jetcityimage

After the bell on Thursday, we got very first quarter outcomes from online retail and innovation huge Amazon ( NASDAQ: AMZN). This report was going to be carefully enjoyed to see not just if there has actually been a downturn in customer costs, however likewise the crown gem of Amazon Web Provider (” AWS”). As it ended up, Amazon’s quarter was much better than anticipated, sending out shares dramatically greater in the after-hours session on top of Thursday’s 4.6% rally.

For Q1, Amazon reported overall profits of $127.4 billion, beating street quotes by nearly $3 billion. The development was once again led by AWS, revealing a 16% year over year boost (leaving out currency motions), and although there was a small consecutive dollar decrease, the year over year development outcome was a portion point above expectations. North American sector sales were up 11% also, with worldwide up 9%, once again both ex-currency. In general, Amazon reported a $2.4 billion sales struck from currencies versus the year ago duration, however still reported an approximately 9.4% boost for the leading line.

Maybe the very best part of this report though was Amazon’s margin structure. The business has actually been working just recently to cut some costs throughout the company. The North American sector had the ability to reveal its very first favorable operating margin in more than a year, swinging to a 1.2% margin as compared to minus 2.3% a year previously and unfavorable 0.3% in Q4. International margins were still unfavorable, however enhanced both sequentially and on a year over year basis. AWS margins ticked down a little from Q4 levels, however at 24% still stay the earnings center of business, providing nearly $21.5 billion in running earnings over the previous 12 months.

Amazon can be found in with 31 cents of incomes, beating the street by almost a penny, and this consisted of a half a billion dollar pre-tax charge due to the modification in Rivian’s ( RIVN) appraisal throughout the quarter. Amazon has actually made a big financial investment in the electrical car maker, however it has actually been required to mark this holding down a lot in current quarters as Rivian’s losses and money burn have actually accumulated. The business’s earnings figure considerably enhanced in spite of an almost $2.4 billion tax headwind over Q1 2022 levels.

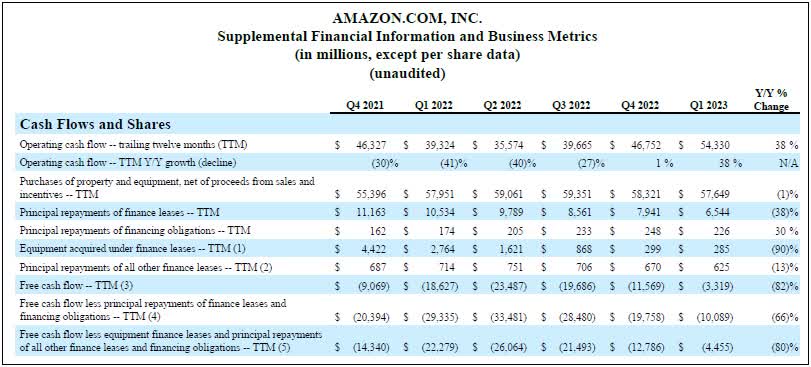

Among the essential products I have actually been talking about in current quarters for Amazon was its capital photo The business has actually been investing greatly not just to grow out its AWS facilities, however likewise its satisfaction and shipment organization post-COVID thanks to more online shopping. This led to complimentary capital going rather unfavorable, leading to Amazon handling a little financial obligation. Nevertheless, as the graphic listed below programs, routing 12 month complimentary capital patterns have actually continued to enhance and are nearly back to the flat line.

Amazon Capital Information ( Q1 2023 Incomes Release)

For the present quarter, assistance from management was mainly in-line with expectations. Amazon is requiring profits of $127 billion to $133 billion, while the street was at $130.34 billion. Running earnings assistance might appear to be a bit light, however the business is typically extremely conservative with its assistance here, and the bottom line number can differ additional depending upon how Rivian shares fare by the end of June.

Amazon has actually constantly been among the beloveds of wall street, with 49 of 53 experts having some kind of buy suggestion on the stock entering into incomes. The typical rate target on the street was $137 and modification, indicating $20 of upside from where the stock remained in the after-hours even after its 7% rally. We may see a couple of rate target walkings based upon the Q1 beats, however I do not see a significant factor for experts to actually alter their numbers here.

There are 2 concerns I have with Amazon at the minute, nevertheless. The very first is if the United States does get in an economic downturn later on this year, customer costs is most likely to take a hit. Today, it looks like travel and experiences are getting a great deal of the discretionary costs combine with COVID mainly behind us lastly, so possibly products costs is not where you wish to be presently. The other concern is if the AWS development rate comes even more down into the low teenagers and even single digits, there will be stress over considerable competitors making inroads here. Income development rates for Amazon are anticipated to increase throughout 2023, which increases the pressure for the business to provide in what might be a rather harder environment.

In the end, Amazon reported strong outcomes on Thursday, sending out the stock well greater later on. Q1 profits beat the street well and were in fact above the high-end of management’s assistance variety, in spite of a somewhat bigger than anticipated currency headwind. While the AWS development rate continued to decrease, it wasn’t as bad as feared, and the North American sector swung to an operating earnings, sustaining a bottom line beat. Capital patterns are definitely enhancing, and Q2 assistance was good. In the meantime, I do not believe there is a factor financiers need to alter their total position on Amazon, although I’m reluctant to advise purchasing right after this $20 rally in the previous 2 weeks offered some headwinds that might be coming later on this year.