” starts to deal with stress, I do not think Deutsche Bank will have enough solvency to prevent taking a hit. Therefore, I would not personally purchase DB stock today, especially thinking about the unpredictabilities concerning its enormous derivatives and trading book.