ozgurdonmaz

Financial Investment Summary

Alcoa Corporation ( NYSE: AA) has actually grown its organization into numerous various product markets and it presently produces and offers bauxite, alumina, and aluminum items in the United States however likewise worldwide. As product rates tend to be unpredictable it brings a particular level of danger to buying a business like Alcoa. In 2022 the rate of aluminum escalated that made AA able to produce big quantities of incomes as compared to years prior. With relocations from the United States, there may likewise continue to be a lack of aluminum on the marketplace, which in my viewpoint would assist keep rates raised and be a driver for AA as soon as again.

Today the marketplace appears to be in rather a chaos and the margins for AA are decreasing rapidly. I do not believe today is the very best time to purchase shares in the business, we may effectively see another action down in margins providing an even much better purchasing chance. I believe a hold ranking is reasonable till margins decrease more and we get more verification about how huge of a lack we may have with aluminum.

Quarterly Report

In the last quarter, the business handled to produce $2.7 billion in incomes in spite of the lower product rates compared to a year back. A decline of around 18% YoY may appear distressing however it’s the rate you spend for buying product price-driven business like AA. In spite of this recession in incomes, the business is still determined about keeping a strong balance sheet to hedge versus times like these. The CEO Roy Harvey stated the following in the last report “We continued to preserve a strong balance sheet”. A remark I believe is very important to display where the concerns lie, and I believe they appear to be where they ought to be.

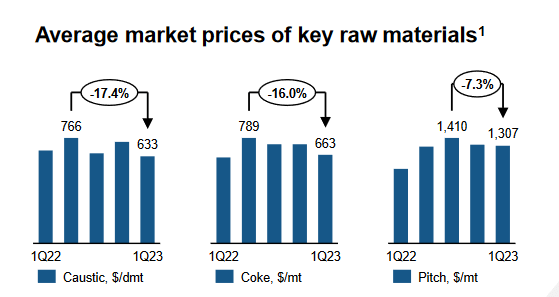

Secret Products ( Revenues Discussion)

Besides that, he likewise discussed a few of the obstacles moving forward, “We’re likewise making essential development in supporting our operations, with groups working to enhance on a minute-by-minute, day-by-day basis.” Keeping margins at an appropriate level will be extremely essential for the coming quarters. Typically with product business you wish to purchase when margins look dreadful and possibly offer when the margins look wonderful. Today I believe we may have more disadvantage to the margins, however the long-lasting pattern for aluminum appears favorable which I believe will benefit AA significantly provided they produced about simply all of their incomes from that section in the business.

Threats

Buying product business is certainly dangerous as the incomes are straight associated to the marketplace rates. The benefit a business like AA has versus another is the capability to produce more incomes and with a much better margin which assists share rates increase exceptionally throughout booms like in 2022 for AA. Throughout the very first 4 months approximately for the business the share rate increased around 50-60% as financiers gathered to the business. However then the rate can simply as rapidly decrease to show a more adversely priced product.

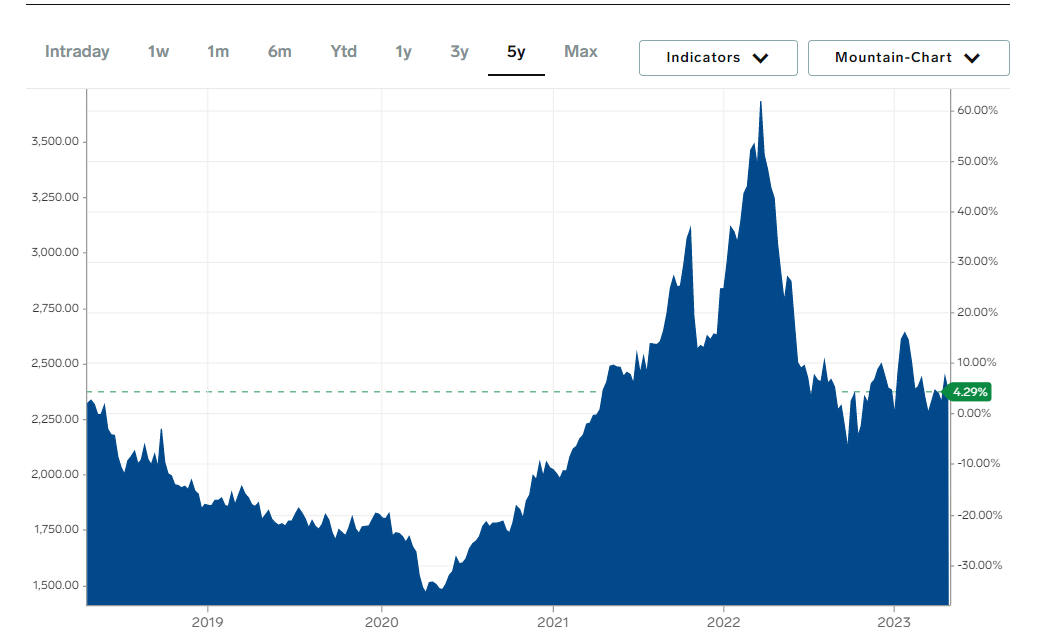

Aluminum Rate Chart (Market Expert)

I believe the most significant danger of purchasing a business like AA is prematurely. Typically the very best offers are discovered when the margins are totally dreadful and there does not appear to be an end in sight for the reduction. Purchasing when margins are fantastic is the reverse of worth investing in product business.

Financials

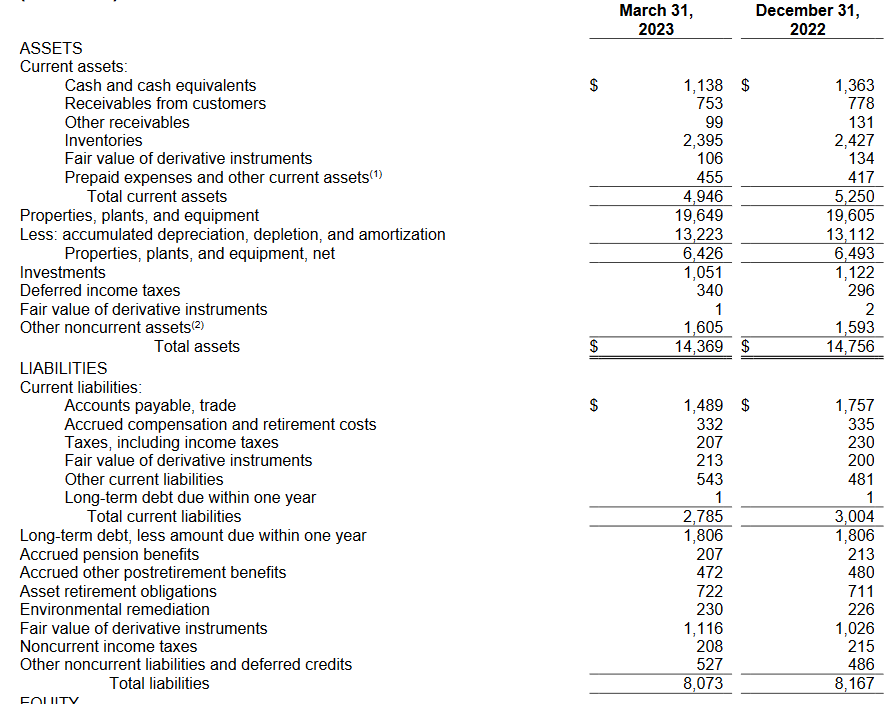

Taking A Look At the financials of the business they appear to be in a steady position. The money position may have fallen somewhat on an annual basis however I do not see it as too distressing. It has actually decreased around $200 million. Typically holds true that business develop a strong position when incomes are strong and times beneficial, and after that hedge with that capital when rates are less beneficial. Stocks appear to have actually stayed rather consistent and this has actually caused the ROA taking a hit as the incomes are now less than a year back. The business presently has a ROA of -5.73% which I believe ought to be viewed extremely thoroughly in the next couple of quarterly reports as it can provide a hit at whether share dilution will ever show up.

Balance Sheet ( Revenues Report Q1 2023)

Moving over to financial obligation, the business needs to be great to manage the existing financial obligation as its just $1 million whilst the long-lasting is $1.8 billion. Another green flag from the balance sheet is that the existing possessions practically surpass the existing liabilities by practically 2x. I believe that the business needs to be needing to handle more financial obligation to sustain development. They even closed a smelter in Washington State as specified in the last report. Today it appears healthiest to simply combine and preserve rather good margins till there is another product rush which AA can gain from.

Evaluation & & Conclude

Taking a look at the appraisal of the business the forward p/e looks rather horrendous at 38x revenues. However as I have actually stated time and time once again, purchasing or holding shares when margins look the worst has actually shown a winning technique with commodity-driven business.

Rate Chart ( Looking For Alpha)

The p/s of the business does not appear expensive at simply 0.6 x forward sales. To supply some more green flags for the business the net debt/EBITDA is simply 0.57 utilizing the TTM numbers. I do nevertheless anticipate this to increase as the incomes continue trending downwards since of the less beneficial aluminum rates compared to 2022.

All in all, I believe AA stock is a hold in the meantime. There are indications indicating a stable need for aluminum with markets like China and India being huge purchasers. This ought to assist the long-lasting outlook for the business and supply a case that incomes can gradually be increasing.